SHANGHAI, Aug 13 (SMM) - The rebar output increased slightly by 0.97% week on week, and apparent demand of rebar rebounded significantly by 9.37% on the week.

Inventories of rebar across Chinese steelmakers and social warehouses stood at 11.48 million mt as of August 12, down 36,100 mt or 0.31% from a week ago. Stocks are up 325,300 mt or 2.94% from a year earlier.

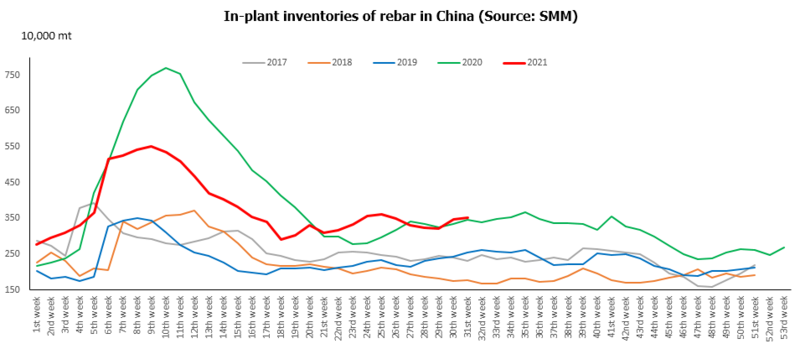

Despite the higher output, the increase in the in-plant rebar stocks narrowed significantly this week, indicating that the in-plant inventories were being transferred to social warehouses more rapidly.

Inventories at Chinese steelmakers rose 42,700 mt or 1.23% on the week and stood at 3.51 million mt. Stocks are up 37,900 mt or 1.09% from a year earlier.

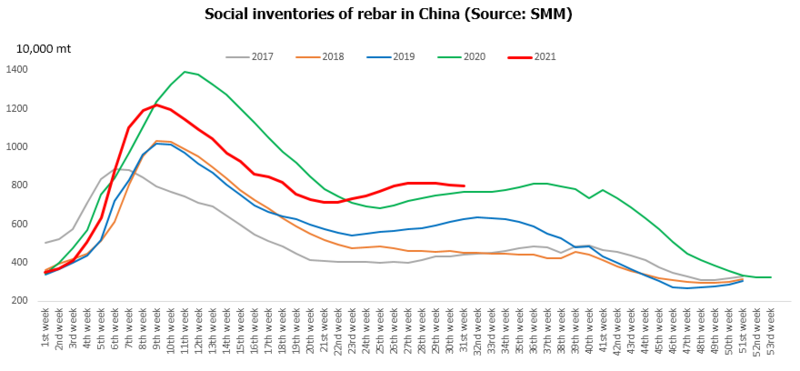

Futures and spot prices both rebounded this week boosted by the funds, and the end demand grew slightly. Speculative demand was also tense. Social inventories of rebar fell more rapidly as daily transactions picked up.

Inventories at social warehouses declined 78,800 mt or 0.98% on the week and stood at 7.97 million mt, up 287,000 mt or 3.74% from a year ago.

Supply and demand were still declining in the short term. Although the crude still capacities were under the production cut policy, the decrease in supply was narrowing. Fewer plants were reducing production against high profits and the approaching peak season. Crude steel output is likely to fluctuate or rebound.

The price trend will be dominated by the demand expectations. Steel prices rebounded and stabilised this week, showing that the end demand rebounded, and the purchase by end users increased. Most speculators were wait and see, but some had entered the market. The restocking demand of middlemen and downstream users for the peak season started to grow in mid-August. If the midstream and downstream demand continues to grow, steel prices may fluctuate higher. However, the increase in the steel output may be interfered by the pandemic, typhoons, and the heavy rainfall in the middle and lower reaches of the Yangtze River.

In the long term, the consumption may not stand high in the peak season, but the prices may not see a sharp drop. Steel prices are likely to remain volatile at high levels and rise higher in October and November. On the supply side, the production cut policy for crude steel may be fully implemented in H2 2021. Considering the profits and supply, the overall decrease in the production may be slighter than market expectations. However, the supply is still expected to be tight. The most serious production restriction is expected to be implemented in the heating season in Q4 2021.

On the demand side, real estate demand will fall in the second half of the year, but the decline will be relatively mild. The sales in the real estate market performed strongly in H1 2021. The sales increase was narrowing, but under the high turnover of housing enterprises, construction will soon be started on the centralised supplied land. Moreover, the investment in real estates is unlikely to fall sharply, so the steel demand by real estate market will decline moderately, showing a certain degree of resilience. As for the infrastructure construction, the special bond issuance of local governments may be accelerated in H2 2021, based on the instructions to reasonably control the investment and local bond issuance progress from the CPC Political Bureau meeting. Therefore, although the growth rate of construction steel demand in the second half of the year will slow down, it will still maintain a certain degree of resilience and will not stall and decline. In addition, the demand may peak in October and November, during which the supply might be tight due to the production restriction.

The supply may rebound in the short term, and steel prices will continue to fluctuate at high levels amid recovered demand. The market needs to beware of the sharp surge and fall in the short term.

![[SMM Hot-Rolled Coil Daily Transactions] Spot Transactions Weakened Somewhat](https://imgqn.smm.cn/usercenter/LVqfJ20251217171736.jpg)