Non-ferrous

Non-ferrous

Base Metals

Rare Earth

Scrap Metals

Minor Metals

Precious Metals

New Energy

Price CenterDatabaseProReportsEventsCar Insight

Language:

Language:

SMM July 21: in an online live conference hosted by SMM, SMM lead analyst Wang Huilin said, "where is the key to breaking the situation at the turn of the off-peak season when inventory splits at home and abroad?" The theme was explained. She said that production of recycled lead and primary lead in the lead spot market in 2021 recovered positively, with supply slightly stronger than the weak fundamentals of demand. However, the recent lead price correction gradually narrowed still need to pay attention to, in the third quarter, SMM maintained a relatively positive expectation, Shanghai lead is expected to run between 15500-16500 yuan / ton.

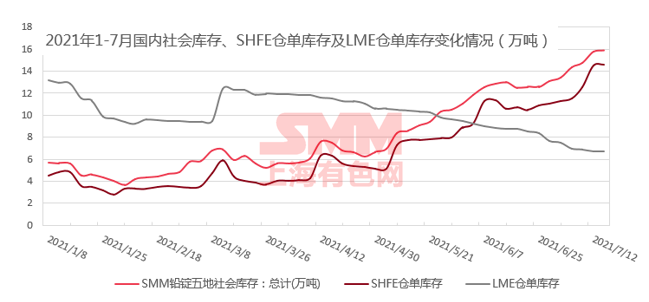

First, lead external strong internal weak inventory split

The split Hulun ratio of inventory at home and abroad has been declining all the way.

Since May, domestic and foreign inventories have split, the Shanghai-Lun ratio has been falling, car sales in May fell for the first time in 13 months compared with the same period last year, and there is a global shortage of chips, leading to a lack of expectations for car production and sales this year. The growth momentum fuelled by China's stimulus policies is beginning to fade.

And overseas markets are beginning to get rid of the blockade and look forward to "hitting the road." at present, North America and Europe are more like the domestic market at the beginning of the lifting of the blockade in 2020. People are gradually getting off the blockade and getting back on the road. Car consumption and lead battery replacement demand have been released.

So from a global point of view, the demand for lead ingots has risen slightly. According to (IlZSG), an international lead-zinc research group, the global lead market has a shortage of 42000 tons in the first five months of this year and 34000 tons in the same period last year. Global lead demand this year will be about 20 per cent higher than last year. Wood Mackenzie (Wood Mackenzie), a research firm, predicts that the global demand for lead used to replace car batteries will rise by 5.9% from 2020 to 6.5 million tons in 2021, returning to pre-pandemic levels.

The storage capacity of three lead ingot delivery warehouses expanded by the lead ingot delivery center increased by 35000 tons during the lead ingot delivery period.

The Shanghai Futures Exchange has continuously expanded two delivery warehouses within a week, continuously increasing the lead ingot delivery warehouse capacity by 3.5 tons in two months. according to statistics, the total storage capacity of lead ingot delivery warehouses in five places in China has exceeded 265000 tons.

At that time, the intention of downstream enterprises to receive goods at high prices was very low, and spot trading was quite light, and spot lead ingots basically maintained a large discount, but at that time, Shanghai lead rose along with Lun lead, and the trade market gave priority to delivery between delivery positions and tedious exports. in this way, domestic lead ingots began to accumulate as scheduled.

Second, at the turn of the off-peak season: the narrow range can not go up or down.

Tight balance support lead price at the end of raw material

In fact, the situation of tight supply on the raw material side has existed since 2020, and the supply on the raw material side has maintained a tight balance after 2021. As a result, the domestic lead trading market has always faced the contradiction that the supply of raw materials such as concentrates and waste batteries is tight, but the downstream consumption situation is not optimistic, and the accumulation of lead ingots leads to the difficulty of rising.

In this case, lead prices in the first half of 2021 showed "neither up nor down" volatility, and the recent approach to the off-peak season alternating season, the market began to look forward to the arrival of the peak season to break the deadlock. The reason for the existence of the lead consumption season is related to the increase in sales of cars and electric cars from August to September in history. Consumer demand for summer travel has been there all the time, but this year there has been a shortage of chips and a surge in new energy vehicles, which may be slightly different from previous years.

According to the recent SMM survey, the enthusiasm of the downstream for peak season storage is generally not high, but there will be regional differences. A small number of downstream enterprises along the coast of Guangdong and Fujian said that battery orders have improved somewhat, and export orders began to warm up; however, battery consumption in Jiangsu and Zhejiang markets and northern markets is relatively limited, and the order situation has not taken a turn for the better.

In the case of difficult price increases for downstream products, although Shanghai lead has risen many times to test the first line of ten thousand six, it is expected that it will still be difficult to stand firm in the near future.

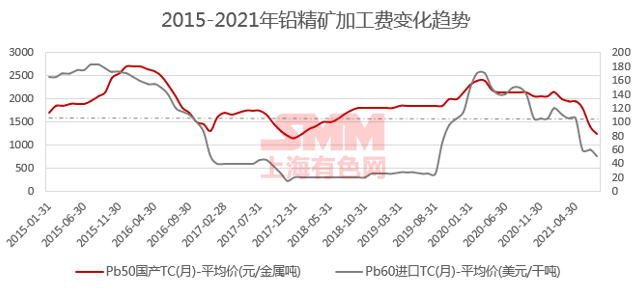

The price of lead smelting raw materials has been strong since 2021.

In 2021, the price of waste battery is easy to rise and difficult to fall, and finally maintain the development trend of slow rise as a whole, but although the cost support has moved up, the production enthusiasm of recycled lead is still relatively high.

From the point of view of the change of domestic lead concentrate processing fee, the result of falling below 1500 yuan per metal ton has been on the low side in nearly 5 years, and the mine's right to speak on the concentrate processing fee is obvious.

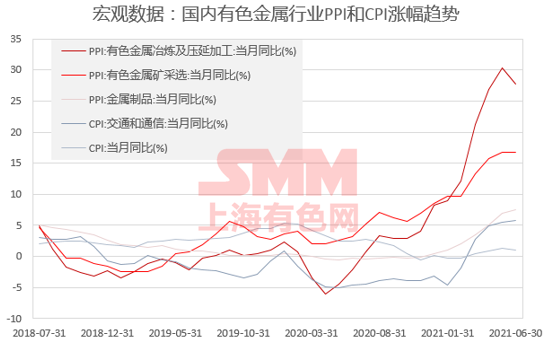

The Macro background of the Nonferrous Metals Industry in 2021-- the growth rate of CPI is not as high as that of PPI.

It is worth mentioning that the lead industry raw materials rise but downstream consumption is not the case, looking at 2021 China's metal industry PPI and CPI situation can be seen, this year's non-ferrous metals industry PPI rose sharply, but CPI related downstream market is completely unable to keep up with the pace, CPI increase is far less than PPI.

With the rise of metal prices, the total profit of mining and metallurgical mining has gradually reached a new high, and the downstream survival pressure is on the high side, which has long attracted the attention of the state. This is also the background of the country's repeated calls to stabilize commodity prices, and to control the excessive rise in the price of non-ferrous metal raw materials through the dumping of copper, aluminum and zinc, giving the lower reaches a respite.

However, in view of the fact that the domestic lead ingots have been in a state of accumulation, compared with the strong rise of other varieties, the increase is relatively limited, so lead has not been included in the control object, nor has it been affected by dumping.

Import profit, loss and balance of lead concentrate

Before that, it was difficult to find the right time for concentrate imports when lead prices were upside down from silver and the Hulun ratio was falling all the way. However, the import volume of lead concentrate remains low in recent months, and the return of superimposed sea freight is far away. It is expected that the import volume will be difficult to recover in the short term.

However, even if the supply of lead concentrate is slightly insufficient, the market will occasionally reduce production due to lack of raw materials, but will soon recover. On the whole, the production enthusiasm of the smelter is still very high, and the production reduction is not obvious. This means that although the concentrate is tight and it is difficult to purchase crude lead, the lead smelter can still maintain normal operation and the normal supply of lead ingots.

Opportunities and challenges under the inflection point of the traditional off-peak season in lead city

Expectation of smelter overhaul / resumption of production scheduling plan from June to July

According to a recent survey by SMM, the supply increment of smelters in June totaled about 6592 tons, and the supply of recycled lead was relatively tightened due to overhaul by large factories. Although the primary lead market in July may cause a small reduction in production due to power cuts, taking into account the recovery plan after the recovery of recycled lead profits, the total recovery increment of refined lead in July is about 30,000 tons, which may continue to put cumulative pressure on the lead market.

Lead smelting actively starts lead ingot supply to maintain a small surplus

Oversupply, low consumption and high inventory put pressure on domestic lead prices.

At present, the basic situation of excess supply of lead ingots is not over, and SMM expects it to be difficult to see an inflection point in inventory in July. In fact, the overall supply of lead ingots this year has been floating over the same period last year, and the increase in the official production of storage batteries is relatively limited, so it is always difficult for lead prices to be traded at high prices, and there has always been an opportunity to buy at low prices in the lower reaches. Therefore, SMM believes that lead prices will be significantly under pressure at 16000 yuan / ton.

Import and export opportunities under strong external and weak internal market

In addition to the supply-side pressure, lead prices still have a chance to break the game for two reasons and are expected to reach the year-round high of lead prices that may occur from August to September. First, the opportunity for internal and external arbitrage or the export of lead ingots, since the second quarter, some people may have completed the long overseas short domestic arbitrage, which also creates conditions for exports. If the subsequent inventory and Shanghai-to-London ratio inflection point comes, it means that the export of lead ingots and internal and external arbitrage may have been completed.

However, it should be noted that, in theory, lead ingots have the conditions for export, but in practice, there will be a series of restrictions that lead to the actual export volume has not been realized. There may be more export intention in the trade market, but it is more difficult for smelters to export directly.

On the other hand, with the advent of high temperature, the inflection point of the off-peak season of batteries in 2021 may come. It is expected that the domestic terminal consumption will bring a turnaround for the lead ingot market in the second half of the year. This period may begin from July to August, when car production and motorcycle production will increase due to the peak sales season, which is the time of year when lead prices are most likely to be high. If the lead price which maintains a narrow range of volatility does not break out of the year's high during this period, then the tone of 2021 will generally maintain the trend of horizontal volatility.

IV. Review and expectation of lead prices in 2021

Looking back at the lead market in the first half of 2021, similar to the mainstream view at the beginning of the year, it stumbled out of the basic rising trend of commodities in the inflation cycle, except that the rise of lead in Shanghai was limited and did not keep pace with the rise of Shanglun lead.

"Click to see the futures market.

The output of recycled lead and primary lead in the lead spot market in 2021 has recovered actively, and the supply is slightly stronger than the demand. However, the recent lead price correction gradually narrowed still need to pay attention to, in the third quarter, SMM maintained a relatively positive expectation, Shanghai lead is expected to run between 15500-16500 yuan / ton.

For queries, please contact Lemon Zhao at lemonzhao@smm.cn

For more information on how to access our research reports, please email service.en@smm.cn