SHANGHAI, Mar 23 (SMM)—Downstream cable companies have placed orders moderately amid price volatility previously. Weak copper demand resulted in slow delivery-taking, accumulating inventory of raw material or finished products at producers. That increased cash pressure at copper rod plants using secondary copper as feedstock, affecting secondary copper suppliers. Secondary copper suppliers have sold aggressively and collected payments to ease cash flow issues. Cash flow issues are expected to intensify due to high tax payment in April. As such, factories and suppliers should liquidate stocks.

Operating rates at copper rod producers using secondary copper as raw material should return to a high level in March against accumulated orders, boosting secondary copper demand. However, decreased new orders at the end of last week and increased cash flow issues have limited the interest in purchasing. That combined with the demand for stock liquidation at suppliers, will keep normal supply and demand.

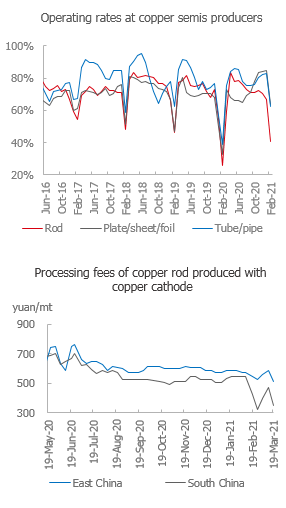

The average weekly price of #1 bare bright copper without invoice stood at 59,930 yuan/mt, an increase of 200 yuan/mt compared with the previous week, and the weekly average price difference between copper cathode and copper scrap stood at 2,217 yuan/mt, an increase of 385 yuan/mt. The average weekly discount of copper rod produced with secondary copper stood at 1,464 yuan/mt against the SHFE front-month copper contract, growing the advantage compared to copper rod produced with copper cathode.

For imported copper scrap, cif quotes for #1 copper scrap were Comex July copper less $0.21/lb, and offers for birch/cliff were Comex July copper less $0.36/lb. US brass was quoted at $5,650-5,850/mt. The coefficient for copper granules (98%) against LME copper stood at 93%, and the coefficient for bare bright copper against LME copper at 96-96.5%, on a cif basis.

Improved consumption of copper rod produced with secondary copper had significant impact on consumption of copper rod produced with copper cathode

Many producers of copper rod using secondary copper as feedstock have seen high orders, reporting strong supply and demand. The price spread between copper cathode and copper scrap has returned to above 2,000 yuan/mt, and discounts of copper rod produced with secondary copper reached a high of 1,550 yuan/mt against the SHFE front-month copper contract. Low-priced copper rods produced with secondary copper have been more desirable for downstream companies amid high copper prices, and this depressed consumption of copper rod produced with copper cathode which has been already weak.

The impact of poor wire and cable demand and secondary copper rods has slowed recovery in the market of copper rod produced with copper cathode. Most of the producers are unlikely to return to normal production levels in March. As consumption picks up amid warmer weather, the market sentiment of the wire and cable industry should rise. Consumption of copper rods produced with copper cathode is expected to improve in April. However, the overly high copper price will depressed consumption. The current inventory of finished products at copper rod producers using copper cathode as feedstock stands at high levels. Producers will prioritise stock depletion and new orders at end users are unlikely to pass to copper rod plants using copper cathode as raw material any time soon. We believe that consumption of copper rods produced with copper cathode in April would hardly return to the peak season level of previous years.

![Ожидания спроса на гуманоидных роботов и высокоэффективные двигатели стимулируют рост сектора двигателестроения, акции Jiangxi Special Electric Motor достигают дневного лимита [Экспресс-новости SMM]](https://imgqn.smm.cn/usercenter/HhNHP20251217171708.jpg)