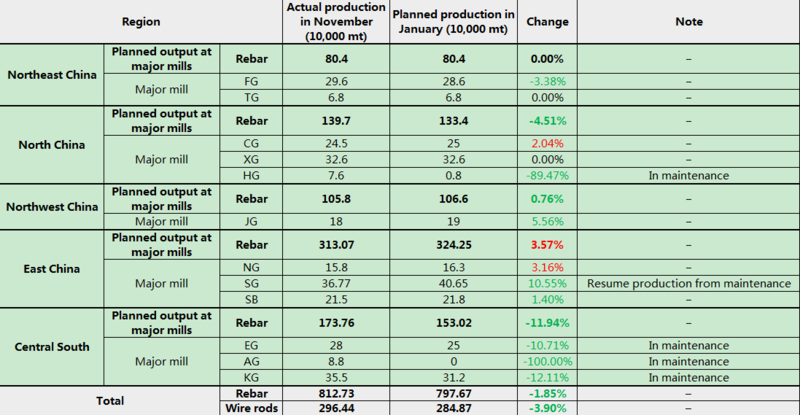

SHANGHAI, Jan 13 (SMM) – Planned output of construction steel rebar across China's major blast furnace steelmakers is estimated to fall 1.85% from the achieved production in December to 7.98 million mt in January, showed an SMM survey.

Scheduled production of wire rods is likely to decrease 3.9% from the actual output in December to stand at 2.85 million mt in January.

The monthly maintenance impacts exceeded 1 million mt from November 2020 to January 2021. This is the most concentrated period of steel plant maintenance since 2019, and steel plant scheduled rebar production is also at a low level.

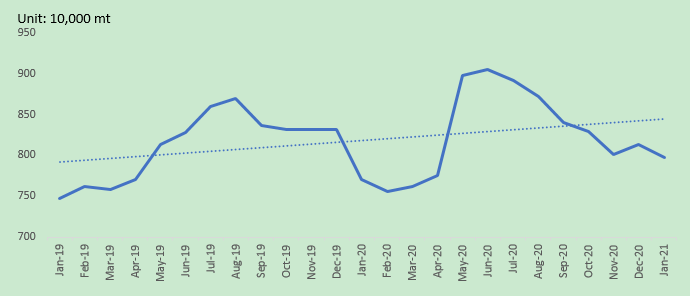

Planned rebar output across China's major blast furnace steelmakers

Source: SMM

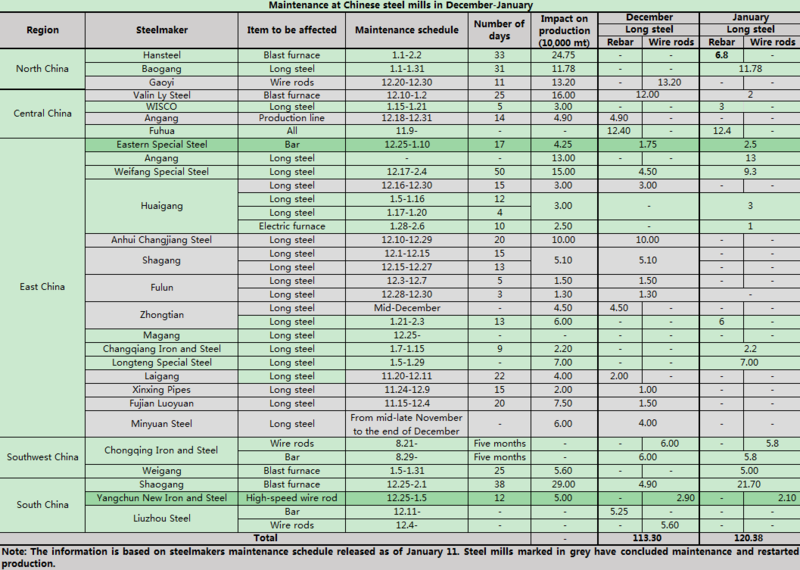

Maintenance at Chinese steel mills in December-January

Source: SMM

The concentration of maintenance in steel plants is mainly due to excessive absolute prices of raw materials, tight coke supply, and annual maintenance demand.

The performance of the raw material end was outstanding in the steel market in 2020. Coke capacity reduction efforts far exceeded market expectations, especially in the second half of 2020. As the backward production capacity was gradually eliminated, even operating rates of coking enterprises continued to decline. In mid-to-late December, operating rates of coking enterprises even dropped to the level of early March, 2020. The coke supply gap continued to widen. Coke prices have experienced 13 rounds of increases since the second half of 2020, and the cumulative increase has reached 500-600 yuan/mt since November alone. According to SMM calculations, the cost of steel plants has risen by 225 yuan/mt.

For iron ore, driven by high demand, lower-than-expectations supply, the appreciation of the yuan, as well as the increase in US gold ore prices, the cost of rebar has increased 579.35 yuan/mt. Gold prices have risen by $55 since November 2020 (the average US gold ore price in 2020 increased $17.66 from 2019).

Although rebar prices are rising, the production profit of steel mills is weak. Some steel mills in Shandong, Hebei and other regions even suffer from losses for a while, and there is an annual maintenance demand for steel mills before the year-end, leading to a significant increase in the concentration of maintenance in steel mills recently, especially in the central and southern regions.

Planned production of rebar and wire rods by region (Source: SMM)

Considering that after the electric arc furnace steel mills got rid of the electricity restrictions in January, operating rates quickly rebounded to a high of over 83%, and the major blast furnace steel mills' scheduled rebar production decreased slightly this month. The rebar supply side was relatively stable in January.

On the demand side, the total scale of demand is gradually shrinking as seasonal disturbances increase (the new wave of pandemic outbreak has a dual impact on demand, some regions encourage migrant workers not to go home for Chinese New Year—or delay the closing date of construction sites or advance work resumption, and there are still some areas to extend the holiday period and require “early holiday”).

Rebar stocks have posted faster increase for two consecutive weeks, and the fundamental weakening situation has been formed. In addition, as winter restocking is imminent this year, and the merchants are on a wait- and-see stance while waiting for winter restocking of the steel mills.

In addition, this is also a busy period for the merchants as they settle payments before CNY, and market transactions are subdued. As a result, upward momentum of the rebar spot price weakened, and rebar prices will show a downward trend in the coming weeks.

![[SMM Hot-Rolled Coil Daily Transactions] Spot Transactions Weakened Somewhat](https://imgqn.smm.cn/usercenter/LVqfJ20251217171736.jpg)