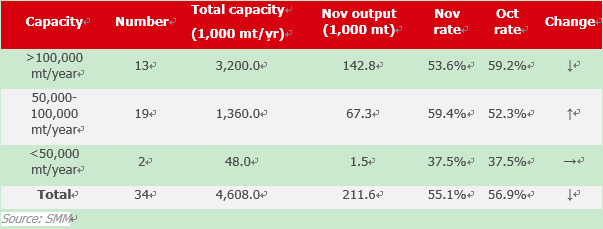

SHANGHAI, Dec 15 (SMM) – Operating rates of the licensed secondary lead smelters in November stood at 55.11%, down 1.82% from October, SMM survey showed. Total capacity in the survey sample which included 34 producers stood at 4.61 million mt/year.

Some secondary lead smelters resumed production as lead prices trended higher in November, but their profits rose limitedly and raw materials were difficult to restock amid tight supply of waste batteries and environmental protection management and control during the heating season. Operating rates at secondary lead producers continued to decline.

Operating rates at large smelters whose annual production capacity exceeds 100,000 mt in November fell 5.63% to 53.55% in November. Jiangsu Xinchunxing and Henan Jinli reduced production out of lack of raw materials. Jiangxi Jinyang suspended the production amid maintenance while Shandong Zhongqing suspended operation for one month due to maintenance and losses in early November.

Operating rates at medium-scale smelters whose annual production capacity falls between 50,000 mt and 100,000 mt rose 7.08% to 59.4%. Guangdong Xinyu and Jiujiang Huijin Metal Materials resumed production amid increased lead prices. Guizhou Huoqilin and Sanhe resumed production capacity amid the end of environmental protection in Guizhou. Operating rates at medium-scale secondary lead producers rose in spite of output cut at Hebei Songhe and Shanxi Yichen due to environmental inspection.

Operating rates at small-scale smelters whose annual production capacity is less than 50,000 mt were flat from October and stood at 37.5% in November. However, non-licensed secondary lead companies have difficulty in resuming work and saw low operating rates due to losses and stricter government control.

Environmental management and control in north China during the heating season remains as the market focus. Production capacity in Henan, Hebei, Shanxi and other places is likely to decline. On the other hand, the newly expanded production capacity at Tianjin Dongbang and Guizhou Jinlong will be released in December, production at Chongqing Deneng, Shandong Zhongqing, and Jiangxi Jinyang resumed production amid the end of maintenance while Guizhou Dingxin and Hebei Songhe resumed normal production amid the end of environmental inspections. Operating rates at secondary lead companies are likely to trend higher in December.

SMM survey of 28 secondary lead smelters

For a detailed report on the China domestic lead market on a monthly basis, please subscribe to China Lead Monthly.

![Driven by increased long positions, the most-traded SHFE lead 2605 contract showed a unilateral upward trend today [Brief Review of Lead Futures]](https://imgqn.smm.cn/usercenter/rDPju20251217171722.jpg)