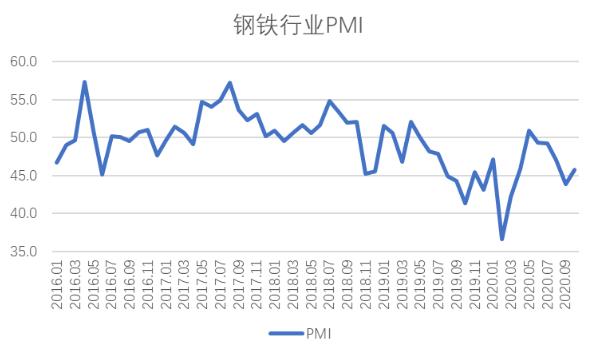

SMM net news:, Zhongwu iron and steel logistics professional committee survey, released the steel industry PMI, October was 45.8%, up 1.9% month-on-month, the iron and steel industry has stabilized. The sub-index shows that the steel market demand has rebounded, enterprise production has increased slightly, the overall cost of raw materials has declined, and the inventory pressure has been further alleviated. It is expected that in November, market demand is still well supported, exports are expected to remain stable, steel production or month-on-month decline.

Fig. 1 changes of PMI index in iron and steel industry since 2016

Market Analysis of Iron and Steel Industry in January and October

(1) Market demand has rebounded

In October, the economic order basically returned to the normal track, the policy of expanding investment and stabilizing domestic demand made steady efforts, and the demand of the iron and steel market also rebounded. The index of new orders was 44.9%, up 8.3 percentage points from the previous month. However, due to the strong wait-and-see mood in the market, the quality of the "Silver Ten" peak season is slightly insufficient, and the index is still running below 50%. At the same time, the rapid spread of the epidemic in foreign countries has affected the steel supply in Europe and the United States, which is conducive to China's iron and steel exports. The index of new export orders was 52.0 per cent, up 5.4 percentage points from the previous month, returning above 50 per cent for the first time since 2019.

According to the understanding of Shanghai Zhuo Steel chain, the current domestic steel market demand is gradually starting, the southern market gets rid of the influence of high temperature, rainy and holiday factors, and the demand release is good, while the northern market is growing due to the approaching winter. According to the monitored purchase data of terminal snails in Shanghai stock market, the average daily purchase volume of terminals in October decreased slightly by 2.06% compared with the previous month, showing a trend of being weak first and then strong.

(2) production of steel mills has increased slightly

In October, driven by the month-on-month rebound in market demand, steel production increased somewhat, but due to the large amount of steel stocks and stricter environmental protection production restrictions in Tangshan and other places, iron and steel production increased steadily, but the increase was relatively small. The production index was 47.1%, up 1.1 percentage points from the previous month. According to the statistics of the China Iron and Steel Association, in mid-October, the average daily output of crude steel in key steel enterprises across the country was 2.1733 million tons, up 0.14 percent from the previous month and 11.24 percent over the same period last year; pig iron was 1.9278 million tons, up 0.28 percent from the previous month and 10.56 percent over the same period last year; and steel products were 2.0766 million tons, up 1.95 percent from the previous month and 10.21 percent over the same period last year.

The rise in steel production has led to an increase in the purchase of raw materials, with an index of 49.3% this month, up 6.2 percentage points from the previous month. Raw material inventory has not changed much, with the raw material inventory index of 40.5%, down 0.4 percentage points from the previous month.

(3) Product inventory tends to decline

In October, market demand stabilized well, driving market sales relatively smoothly. The inventory index of finished goods was 37.3%, up 0.5% from the previous month. Although the index rose slightly, it remained below 40%, indicating that the steel mills had a good situation of destocking.

In terms of social inventory, driven by the start-up of terminal demand, social inventory shows a downward trend as a whole. According to CISA, in mid-October, the social inventory of five major varieties of steel in 20 cities was 12.16 million tons, a decrease of 480000 tons, or 3.8 per cent, compared with the previous decade. In terms of varieties, the inventory of rebar is 5.94 million tons, 390000 tons less than that of the previous ten days; the inventory of wire rod is 1.98 million tons, 70, 000 tons less than that of the previous ten days; the inventory of hot-rolled coiled plates is 2.05 million tons, the same as that of the previous ten days; the inventory of cold-rolled coiled plates is 1.17 million tons, 20, 000 tons less than that of the previous ten days; and the inventory of medium and heavy plates is 1.02 million tons, the same as that of the previous ten days.

(4) Steel prices fluctuate upward

In October, the stabilization of demand led to the strengthening of steel market prices. Zhuo steel chain data show that after the end of the double holiday, the Shanghai rebar index has risen 55 yuan / ton to 3708 yuan / ton compared with the end of September, and then the market price fluctuated with the start of terminal demand, with the Shanghai rebar index rising to 3746 yuan / ton on the 22nd. Near the end of the month, prices fell somewhat. On the 27th, the Shanghai rebar index was 3727 yuan / ton, still significantly higher than the level of the same period last month. It is expected that steel prices will rise first and then decline in November, and demand will continue to release at the beginning of the month. As the weather turns cold, the market demand in the north will gradually weaken, and steel prices may decline in the second half of the month as demand falls.

(5) the pressure on the cost of raw materials has decreased.

In October, the prices of raw materials in the iron and steel industry were divided, the prices of iron ore, the main raw material, fell, while the prices of other raw materials increased to varying degrees, but from the overall perception of the enterprise, the pressure on the cost of raw materials has declined. The purchase price index of raw materials was 47.3%, down 6.8 percentage points from the previous month, and returned to less than 50% after running at a high level for five consecutive months. In terms of varieties, due to an increase in international iron ore shipments and arrivals in October, the Pu 62 per cent iron ore index fell 6.20 US dollars / tonne to 116.95 US dollars / tonne from the previous month. As for other raw materials, as of October 29th, the price of plain carbon billet in Hebei was 3440 yuan / ton, up 120 yuan / ton from the end of the month; the price of scrap in Jiangsu was 2760 yuan / ton, up 140 yuan / ton from the end of the month; the price of secondary coke in Shanxi was 1940 yuan / ton, up 100 yuan / ton from the end of the month; and the price of 65-66 tasty alkaline dry-based iron concentrate powder in Henan was 1060 yuan / ton, up 10 yuan / ton from the end of the month.

(6) keep the funds loose

Yuan loans increased by 1.9 trillion yuan in September, up 204.7 billion yuan from a year earlier, according to the central bank. The scale of social financing increased by 3.48 trillion yuan in September, 963 billion yuan more than the same period last year. At the end of September, M2 grew 10.9% year-on-year, 0.5 and 2.5 percentage points higher than at the end of last month and the same period last year, respectively; M1 grew 8.1% year-on-year, 0.1% higher than at the end of last month and 4.7% higher than the same period last year; and M0 grew 11.1% over the same period last year. The net cash input in the first three quarters was 518.1 billion yuan. Judging from the credit data, money remained loose in September and support at the bottom of the commodity market continued. However, subject to the impact of supply pressure in the spot market, the market performance is relatively cautious. Combined with the domestic and foreign political and economic environment, domestic monetary policy will continue to maintain loose liquidity, so the commodity market opportunities may be released in stages in the fourth quarter.

II. Future research and judgment

(1) there is still a good support for the demand of the iron and steel market in November.

Demand in October showed a trend of first weak and then strong, bringing a steady increase in market demand in November to a good start. In November, China's economic recovery will further accelerate, and the development of the real estate market, the promotion of major national projects, and the rebound of downstream industries such as machinery and automobiles all play a good role in supporting the demand for steel in the domestic market. In the real estate market, from January to September, investment in real estate development increased by 5.6% compared with the same period last year, which was 1.0% higher than that in January-August; the area of new housing starts in January-September decreased by 3.4%, narrowing by 0.2%; the area of land purchased by real estate development enterprises decreased by 2.9% compared with the same period last year, an increase of 0.5 percentage points over January-August. The transaction price of land was 931.6 billion yuan, an increase of 13.8%, or an increase of 2.6%. Investment in the domestic real estate industry rebounds month by month, which provides a good driving force for the sustainable development of real estate, and from the understanding of the market, although the real estate regulation and control policy is still tightened, the heat of real estate transactions is not reduced, so on the whole, the demand support given by real estate enterprises to the steel market in the short term may continue to maintain a relatively exuberant trend. The automobile industry also has a good performance. Automobile production and sales have increased for six consecutive months, and sales growth has been maintained at more than 10% for five consecutive months. As winter approaches, the rush schedule for construction sites in the north will also appear in November. On the whole, there is still some guarantee for steel demand in November.

(2) Steel exports are expected to remain stable

At present, the epidemic abroad is once again serious, France, Germany and other countries have stepped up the blockade. It is expected that the spread of the epidemic may accelerate from November to December, and the economies of countries around the world will be greatly affected. On the one hand, economic vitality will decline and market demand will decline; on the other hand, enterprise production will also be tightened. As an important part of the international supply chain, China's production capacity has been basically recovered. with the continuation of the international epidemic, steel exports in the fourth quarter are expected to remain stable, with a year-on-year decline of 54 million tons. 15% lower than the same period last year.

(3) the production of steel mills may decline somewhat.

Since October, some cities have launched emergency measures for heavily polluted weather. Tangshan City has launched a level II emergency response to heavy pollution weather on October 23, strengthened emission reduction measures, and made detailed regulations on the production limit ratio of sintering machines in iron and steel enterprises. Handan City has also launched an emergency response to further strengthen the management and control of key emission industrial enterprises. With the full implementation of the policy of stopping production and limiting production in various places, and the current rising prices of raw materials such as coke, steel mill production is expected to decline in November and throughout the fourth quarter, but still maintain a trend of growth compared with the same period last year. The annual steel output is expected to exceed 1 billion tons.

Overall, in October, the iron and steel industry stabilized, market demand rebounded, driving up steel production, steel prices shock upward, inventory pressure has been alleviated. The pressure on the cost of raw materials for enterprises has also declined. Market demand is expected to continue to support in November, exports are expected to remain stable, but corporate production or month-on-month decline.