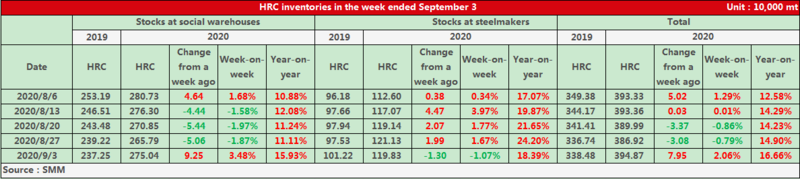

SHANGHAI, Sep 4 (SMM) - SMM data showed that inventories of hot-rolled coils (HRC) and plates across social warehouses and steelmakers, which are used in automobiles and home appliances, stood at 3.95 million mt in the week ended September 4, after a 2.06% increase in the previous week. The stocks were 16.7% higher than the same period last year.

Operating rates of blast furnaces (BFs) at Chinese steelmakers this week came in at 89.6%, which remained unchanged from last week, according to SMM survey. In addition, the hot rolling output maintained stable at a high level this week as operating rates and production of hot rolling lines at various steelmakers basically remained stable. The actual end-users consumption less than expectations at high prices led to a rise of inventories.

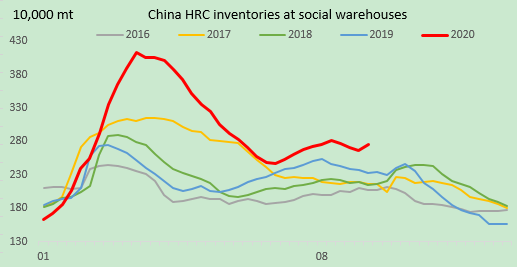

SMM data showed that HRC stocks across social warehouses stood at 2.75 million mt this week, with a rise of 3.48% from the prior week, and up 15.9% from a year ago.

The impact of typhoon weather on shipments gradually weakened and steelmakers in north China significantly increased HRC shipments to the south. Steelmakers correspondingly accelerated the shipments to social warehouses, improving the market supply from the previous period. However, affected by the news environmental protection which limited production, hot-rolled coils spot resources rose again at a high level this week, leading to concerns about high prices and cautious purchasing. The actual consumption was less than expectations. That also accounted for the sharp rise of HRC stocks across social warehouses this week.

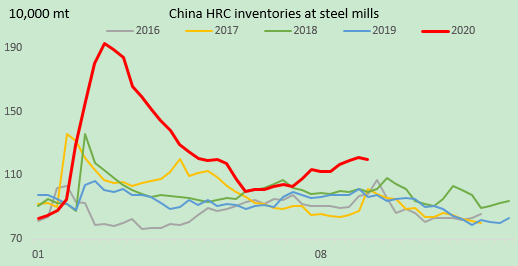

In-plant HRC inventories decreased 1.07% week on week and advanced 18.4% year on year to 1.2 million mt in the week ended September 4, showed SMM data.

Steelmakers in north China accelerated the shipment recently, and the in-plant inventories gradually shifted to the social warehouse. In-plant HRC inventories halted its buildup and started to fall due to the enlarged prices difference between cold-rolled coils and hot-rolled coils and large shipment of the cold-based resources of steelmakers.

Although the output of hot-rolled coil was relatively stable, high prices suppressed the end-user demand obviously, leading to the accumulation of hot-rolled coil inventories and increasing the market supply pressure, especially in east China.

Demand is likely to improve in the following weeks, while the overall release will be delayed due to the suppression of high prices. Meanwhile, traders are pressurised by increasing inventories. Spot prices are expected to trend lower in the next few weeks without the support of positive news.