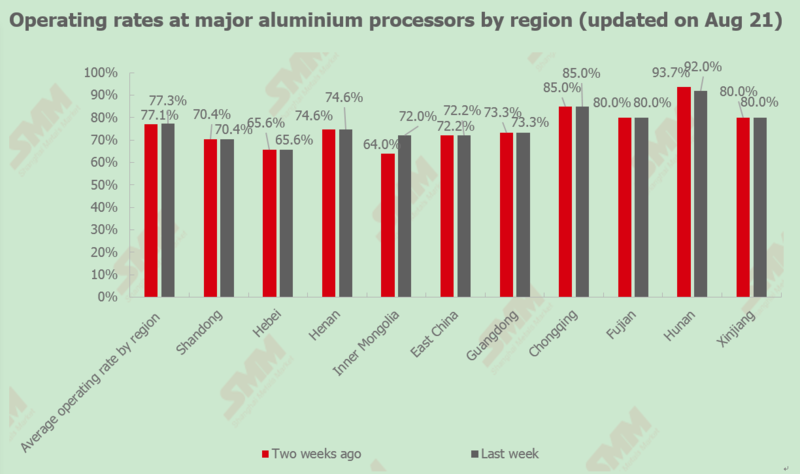

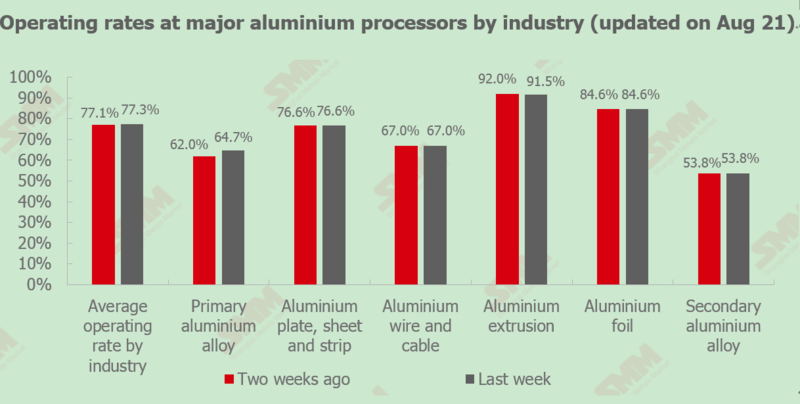

SHANGHAI, Aug 25 (SMM) — Operating rates across major aluminium processors rose 0.2 percentage point on a weekly basis to 77.3% last week, contributed by the commissioning of new capacity at primary aluminium alloy producers. Operating rates are expected to be largely stable this week. Demand for aluminium foil remained robust, while orders at small and medium-scale producers in extrusion, wire and cable, plate and strip sectors remained weak. Worsening COVID-19 overseas kept processors concerned about the recovery of export orders in September. With the import window of aluminium alloy ingots being closed, secondary aluminium producers are increasingly optimistic over the upcoming peak season of September to October. Small and medium-scale extrusion producers showed little interest in aluminium billets produced with re-melted aluminium scrap due to weak orders.

Aluminium plate/sheet and strip: Despite falling new orders, ample backlog orders kept operating rates stable. Demand for construction decorative plate and strip was stable, while orders for can stock and tab stock remained ample. Demand for automotive sheet improved. Export orders remained weak amid COVID-19. A listed firm in Henan produced over 400,000 mt of aluminium plate/sheet and strip in H1, but was concerned about the market outlook in H2.

Aluminium foil: Long production schedules kept operating rates stable. Some producers have been running close to full capacity since June. Orders for electronics foil, electrode foil and brazing foil improved. There are still many backlog orders for air-conditioner foil and light-gauge soft packaging foil from June-August waiting to be delivered. Output at some producers increased in July when compared to a year ago and did not fall sharply in August.

Aluminium wire and cable: As May-August is the period of delivery to State Grid, large producers maintained stable operating rates. However, most producers received fewer orders than last year and are pessimistic over orders in H2 due to uncertainty over the volumes of tenders from State Grid and China Southern Power Grid and as orders on hand will gradually run out.

Aluminium extrusion: Large producers reported ample orders, while orders at small and medium-scale producers remained weak, with no signs of improving in the short term. Aluminium billet processing fees fell sharply after aluminium prices hit new highs, driving extrusion producers to restock as needed. Processing fees in east China recorded smaller declines than Guangdong due to slower transport from Xinjiang amid COVID-19. Exports are expected to continue to decline on a yearly basis. Producers show mixed sentiment over demand in the upcoming peak season. Operating rates at large producers are expected to remain largely stable in the near term.

Primary aluminium alloy: The ramp-up of new capacity boosted operating rates at primary aluminium alloy producers. Operating rates at aluminium wheel plants were little changed in August when compared to July. Producers expect orders from carmakers to increase in September. Processing fees of A356.2 primary aluminium alloy in Wuxi remained stable between 650-750 yuan/mt for self-pick up.

Secondary aluminium alloy: Summer break at die-casting plants occurred mostly in the first half of August. Although most die-casting plants have ended their summer break, production has not yet recovered fully. A growing number of secondary aluminium producers are bullish over future prices, given the low possibility of aluminium scrap import restrictions being loosened in the short term and the closure of import window of aluminium alloy ingots amid sharply rising ADC12 secondary aluminium prices overseas. Secondary aluminium producers reported a slight increase in raw material and finished product inventories, and did not cut output sharply in the low season. Weak orders at small and medium-scale aluminium extrusion producers suppressed demand for aluminium billets produced with re-melted aluminium scrap. Prices of aluminium scrap taint rose slower than primary aluminium. Operating rates at secondary aluminium producers are expected to remain largely stable this week amid arrivals of imported aluminium alloy ingots, and are unlikely to rise until September when supply of imported aluminium alloy ingots declines further and demand improves.