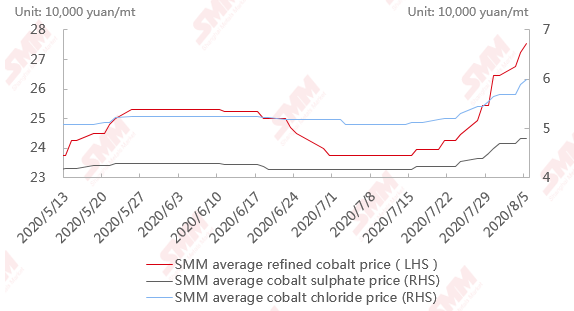

SHANGHAI, Aug 7 (SMM) — Cobalt prices in the domestic market rose sharply. The prices of refined cobalt, cobalt sulphate, and cobalt chloride increased by nearly 10% to 11%, which is higher than about 3 to 4% of the previous month since mid-July.

Chart 1: Changes in prices of cobalt products

Source: SMM

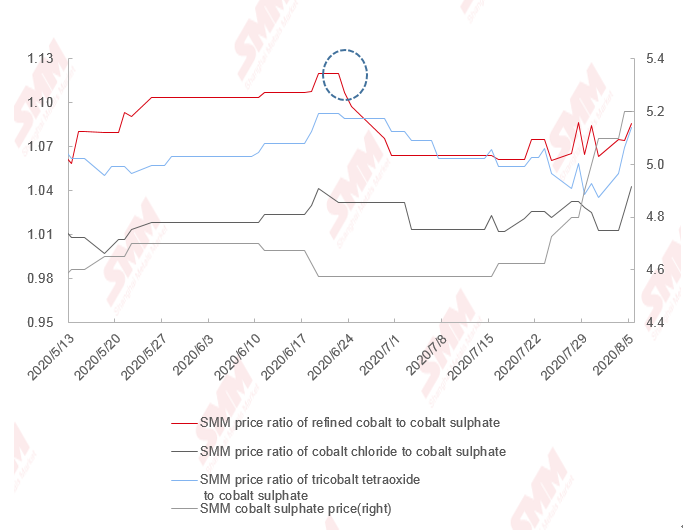

The price ratio of refined cobalt to cobalt sulphate gradually trended to 1 after mid-June, mainly due to the gradual recovery of demand for battery materials.

Chart 2: Price ratio of cobalt products

Source: SMM

Catalysts behind higher prices from May to June include port closure at South Africa in April and a shortage of domestic cobalt raw materials from May to June. There was an oversupply of smelted products in the domestic market, and destocking of cobalt sulphate have improved fundamentals. However, downstream demand did not improve significantly, and the demand for 3C digital electronics entered the low season for procurement, resulting in a small increase in prices.

A sharp increase in prices from mid-July was due to the following factors:

1. Supply end of cobalt raw materials

Although there is a huge number of confirmed cases of COVID-19 in the African mining areas, production has not been affected for the time being. Despite strict prevention and control in the mining areas and the small probability of a large-scale outbreak, the market sentiment remains bearish.

At present, port capacity at South Africa is badly affected by the pandemic. It was understood that port capacity had been slowly recovering since South Africa lifted the transport restrictions on May 1 and the first batch of shipments departed in mid-May, and port capacity from June to July was only 50 to 60% of normal capacity,

According to feedback from cobalt raw material suppliers, the shipping schedule of mainstream suppliers remained the same as in the previous period and there was no sign of improvement due to their special transportation channels. It is expected that the situation would continue for the next two to three months. Some of the August shipping schedules were disrupted, according to suppliers. Over at South African ports, capacity is limited, and cobalt raw materials shipments need to compete for shipments slots with other cargoes.

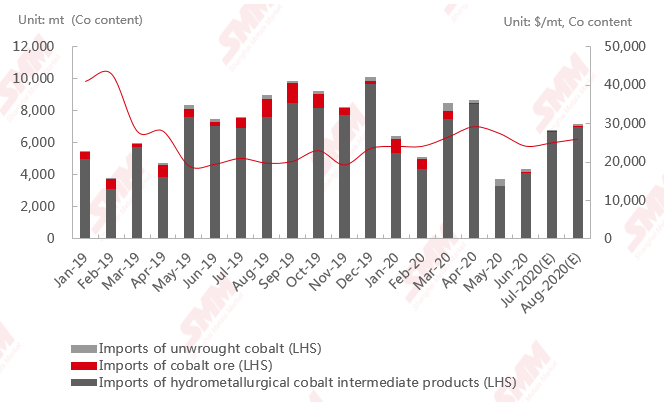

Total imports of cobalt raw materials in Q2 2020 amounted to 16, 800 mt (Co content), a 19% decline year on year. Total imports of cobalt ore stood at 100 mt, a 92% lower year on year; the total import volume of intermediate products of hydrometallurgy cobalt was 15,800 mt (Co content), a 15% decline as compared to a year ago. Unwrought cobalt imports at Q2 stood at 800 mt (Co content), an increase of 57% year on year.

Chart 3: China cobalt raw material imports (Jan 2019- Aug 2020, estimate)

Source: SMM, China Customs

The African government and the industry are rectifying artisanal mining, and will have full control of artisanal mining in August, according to market participants. The import of some cobalt raw materials may be influenced in the short term, leading to tight supply. However, the annual supply of cobalt raw materials from artisanal mining is only 6% to 10% of the total global supply, hence this will have little impact on the cobalt raw materials supply.

Therefore, domestic cobalt raw materials continue to be tight supply in the near term for the next two to three months. According to surveys across shipping sector, the domestic bonded zones, traders, smelters and battery factories, the domestic cobalt raw material inventory is about 9,000 to 11,000 mt, enough for 1-1.5 months of end-user consumption, while consumers usually keep around 2-3 months of cobalt raw material stocks.

In addition, the suppliers of cobalt raw materials are also reluctant to trade at lower prices despite the higher hidden costs of mining companies amid COVID-19. This resulted in a decline of orders and higher prices.

2. Supply of smelting products

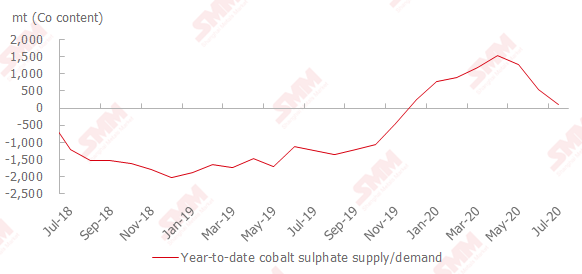

China's cobalt sulphate basically reached a balance between supply and demand in July. Low inventories encouraged suppliers to raise quotations.

Chart 4: Cumulative balance of China copper sulphate (July 2018- July 2020, estimate)

Source: SMM

3. End-user demand

3C digital sector entered the peak of procurement and stocking in the second half of the year, boosting demand for cobalt salt and tricobalt tetraoxide. Inventories of cobalt raw materials at major battery factories stood at least 1,500 to 2,000 mt (Co content), and cobalt raw materials will arrive at ports every month. The raw material inventories of lithium cobalt oxide (LCO) manufacturers and battery factories were higher than those of upstream cobalt salt and tricobalt tetraoxide producers. However, some producers are still worried about the subsequent arrival of cobalt raw materials.

The ternary demand is beginning to rise with positive outlook in the second half of the year. As the purchases of ternary materials by motive power battery factories are basically under long-term contracts battery and ternary material factories have sufficient stocks, and there is still no significant increase in the purchase demand for upstream raw materials. As the growth rate of demand is lower than that of upstream raw material prices, it is still difficult for higher raw material prices to pass through to prices in downstream sectors.

4. Capital inflows and rumour of government stockpiling

The injection of capital into the market amid positive macroeconomic developments triggered a sharp increase in demand for refined cobalt. However, consumption in high-temperature alloys, magnetic materials, chemical and other industries showed no signs of improvement. Rumours of government stockpiling also buoyed prices of cobalt.

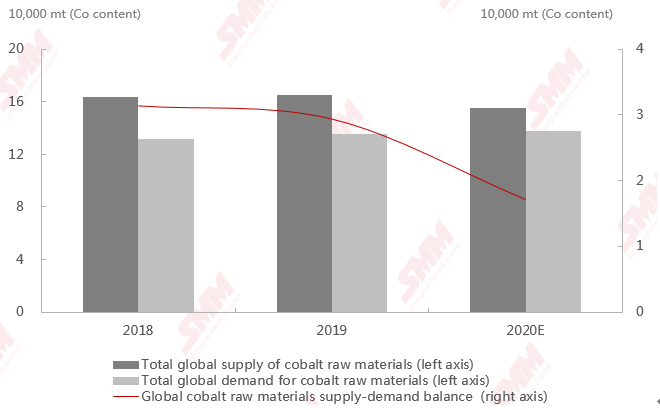

In summary, due to the impact of Covid-19 in 2020, global cobalt supply will remain in surplus. However, the supply and demand situation may improve significantly. It is expected that the global cobalt raw materials will be in a surplus of 17,000 mt (Co content).

On the supply side, Glencore’s Mutanda copper-cobalt mine was shut down. Some new cobalt raw material projects that were originally scheduled to be put into operation this year may be postponed to next year. The supply of artisanal mining would also decrease in the short term. Therefore, SMM has lowered cobalt raw material supply forecast further to 155,000 mt (Co content), a decrease of 6% year on year. On the demand side, SMM lowered production forecasts for new energy vehicles, digital, and energy storage, and the total global cobalt demand was lowered to 138,000 mt (Co content).

Chart 5: Global Supply balance of cobalt raw materials

Source: SMM

Despite increasing demand for LCO and upstream raw materials from 5G, online office and wearable electronic products, the expected declines in production and sales of mobile phones amid COVID-19 will curb demand growth. Therefore, the sharp price increase of upstream raw materials may cause delays in downstream stocking plans. The price increase of cobalt in the second half of the year will be limited, and the price of refined cobalt may fluctuate between 230,000 to 320,000 yuan/mt.