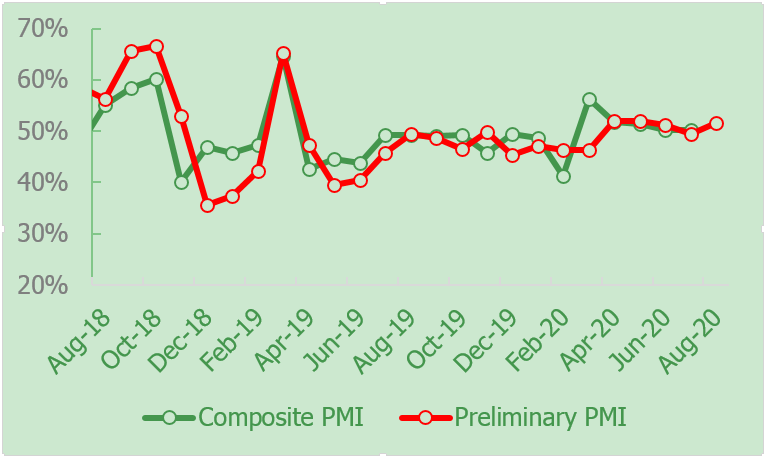

SHANGHAI, Aug 5 (SMM) – Manufacturing activity across nickel downstream sectors in China expanded for the fifth consecutive month in July, but at a slower pace.

SMM data showed that the purchasing manager's index (PMI) for downstream nickel industries, including stainless steel, electroplating, alloy and battery, stood at 50.2 in July, down 0.05 point from June. A reading above 50 indicates expansion.

The preliminary nickel downstream sectors PMI for August is assessed at 51.54, rising 1.34 points from the final reading for July and remaining in the expansionary territory.

Production sub-index remained above 50, with the battery sector taking the lead

The composite sub-index for production in July was down 1.78 points from a month ago at 50.47, staying in expansion. The production sub-index in the stainless steel sector slipped 2.57 points on month to 50.57. In July, the stainless steel market has performed well, with improved profits across mills, and the pace of shipments was relatively normal. Most of the stainless steel makers kept stable production, while some of them returned to normal production from maintenance. The electroplating industry remained the worst performer with a production sub-index of 39.54 in July. Some electroplating plants in south China maintained the mode of “three days on duty and one day off” to ease operating pressure caused by fewer orders.

New orders sub-index returned to the expansionary territory, stainless steel sales beat expectations in the low season

The sub-index for new orders across downstream nickel sectors rose to an expansionary territory of 50.3 in July, up 1.4 points from June, back to the growth-contraction threshold. In the stainless steel sector, the new orders sub-index rose 1 point to 50.3, beating expectations. Although actual end-user demand was softer during the low season, but mainstream steel mills maintained a strategy of stable prices

In the alloy sector, the new orders sub-index rose slightly by 0.1 point to 48.3 in July. Orders at some of the special steel makers in south China have declined. Some plants of alloy for military and nuclear power using in north China reported relatively stable production plans and orders, while some special steel plants in the south reported less orders and reduced planned production by 10-20%.

Sub-index for raw material inventories fell into contractionary territory, surging nickel prices sidelined some downstream buyers

The sub-index for raw materials inventories came in at 49.37 for July, 3.21 points lower from June, falling into the contraction range. The sub-index for raw materials inventories in the stainless steel sector came in at 50, 3.81 points lower from 53.81 in June. Prices of NPI has trended higher in July due to an increase in nickel prices. Although stainless steel plants maintained normal purchases, they are less aggressive in procurement as compared to June, and there was no significant changes in raw material inventories. The PMI for electroplating sector was lower than 50 as plants cut operating rates amid rising base metals prices.

Sub-index for finished products inventories went back to above 50

The sub-index for finished products stocks edged up 0.3 point from a month ago to 50 in July. The sub-index for finished products stocks in the stainless steel sector came in at 50.1, slightly better than expectations. The continuous heavy rainfalls in the south China has affected arrivals of stainless steel. This, combined with factors such as limited supply of spot cargoes and stainless steel makers increasing the proportion of direct suppliers, has resulted in a better-than-expected shipments in the low season.

![[NPI Daily Review] High-Grade NPI May Still Have Downside Room Under the Dual Pressure of End-User Demand and Steel Scrap](https://imgqn.smm.cn/usercenter/CjEnN20251217171733.jpg)

![[SMM Midday Nickel Commentary] On March 24, nickel prices retreated after rapid rise, and Iran denied having held talks with the U.S.](https://imgqn.smm.cn/usercenter/yaAtG20251217171733.jpg)