SHANGHAI, Mar 2 (SMM) – Manufacturing activities across nickel downstream sectors in China accelerated their declines month on month in February and stayed in contraction for the 11th consecutive month, according to SMM survey.

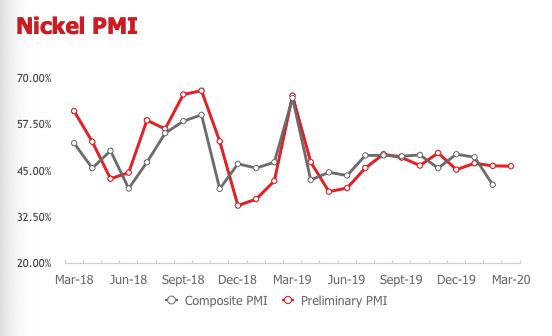

SMM data showed that the purchasing managers' index (PMI) for downstream nickel industries, including stainless steel, electroplating, alloy and battery, stood at 41.24 in February, down 7.46 from January. A reading below 50 indicates contraction.

The preliminary PMI for nickel downstream sectors is assessed at 46.27 in March, 5.03 higher from the finalised reading in February.

Last month, the composite sub-index for production declined 7.97 from January to 37.42, on the back of production cutback at stainless steel producers amid transportation hurdles and inventory pressure. The sub-index for production in the stainless steel sector slipped 6.67 on the month to 38.57 in February. SMM learned that the output cut at stainless steel producers was less significant during the Chinese New Year holiday, before elevated stocks at plants and social warehouses drove producers to expand the cutback. The sub-index for production in the electroplating sector was 29.59 in February, considerable lower than expectations, as most medium-scale and small producers kept closed since January 20 on the impact of coronavirus (COVID-19) outbreak. Only a handful of large-scale spare parts electroplating factories have resumed operations.

According to SMM data, the overall sub-index for new orders across downstream nickel sectors continued to contract by 14.43 on the month to 34.73 in February. Downstream producers in the stainless steel sector recovered at a slow pace as the major trading place in Wuxi (Oriental Market) resumed operations at end February. Transactions remained limited even as some traders accepted orders online, leaving the sub-index for new orders in the stainless steel sector at 34.29 last month. The new orders sub-index for the alloy sector also failed to meet expectations and stood at 39.61, affected by the long production cycle at some producers of military-use alloy. Downstream producers of cars and digital products faced with cash flow burden amid the epidemic outbreak, and this reduced the orders in the battery sector, whose new orders sub-index came in at 34.29 in February.

The overall sub-index for raw materials inventories edged down 2.61 from a month ago to 46.07 in February, as downstream producers continued to deplete stockpiles of feedstock purchased before the CNY holiday. The decline was relatively smaller as affected production and new orders amid COVID-19 outbreak slowed the consumption of feedstock and the reduced nickel prices drove some producers to restock. The raw materials inventory sub-index for the stainless steel sector was 47.14 last month as stainless steel plants purchased nickel pig iron on lower prices, but the procurement volumes were smaller than the normal levels. Alloy producers restocked raw materials steadily, with the sub-index for the alloy sector at 55.95, while the virus impact weighed on base metals prices.

The overall sub-index for finished products stocks flipped to a contraction in February, standing 12.19 lower from a month ago at 41.2. The sub-index for the stainless steel sector slowed to 39.71 as demand came weaker than supply. Battery materials producers scaled back operations to avoid inventory build-up amid sluggish demand, and this saw the finished goods inventory sub-index in the battery sector stabilising at 50.

![[SMM Analysis] Weak Nickel Caps Chinese Stainless Steel Futures in a Tight Range as Mill Price Discipline](https://imgqn.smm.cn/production/admin/votes/imagesLDoQB20260703182347.png)

![[SMM Analysis] Nickel and Cobalt Salt Prices Weak; Intermediate Product Payables Under Pressure](https://imgqn.smm.cn/usercenter/yaAtG20251217171733.jpg)

![[SMM Analysis] Indonesia's nickel ore HMA sharply cut by 7.6%, high inventories in China and Indonesia suppress nickel ore market sentiment](https://imgqn.smm.cn/usercenter/vcoVV20251217171732.jpeg)