SMM7 20: SMM held the 2020 China Ni-Cr stainless Steel Industry Market and Application Development Forum in Wuxi on July 20. At the meeting, Li Chuntian, a senior analyst at SMM, looked forward to the supply and demand pattern and price of China's stainless steel industry chain in 2020.

Analysis of stainless steel production capacity

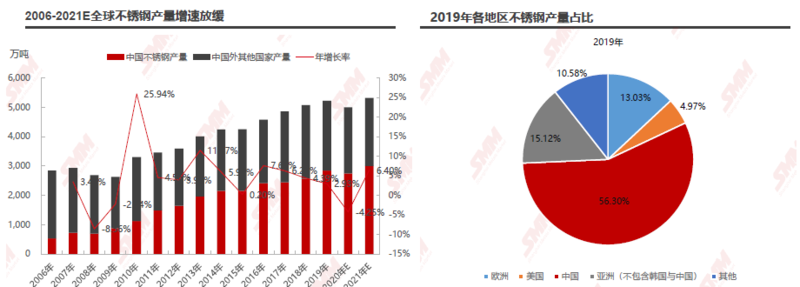

The growth rate of global stainless steel production slows down and China accounts for more than 50%.

After 2010, the global stainless steel production gradually increased, but the growth rate gradually slowed down. In 2010, the annual growth rate of stainless steel reached 25.9%. The output of stainless steel was at a low level in early 2009 due to the impact of the financial crisis, and production began to recover gradually in the second half of 2009.

Production in all regions of the world increased higher in 2010 than in 2009, and then the annual growth rate of stainless steel was maintained at 5%. 6%.

In 2020, global stainless steel production is expected to show a downward trend, a decline of about 4%. Because of the impact of the epidemic, production in all countries was affected, with the largest decline in the first quarter and a gradual recovery in the second quarter.

According to the proportion of output in various countries, the total output of stainless steel in China surpassed that of Japan in 2006, becoming the largest stainless steel producer in the world. In 2019, China's output of stainless steel reached 28.4 million tons, accounting for 56% of the total output.

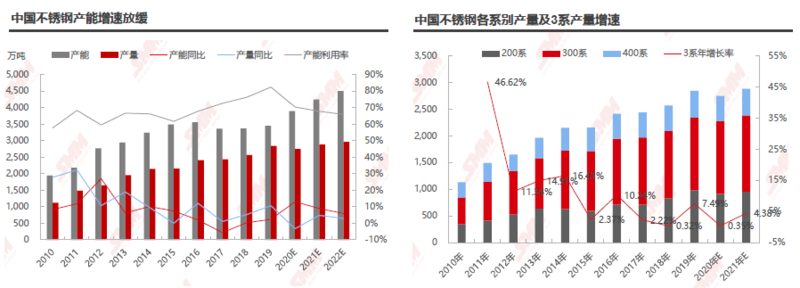

The growth rate of stainless steel production capacity in China slows down

From 2017 to 2019, the output of stainless steel production in China increased at a low speed. On the one hand, the negative impact of the rise of stainless steel industry in Indonesia on Chinese manufacturers; On the other hand, the economic growth rate has changed from high-speed to "medium-high-speed" growth, and its Chinese real estate market and automobile industry have bid farewell to rapid growth, resulting in a decline in the growth rate of stainless steel consumption in China, and a slowdown in the expansion and construction of Chinese stainless steel manufacturers. The expansion presents a trend of integration of raw materials and finished products, with Qingshan Group, Shandong Xinhai, Jiangsu Delong and Mingtuo Group as typical representatives. The red delivery of raw materials has become the main competitiveness of the development of steel mills.

Cost and profit Analysis of stainless Steel

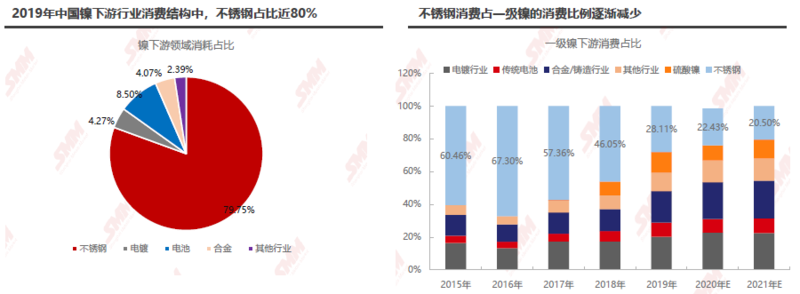

Stainless steel is the main consumption area of primary nickel, and the proportion of primary nickel consumption is gradually declining.

In 2019, in the consumption structure of China's nickel downstream industry, stainless steel consumption is still the main area of nickel consumption, accounting for nearly 80%. The proportion of primary nickel in stainless steel consumption is gradually declining, accounting for about 28% in 2019, and is expected to decrease to about 23% in 2020. The decrease in the proportion of pure nickel is mainly due to the increase in the proportion of high nickel iron in the source of stainless steel nickel.

Analysis on the Source proportion of stainless Steel and Nickel Raw Materials

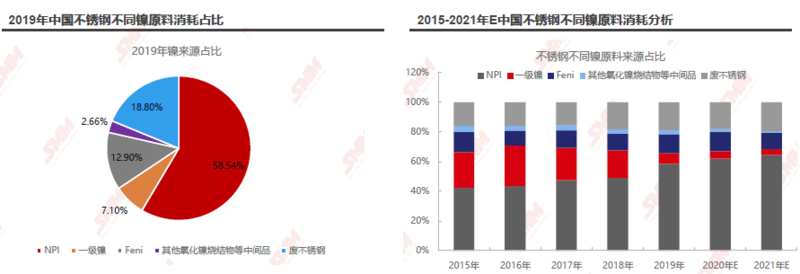

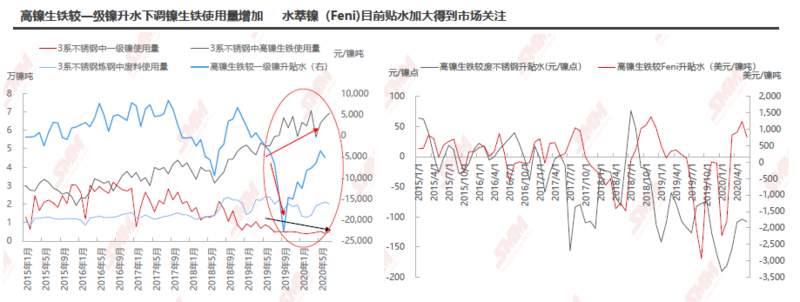

In the smelting of stainless steel, the main sources of nickel are: Feni (nickel content more than 15%, also known as water extraction nickel in China, hereinafter referred to as Feni), NPI, primary nickel, other intermediate products of oxidized sinter and nickel, and waste stainless steel.

With the rapid expansion of global nickel pig iron production, the use of nickel pig iron has been increasing since 2017. In 2019, stainless steel plants used more than 50% of nickel pig iron, while the use of pure nickel decreased to less than 10%. It is estimated that among the sources of nickel raw materials in 2020, the proportion of nickel pig iron consumption in stainless steel plants across the country will continue to increase, with an average proportion of more than 60%, while the proportion of pure nickel will drop to about 5%.

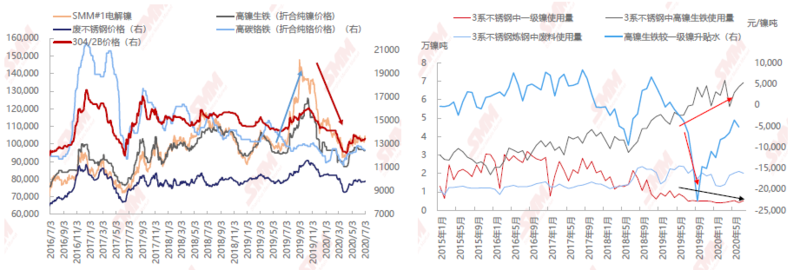

Comparison between the price of stainless steel and the price trend of various raw materials

Compared with the price trend of Ni-Cr raw materials, there is a greater correlation between the price of stainless steel and the price trend of nickel raw materials, among which the price correlation with high nickel pig iron is higher, mainly because the consumption of high nickel pig iron in 304 stainless steel is relatively large. Since the second half of 2019, the discount of high nickel pig iron has been gradually expanded compared with first-grade nickel, the economy has been greatly improved, and the usage has increased.

Economic comparison between High Nickel Pig Iron and Water-extracted Nickel (Feni) and scrap stainless Steel

Since the second half of 2019, the discount of high nickel pig iron has been gradually expanded compared with first-grade nickel, the economy has been greatly improved, and the usage in stainless steel production has increased. Recently, the discount range of imported Ferro nickel has been expanded, which has more economic advantages, which has attracted the attention of the market. However, due to the limited trade channels in the market, the usage of steel mills has not increased significantly at present.

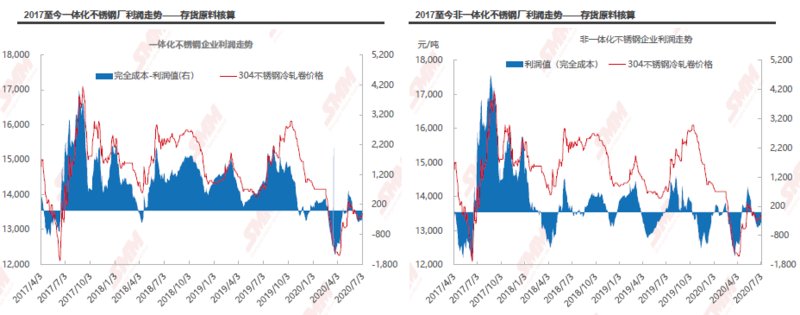

Analysis on the trend of cost and profit of stainless Steel

Analysis of Terminal consumption structure and supply-demand balance of stainless Steel

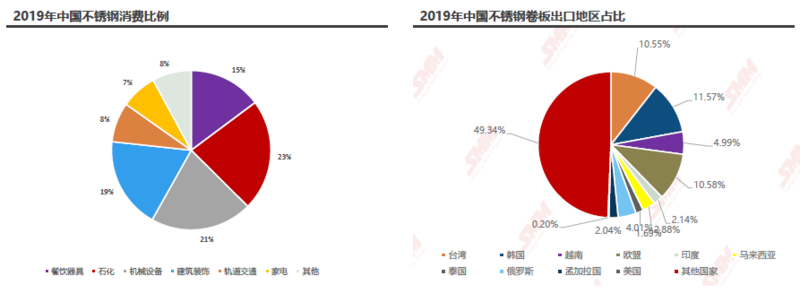

In 2019, petrochemical, mechanical equipment and architectural decoration are still the main consumption in the downstream of stainless steel, accounting for more than 60%, and catering utensils and household appliances account for about 30%.

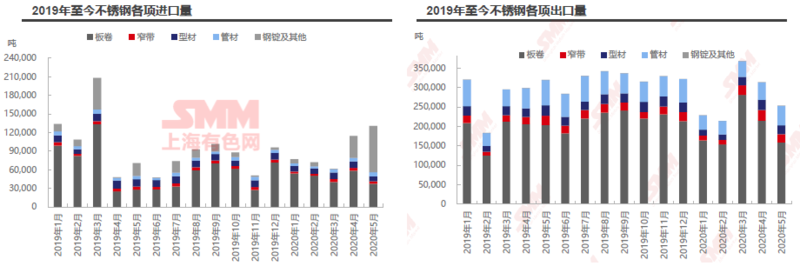

Analysis on the Import and Export of stainless Steel in China

According to 2019 data, coil accounted for an average of about 70% of stainless steel imports; in the first quarter of 2020, coil was still the main import force; since April, stainless steel imports have increased and the proportion of coil has gradually declined. this is mainly due to an increase in imports of stainless steel ingots and other categories from Indonesia, of which ingots and other imports reached 75000 tons in May. Stainless steel exports reached a peak in March 2020, due to the impact of the epidemic, the concentrated delivery of orders after the resumption of work in March, and then the export volume showed a decreasing trend, due to the impact of foreign epidemics and the delay of import and export orders. It is expected that the follow-up export volume may still decline to a certain extent.

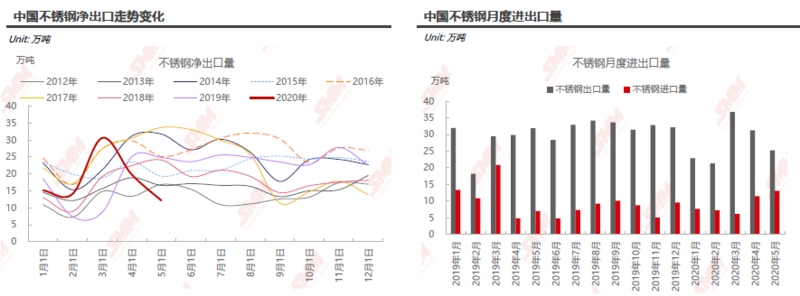

China's net export of stainless steel has a certain seasonal trend. since the fourth quarter of last year, due to the influence of domestic and foreign holidays, the export volume showed a decreasing trend, but began to recover gradually after the February-March holidays, and reached a high level in the second quarter. In 2020, due to the impact of the epidemic, exports reached a peak in March, with a large net export volume; on the other hand, Indonesia's imports of billets increased and exports decreased, which further promoted the downward trend of net exports.

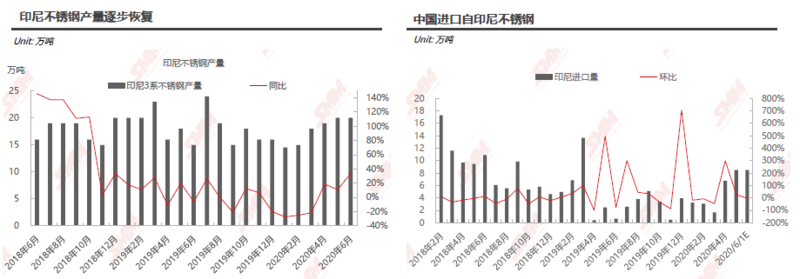

Production and import of stainless steel in Indonesia

Since 2020, Indonesia's stainless steel production has gradually increased, with an output of about 200000 tons in June. While imports of stainless steel from Indonesia gradually increased compared with the previous month, with stainless steel ingots and other categories increasing significantly, with an increase of nearly 40,000 tons, or 110%, in May. Although there are anti-dumping restrictions, stainless steel exported from Indonesia from China is mainly in the form of imported processing trade.

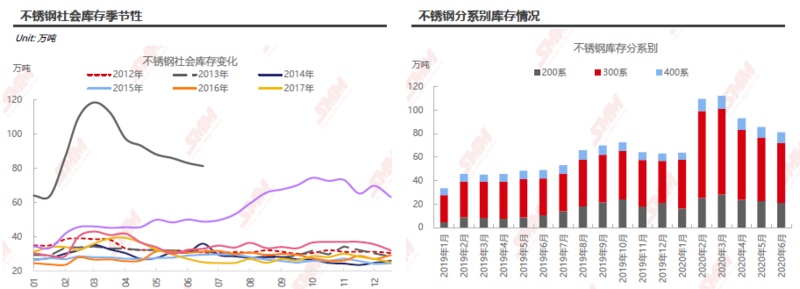

Social inventory of stainless Steel in China

The seasonality of stainless steel social inventory accumulation, in previous years, the accumulation of inventory is concentrated in the first quarter, and then the second quarter will gradually reduce the inventory. At the end of 2019, due to the contradiction that supply exceeds demand, inventory accumulated at a high level, while at the beginning of the year, inventory reached an all-time high of 1.1 million tons because of the epidemic. Since the second quarter, the recovery of market demand, superimposed steel production reduction in the first quarter, inventory continues to be in the trend of inventory reduction. As the output of most steel mills has returned to full production and the supply has increased, there is a traditional off-season of stainless steel in June / July, the demand is weak, the extent of warehouse reduction in June decreases obviously, and there may be a risk of base again in July and August.

The correlation of stainless steel social inventory

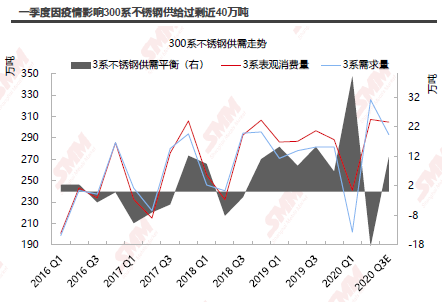

In the first quarter of 2020, due to the influence of the epidemic, the supply surplus of 300 series stainless steel reached a new high of nearly 400000 tons. After the resumption of work and production, the demand was greatly improved in the second quarter, the supply was in short supply, and the whole was in a state of de-stocking. However, when the steel mills gradually resume production, it is expected that there will be a small supply surplus again in the third quarter, but to a small extent. The total supply and demand of stainless steel is similar to that of 300 series, with a substantial surplus of nearly 500000 tons in the first quarter, a gap in the second quarter and a small surplus in the third quarter.

Summary

Raw material end: at present, in terms of the use of nickel raw materials in stainless steel plants, high nickel iron accounts for a relatively large proportion, while the supply of iron nickel is expected to be loose in 2020, and it is difficult for prices to strengthen in the third and fourth quarters, but due to the support of mineral prices, the weakening range of high nickel iron prices is limited, and high nickel iron prices are vulnerable to shock operation; high carbon ferrochromium prices are expected to show a slight downward trend in the second half of the year due to the impact of high chromium ore prices, so the domestic stainless steel cost may show a certain decline.

Supply and demand side: in the second quarter, some steel mills have resumed production, and domestic stainless steel production has gradually increased; Indonesian stainless steel production has been accelerated, and the return quantity has increased gradually, and the supply of stainless steel has increased; while the demand side has experienced a concentrated outbreak in March, gradually returning to dull, the demand growth rate is not as fast as supply, and the supply is still in a loose state in the second half of the year.

Price forecast: in the second half of 2020, under the condition of loose supply of stainless steel, the price is still cost support and demand-driven. It is estimated that the price range of cold-rolled stainless steel is 12800Mel 14000 yuan / ton.

Scan the QR code, apply for participation or join the SMM metal exchange group

![[SMM Nickel Flash News] Indonesia's ENC Project Set to Add New Battery-Grade Nickel Supply](https://imgqn.smm.cn/usercenter/CWsEw20251217171732.jpeg)

![[SMM Analysis] Indonesia's May Sulphur and Sulphuric Acid Import and Export Data](https://imgqn.smm.cn/usercenter/BdFZr20251217171712.jpg)

![[SMM Analysis] May Indonesia Sulphur and Sulphuric Acid Import and Export Data](https://imgqn.smm.cn/usercenter/ZsMtd20251217171723.jpeg)