SMM7 March 20: at the 2020 China Ni-Cr stainless Steel Industry Market and Application Development Forum held in SMM on July 20, Yu Wen, a senior analyst at SMM, looked forward to the market analysis and price of China's manganese ore and chromium ore in 2020.

The epidemic situation hinders the temporary development of China's economy but does not change the trend of long-term stability and improvement of our economy. In the progress of the times, the mode of trade is changing the market from the original income cost profit to a variety of profit models, such as brand profit, resource profit, leverage profit and so on. With the vigorous development of the bulk market, the era dividend represented by chromium and manganese, the small metal market is constantly learning to change from spot trading of finished products to spot, raw materials, futures and even more diversified operations.

SMM has regained its focus on these industries in terms of price impact, diversity of data and in-depth analysis, in line with the proud base metals of our company. Not only follow the pace of the market to look at the existing chromium market, but also look forward to the future of the chromium industry chain. Downstream stainless steel plants can still make profits such as upstream metal nickel spot and futures through resources and leverage under pressure on the profits of the main products.

On the other hand, the financial attribute of the Ferro-chromium market in the industrial chain has been greatly improved under the background of the future prospect of the listing of high-carbon ferrochromium in the last stock market. At the same time, under the background of China's sustainable economic development, the demand for infrastructure resources is increasing. The supply of a large number of products such as crude oil, thread, stainless steel and so on will continue to enlarge.

However, the original price dispute brought about by globalization will also become more and more serious. The pattern of oversupply in the end market may continue, while the upper reaches such as chromium alloy market in the process of continuous environmental protection suppression and backward capacity elimination, the market effective production capacity shows a shrinking trend and has a long history.

It is a great honor for SMM to share timely and effective information and data with the majority of relevant practitioners to learn and communicate with SMM soon before it goes on sale in the futures market.

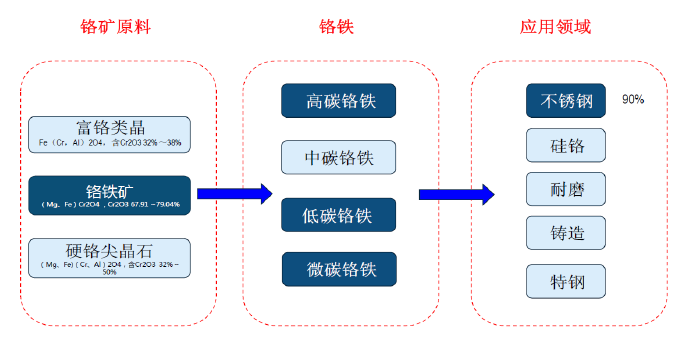

Stainless steel is the core of chromium market demand

The technology of domestic chromium industry is mature and stable.

Main uses of high carbon ferrochromium containing reproduced ferrochromium

(1) it can be used as alloying agent for ball steel, tool steel and high speed steel with high carbon content to improve the hardenability, wear resistance and hardness of the steel.

(2) it can be used as an additive to improve the wear resistance and hardness of cast iron, and make the cast iron have good heat resistance at the same time.

(3) used as chromium-containing raw materials for the production of silicon-chromium alloy and medium, low and low-carbon ferrochromium by slag-free process;

(4) used as chromium-containing raw material for the production of metal chromium by electrolysis;

(5) used as raw material for smelting stainless steel by oxygen blowing.

Smelting process

The smelting methods of high carbon ferrochromium include blast furnace, electric furnace, plasma furnace and so on. The use of blast furnace can only produce special pig iron with about 30% chromium. At present, most of the high-carbon ferrochromium with high chromium content are smelted in ore reheating furnace by flux method. The basic principle of smelting high carbon ferrochromium by electric furnace process is to use carbon to reduce chromium and iron oxides in chromium ore.

The starting temperature for the reduction of chromium oxide to Cr2C2 by carbon is 1373K, the starting temperature for the formation of Cr7C3 is 1403K, and the starting temperature for reduction to chromium is 1523K, so the carbide of chromium, not metal chromium, is obtained when carbon is reduced to chromium ore. The carbon content in ferrochromium depends on the reaction temperature. It is easier to form carbides with high carbon content than to form carbides with low carbon content.

Raw materials for smelting high carbon ferrochromium

The raw materials for smelting high-carbon ferrochromium are chromite, coke and silica. The content of Cr2O3 ≥ 40 Cr2O3/ ∑ FeO ≥ 2.5S < 0.05P < 0.07MgO and Al2O3 in chromium ore should not be too high, with a particle size of 10 70mm. In the case of refractory ore, the particle size should be smaller.

Coke is required to contain not less than 84% fixed carbon, ash less than 15 S < 0.6%, and particle size 320mm. Silica is required to contain SiO2 ≥ 97 Al2O3 ≤ 1.0%, good thermal stability and 20 80mm particle size without soil.

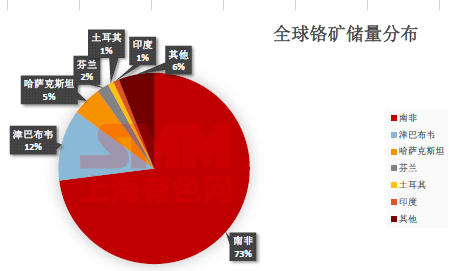

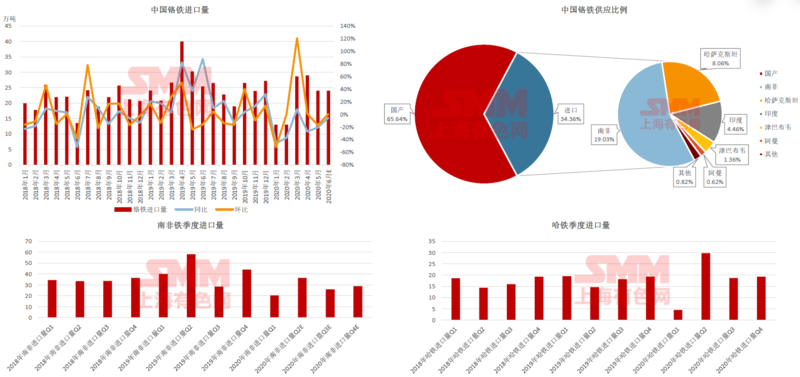

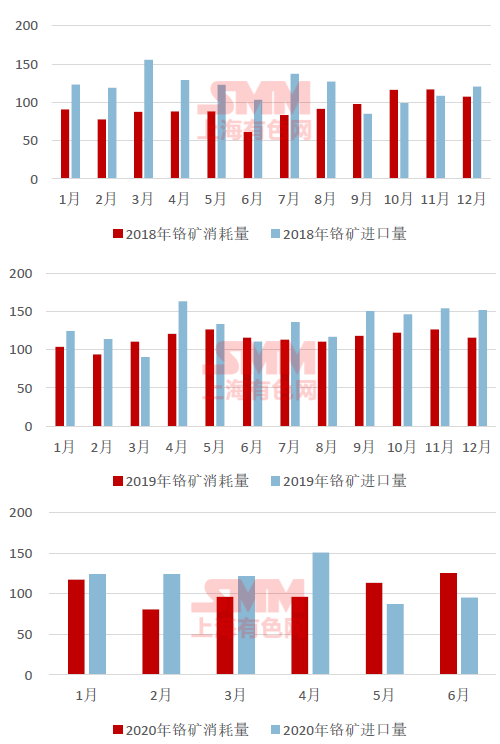

South Africa has the largest chromium ore reserves in the world and China imports the first.

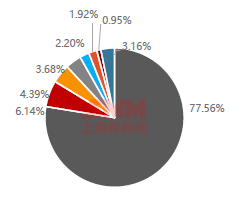

Distribution of China's Chromium Ore Import in 2019

Review and expectation of downstream demand in Chromium Market

The supply and demand side: in the second quarter, some steel mills have resumed production, and the domestic output of stainless steel has gradually increased; the production of stainless steel in Indonesia has been accelerated, and the amount of returning stainless steel has increased gradually, and the supply of stainless steel has increased; while the demand side has experienced a concentrated outbreak in 3.4 months, it has gradually returned to flat, the growth rate of demand is not as fast as supply, and the supply is still in a loose state in the second half of the year.

Price forecast: in the second half of 2020, under the condition of loose supply of stainless steel, the price is still supported by cost and led by demand. The price range of cold-rolled stainless steel is expected to be 12800 14000 yuan.

The demand for high-carbon ferrochromium is expected to increase during the year when downstream stainless steel production resumes.

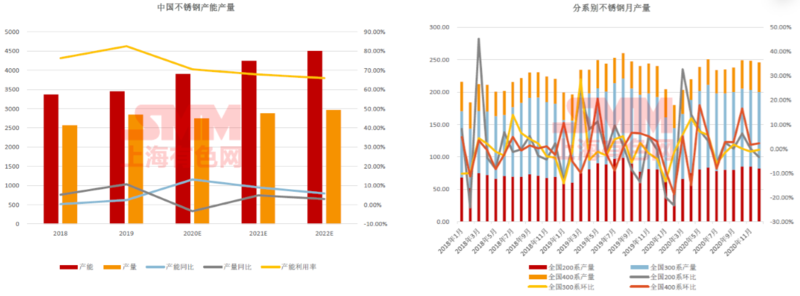

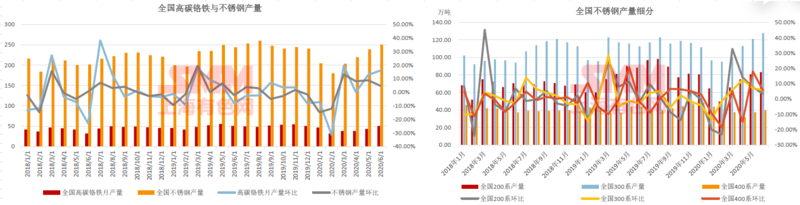

The output of high carbon ferrochromium and stainless steel are periodic.

China's stainless steel production capacity showed a low growth rate in 2018 and 2019, on the one hand, the negative impact of the rise of the Indonesian stainless steel industry on Chinese manufacturers; on the other hand, the economic growth rate has shifted from high-speed to "medium-high-speed" growth, such as the Chinese real estate market and the automobile industry, which has led to a slight decline in the growth rate of China's stainless steel consumption, falling to 4.5% in 2019. SMM estimates that the planned new production capacity of stainless steel in China will be about 16.5 million tons in the next three years, and the actual progress of production depends on the funds of the steel mills and the replacement of the actual capacity. The red delivery of raw materials is still the main competitiveness of the development of steel mills.

The overall stable output of stainless steel from July to December 2020 and the overall trend of demand for high-carbon ferrochromium

From January to June 2020, stainless steel production decreased by 4.5% compared with the same period last year. According to SMM, the year-on-year decline in stainless steel production in 2020 was reduced to 3.3%. The demand for China's high-carbon ferrochromium market continues to pick up.

The output of stainless steel is expected to decrease first and then increase from July to December 2020. The national output of stainless steel row is reduced due to the accumulation of routine maintenance and social inventory in stainless steel plants in July, but with the market recovery and periodic increase, the demand trend of high-carbon ferrochromium is expected to show a steady trend.

From June to December 2020, the total demand for high-carbon ferrochromium was 4.6919 million tons, with an average monthly demand of about 782000 tons, a cumulative decrease of 1.19 percent over the same period last year and an increase of 15.63 percent over the first half of the year. The trading volume between high-carbon ferrochromium manufacturers and imported ferrochromium manufacturers may continue to increase.

The supply of domestic high-carbon ferrochromium may be insufficient to restore the supply of imported ferrochromium.

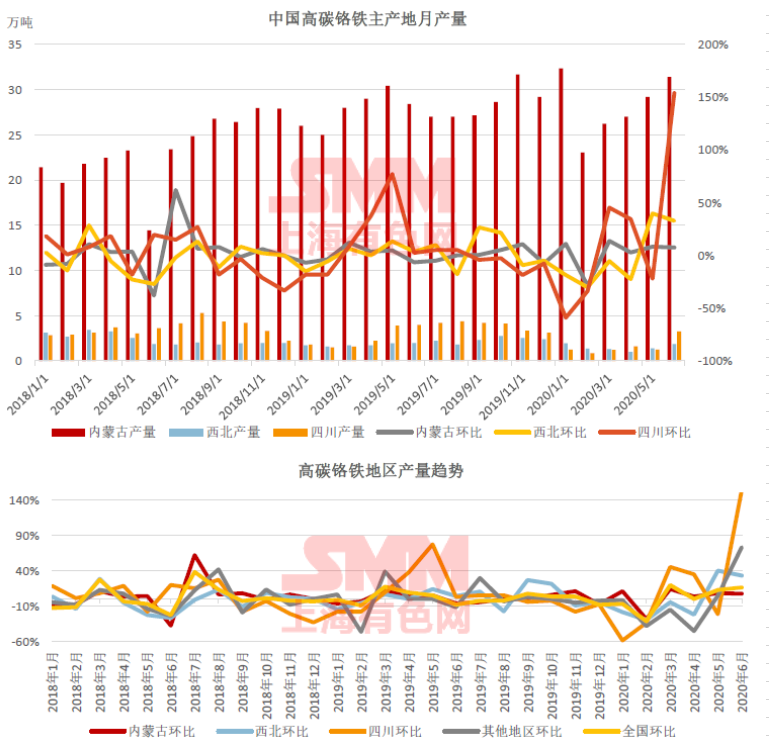

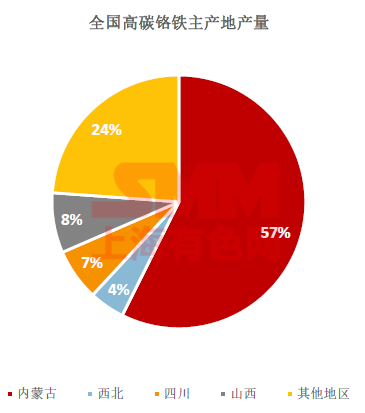

From January to June 2020, the domestic production of high-carbon ferrochromium decreased by 15% compared with the same period last year, and the continuous national output of high-carbon ferrochromium in Inner Mongolia accounted for about 57%, and dominated the national output of high-carbon ferrochromium during the month. Because of the difference of statistical caliber and data coverage between main producing areas and non-main producing areas in China, Inner Mongolia can be used as a reference index for future and following research in the correlation analysis of output.

The import of ferrochromium has maintained a long-term growth trend.

Uncertainty in short-term supply of ferrochromium in South Africa

Glencore holds a 79.5% stake in Glencore Merafe Chrome Venture and invests in the following mines and smelters:

The Helena Magareng and Thorncliffe chromium deposits are located in the eastern limb of the Bushveld igneous rock group.

The Waterwall and Crondale chromite deposits near Rustenburg on the western margin of the Bushveld igneous rock group

Rietvly Silicon Mine, opencast mining, ferrochromium smelter with different technologies is located near Rustenburg.

Boshoek Wonderkop and Rustenburg smelters near Rustenburg using Otto Kunpu technology

Use of Premus technology at Lion and Lydenburg smelters near Steelpoort and Lydenburg, respectively

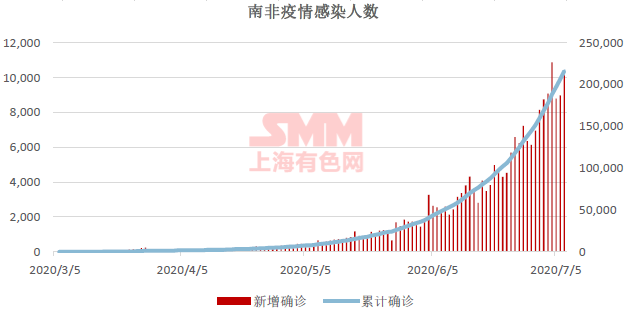

Whether the blockade policy of South Africa ushered in the second wave

South African officials set their first forecast for the outbreak peak in early June; the second forecast changed the outbreak peak from late August to early September, and the South African government is still calling for stricter blockade regulations in opposition parties and regions such as Gauteng province. SMM believes that South Africa still has a comprehensive national blockade or regional restrictions in August to deal with the outbreak peak.

A list of new capacity in Indonesia from the end of 2019 to 2020

From January to August in 2018, chromium ore inventory is on a rising trend. According to domestic factory production, even if the downstream alloy plant is operating well, the port inventory has not been effectively consumed due to the fact that the import of chromium ore has been greater than the consumption of chromium ore. At the end of August, the inventory of chromium ore in the country's major ports even reached 3.83 million tons, a record high. Until September, the import of chromium ore was only 850000 tons, and the arrival of domestic chromium ore to the port reached the lowest level in nearly three years. Coupled with the gradual recovery of factories in environmental protection production restrictions, and at the same time actively preparing stocks for double sections, the chromium ore inventory in the main ports of the country was rapidly consumed. The port inventory of chromium ore returned to the prefix ".

The overall chrome mine port inventory is stable in the first half of 2019. Since late March, the spot inventory of chromium ore has been basically maintained at 270000 tons. Compared with the increasing inventory last year, the supply of chromium ore this year is basically balanced with the consumption of chromium ore. In recent years, with the development of the market, more and more alloy factories choose to import futures independently or cooperate with fixed chromium ore traders. The difficulty of operation increases, resulting in the reduction of the operation volume of pure chromium ore traders, most of the port chromium ore inventory is factory stock, and the function of trader reservoir is gradually reduced.

In the second half of 2019, the national port inventory increased slowly, the monthly imports of chromium ore increased and the off-season consumption of stainless steel plants overlapped, and the chromium ore inventory was difficult to digest. From August 23 to November 8, the national port inventory increased for 10 consecutive weeks, and on October 18, the national port inventory exceeded 3 million tons, a record. After the first slight decline in stocks on November 15, the inventory continued to increase, with a maximum inventory of 3.48 million tons.

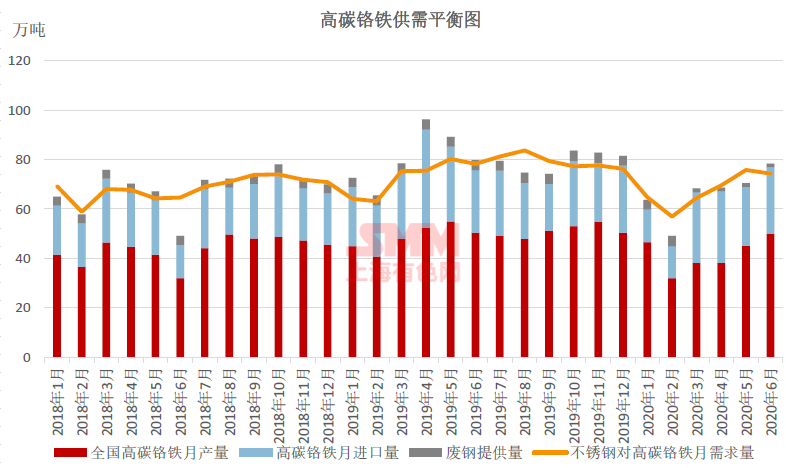

2018-2019 High carbon Ferro Chromium concussion downward trend of supply and demand shows repair trend in 2020

China's high-carbon ferrochromium market is in a relative surplus in 2018, although the central environmental supervision swept most of the main producing areas of ferrochromium in China in June, and the factory shutdown and production reduction seriously affected the output of domestic ferrochromium, however, the amount of chromium metal provided by overseas high-quality high-carbon ferrochromium is enough to maintain the demand for stainless steel. after environmental supervision, high profits drive manufacturers to resume production in large quantities, and the market once again shows a market situation in which supply exceeds demand.

The supply and demand of high-carbon ferrochromium increased significantly in 2019. The total supply of domestic and imported high-carbon ferrochromium was 9.1064 million tons, an increase of 14.25 percent over 2018. China's consumption of high-carbon ferrochromium in 2019 was 8.6427 million tons, an increase of 8.91 percent over 2018. In the case of the original surplus of high-carbon ferrochromium, the growth rate of high-carbon ferrochromium is still higher than the growth rate of consumption, and the oversupply has intensified, with a surplus of 268400 tons of high-carbon ferrochromium for the whole year. An increase of 187.67% over 2018.

The supply and demand pattern of high carbon ferrochromium is expected to be greatly improved by the end of 2020.

The output of downstream stainless steel has increased significantly since April, while the operating rate of domestic high-carbon ferrochrome in that month was only 48.6%. On March 26, due to the national blockade imposed by South Africa and other countries due to the epidemic, the supply of imported ferrochrome and chromite decreased by more than 20% compared with the same period last year. And the South African government expects to enter the outbreak period in September, when the supply of South African ferrochrome and chromite may be under pressure again.

High-carbon ferrochromium under the influence of the epidemic, SMM believes that domestic production of high-carbon ferrochromium and imported ferrochromium showed negative growth in 2020, and the supply of high-carbon ferrochromium was in short supply at the end of the year, which was 213400 tons per month, significantly repairing the structure of oversupply in 2019.

Scan the QR code, apply for participation or join the SMM metal exchange group