SMM7: at the 2020 (Fifth) China International Nickel-Cobalt-Lithium Summit Forum and China International Conference on New Energy Lithium Materials held by SMM, Liu Bowen, head of the Research and Development Department of Shandong Haike Chemical Group Co., Ltd., said that the development and opportunities of the industry were analyzed from the perspective of lithium battery electrolyte solvents.

New energy vehicles enter the stage of accelerated development

Mr Liu said the epidemic affected European and domestic markets; demand for Q2 bottomed out in 2020, but sales of electric cars rose sharply in the second half of the year under incremental indicators and subsidies in first-tier cities such as Beijing.

"with a low opening and a high rise in 2020, the epidemic affected sales of 450000 units, with an estimated global sales of 2.7 million units, an increase of 20 percent; a domestic forecast of 1.28 million units, an increase of 6 percent, and an increase of 1.42 million units abroad, an increase of 35 percent.

In 2021, with double credits and carbon emissions policy, global sales are expected to be 4 million units, an increase of 47%, domestic units are expected to be 1.82 million units, an increase of 42%, and 2.15 million units abroad, an increase of 43%.

In 2025, global sales of electric vehicles are expected to be 13.78 million, with a domestic electrification rate of 6.23 million and a domestic electrification rate of 20 per cent, while 7.55 million abroad and a European motorization rate of 22 per cent.

Lithium battery has been improving for a long time.

2020 A bad start in the short term: the power battery affected by the COVID-19 epidemic is expected to increase by 16%, and the 3C mobile phone battery is expected to increase by about 20%.

2020 growth highlights: energy storage ESS, is expected to be supported by 5G energy storage 9GWH, side electricity and optoelectronic storage, and UPS, with a compound growth rate of 20%.

On the eve of the outbreak of electrolyte demand

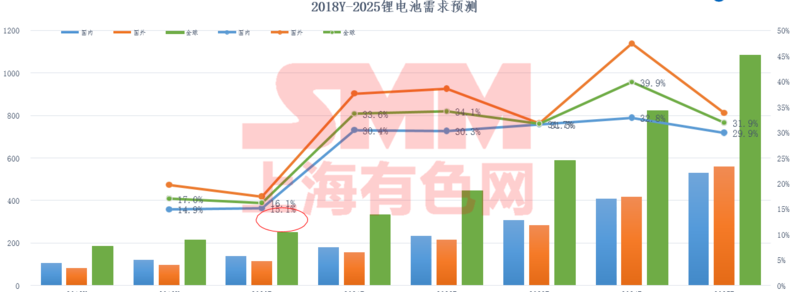

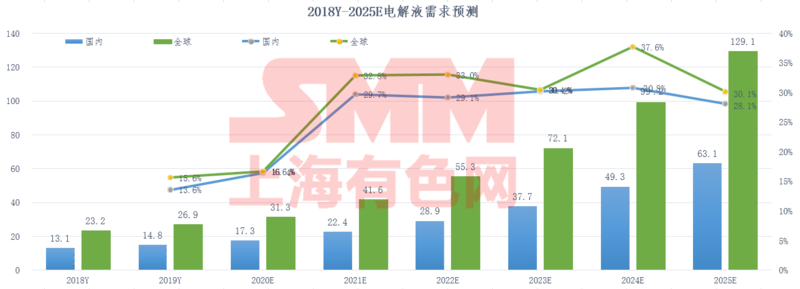

Liu Bowen said that in 2020, the global demand for electrolyte is about 313000 tons, a growth rate of about 16.7 percent; domestic demand is 173000 tons, a growth rate of 16.4 percent; from 2021 to 2022, the demand for lithium batteries is growing rapidly, with a domestic growth rate of more than 30 percent and about 533000 tons in 2023. The demand for lithium batteries abroad is expected to grow by more than 33 percent, and the demand is expected to be concentrated in Europe, with an estimated 180000 tons.

From 2019 to 2025, the average annual compound growth rate of lithium batteries is about 30% at home and about 33% abroad, and the market potential in Europe and the United States is huge.

The demand for solvents is growing steadily.

In 2020, solvent demand is affected by the slowdown of electric vehicles and the weakening demand for digital batteries, which is expected to grow by only 15.7%; but the demand for LFP batteries and energy storage will grow rapidly by 25%; it is estimated that the demand for solvents in 2023 will be 560000 tons, and the demand for electronic EMC, electronic EC and electronic DMC will increase by more than 30%. In 2025, the demand for solvents will be 1 million tons. Tesla-Panasonic, CATL, LG, SKI, and SDI industry chains lead the demand for electrolyte solvents.

Analysis of electrolyte and solvent industry

The concentration of the global lithium battery industry is 71%, and the concentration of the electrolyte industry is 73%. LG Chem is developing rapidly; the oligopoly competition pattern of the electrolyte industry is leading the development of the industry by Tianji, New Zebang and Cathay Pacific; the development of electrolyte benefits from overseas markets, and the overseas market increases by more than 30%.

2020 A bad start in the short term: the power battery affected by the COVID-19 epidemic is expected to increase by 16%, and the 3C mobile phone battery is expected to increase by about 20%.

2020 growth highlights: energy storage ESS, is expected to be supported by 5G energy storage 9GWH, side electricity and optoelectronic storage, and UPS, with a compound growth rate of 20%.

In 2020, the domestic demand for lithium batteries is about 137GWH, driven by small power and 5G energy storage, with a growth rate of about 15%; foreign demand for lithium batteries is about 113GWH, with a growth rate of about 17%; and the global demand for lithium batteries is about 249GWH, with a growth rate of about 16%.

Conclusion

Liu Bowen said that since the beginning of this year, affected by the epidemic, the growth of the electric vehicle and lithium-ion battery industry has lagged to some extent, but does not change the long-term high growth trend. Lithium-ion battery is still the most feasible way of energy storage at present, and the market life cycle of carbonate as a mainstream solvent can be expected to be 8 Mel 10 years. Although it has been 30 years since the commercialization of lithium batteries, it is still a new thing to be used in electric vehicles, including a lot to be improved.

Scan the code to apply to join the SMM Cobalt and Lithium Industry Exchange Group