"SMM Zinc Industry chain Weekly report" released, the weekly report SMM will select the hot topics, prices, market or major changes in the industry chain information released into a document for your reference.

The following is an excerpt from the weekly report of the zinc industry chain:

Zinc market forecast next week: in terms of Shanghai zinc, the domestic stock market rose brightly this week, leading to a pick-up in macro sentiment in the market, hot money pushed a strong rebound in non-ferrous metals, and zinc prices basically deviated from fundamentals in the second half of the week. But on Friday, it was reported that the United States will resume imposing 25% tariffs on some Chinese goods, and Sino-US trade relations still sow a lot of uncertainty to the macro mood. From the perspective of next week, the fundamentals of zinc in Shanghai are still weak. On the supply side, smelters such as Tongguan in Anhui, Sanli in Hunan and Taifeng in Hunan have been overhauled and normal production has resumed. Superimposed zinc prices have returned to high levels in the first half of the year, and smelters are willing to ship goods. The overall pressure on the supply side is on the high side. On the consumer side, under the high zinc price, most downstream enterprises mainly consume inventory, hold a wait-and-see attitude to the price, and their willingness to buy is very weak under the influence of the off-season of domestic consumption. orders are also slightly weaker than the previous month, the overall market demand is poor, and there is still no support from a fundamental point of view. From a technical point of view, Shanghai zinc jumped on the Brin Road, it is expected that there will be some bullish exit next week, zinc prices may have a certain pullback, but the support of the Qiqi pass is still strong. Next week, we still need to pay attention to the impact of Sino-US relations and the epidemic in Kazakhstan on macro-sentiment. Overall, next week, Lun Zinc is expected to run at US $2,180 per ton at 2120Mel; 2008 of the main contract for Shanghai Zinc is expected to run at RMB17,250,17,850 per ton, and the spot side is expected to raise water at around RMB40 per ton in August.

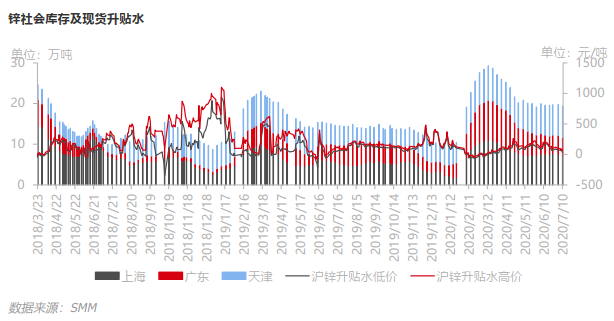

Import profit and loss: RMB appreciation, import loss narrowed. As of Thursday, the average Shanghai-Lun ratio this week was 8.27, slightly lower than last Friday, the average import loss narrowed by 70 yuan / ton to 360 yuan / ton compared with last week, and the import window remained closed. This week, the spot market has SMC, AZ circulation, compared with domestic to maintain a discount of 10 Murray 30 yuan / ton level. Domestic epidemic control is better than overseas, and the pace of economic recovery is also better than domestic. The sharp appreciation of the RMB this week has significantly narrowed import losses, but domestic smelting output is expected to increase month-on-month, and domestic zinc fundamentals are still weak in the short and medium term. Based on the current domestic inventory levels and production expectations, domestic demand for imported zinc is relatively small, fundamentals do not catalyze the import window to open, and it is expected that the short-term import window will remain closed.

"apply for free access to the SMM metal industry chain database

Catalogue of "SMM Zinc Industry chain Weekly report" in this issue

Main points of this weekly report: processing fees, import profit and loss inventory

Hot spots in the zinc industry: what is the story of the fundamentals outside the macro promotion of a strong breakthrough in zinc through the Qiqi pass?

Zinc concentrate market: smelter raw material inventory rises domestic zinc concentrate processing fees remain stable

Refinery dynamics

Import Zinc Market: RMB appreciation, Import loss narrowed

Zinc City predicts next week: there are hidden dangers in Sino-US relations. Shanghai Zinc may have a pullback next week.

Zinc market review: market risk appetite increases, zinc prices in the two cities rise sharply

Galvanizing: off-season may spread weak orders for galvanized structural parts in July

Die-casting zinc alloy: the price of raw material zinc ingot rises rapidly and the demand of die-casting zinc alloy factory is poor.

Zinc oxide: zinc oxide starts flat zinc price pulls up procurement is suspended

Scan the QR code application report for free and join the SMM copper industry chain exchange group

[China Zinc Industry chain High-end report] SMM exclusive monthly survey of zinc industry chain report, covering from zinc concentrate to zinc primary consumer operating rate and supply and demand profile. And announce the exclusive monthly zinc concentrate, refined zinc balance, continue to track the industry entity enterprises, update data. And through the supply and demand situation and data model to make a simple prediction of the future trend of zinc. "View details

![Kẽm Thượng Hải: Giá kẽm tương lai SHFE củng cố ở mức cao, các doanh nghiệp hạ nguồn vẫn thận trọng [Bình luận giữa ngày SMM]](https://imgqn.smm.cn/usercenter/nlmjY20251217171755.jpg)

![Kẽm Ninh Ba: Doanh nghiệp hạ nguồn tiếp tục thận trọng, giao dịch kẽm giao ngay ảm đạm [SMM Điểm tin giữa ngày]](https://imgqn.smm.cn/usercenter/qTzTI20251217171754.jpg)