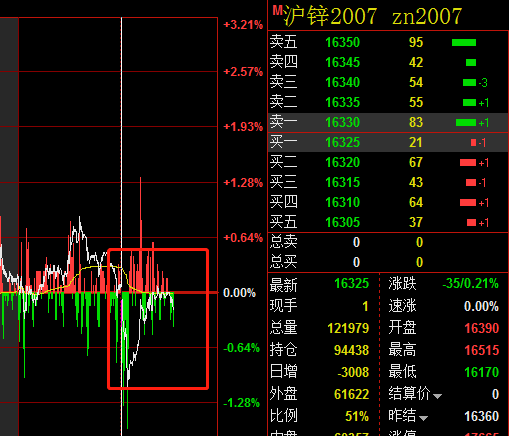

SMM5 March 25: affected by the frequent news of Sino-US relations and the fact that the government work reports of the two sessions did not set a target for economic growth, zinc prices continued to decline at the start of trading today. Today, the main contract for zinc in Shanghai fell to 16170 yuan / ton. As of 11:20 today, it was tentatively reported at 16325 yuan / ton, a decline of 0.21%.

In terms of fundamentals, domestic zinc concentrate processing fees have continued to decline since late February. As of the week of May 22nd, the TC of domestic zinc concentrate was 5100 yuan / metal ton. With the continuous decline of processing fees, the superimposed zinc price has been repaired compared with that after the Spring Festival, so that the profits of mines have been restored, the willingness of most mines to ship goods has improved, and the shortage of raw materials in smelters has been gradually alleviated. On the supply side, although some smelters carry out maintenance, the actual impact is concentrated in June, and some smelters have postponed the original maintenance time. At present, the average raw material inventory of the smelter is more than 20 days. As follow-up shipments from Russia and Australia arrive at the port one after another, the problem of tight raw material supply is basically alleviated, and follow-up attention is paid to the maintenance of smelters.

On the consumer side, galvanizing, large enterprises still maintain a high operating rate, and terminal consumer orders will remain stable. However, due to the early rush orders are basically completed, the recent orders are worse than before. In terms of die-casting zinc alloy and zinc oxide, the current overseas orders have not improved significantly, the pull of domestic demand is relatively limited, and the overall performance is still poor. Recently, the two sessions have proposed to strengthen the new infrastructure, but it will take some time for the specific transmission to the order side. Generally speaking, the fundamental support is weak in the short term, but the early short positions may lead to a slight correction in zinc prices. Follow-up attention will be paid to the guidelines brought by the policies of the two sessions.

Focus on the development prospect and price trend of lead and zinc industry

In 2019, global trade disputes escalated, the global economy was under pressure, and central banks began a wave of interest rate cuts. At the same time, the meeting of the political Bureau of the CPC Central Committee stressed that at present and for some time to come, the basic trend of China's economic stability and long-term improvement will remain unchanged, and 2020 will also be the year when China will build a moderately prosperous society in an all-round way and the 13th five-year Plan ends. In this context, the new crown virus is rampant all over the world, and it is worth looking forward to how to achieve steady economic growth.

In the zinc market, the production of overseas mines increased step by step in 2019, but the production of domestic mines was repeatedly hindered. In the first quarter of 2020, zinc prices fell below the mine cost line, and mine profits plummeted. How will the profits of smelters and mines be distributed in 2020? can overseas mines be expected to be put into production under the disturbance of the epidemic? In addition, the output of domestic zinc refining smelters broke through the bottleneck and set a new record in 2019, but under the disturbance at the supply end of zinc mines in 2020, can the capacity utilization rate of smelters maintain a high load? Whether the infrastructure investment under the tone of "stabilizing the economy" in 2020 can exceed the expected performance, whether the galvanizing industry can exceed the seasonal performance is still worth looking forward to, and the contradiction between supply and demand of zinc may be reversed in 2020, so paying attention to and distributing structural opportunities is another choice. Can zinc prices fall and rise in 2020?

In response to the above topics, SMM will invite industry celebrities, industry professionals, enterprises from the upper and lower reaches of the industrial chain to hold the "2020 (15th) lead and Zinc Summit" in Changsha to jointly discuss the current situation and problems of the industry, as well as the future development prospects, and analyze the fundamentals and the future trend of zinc prices.

Click to sign up for SMM 2020 (15th) lead and Zinc Summit

Scan the QR code in the picture to sign up for the lead-zinc summit and fill in the personal information on the last page. The meeting staff will contact you later!