SMM: in April, with the decline in the rate of increase in new cases around the world, market sentiment has picked up, a number of overseas countries announced that they will restart the economy one after another, Shanghai zinc rebounded after a sharp decline, as of today, the Shanghai zinc index closed at 16295 yuan / ton, up 7.42 percent within the month. Looking ahead to May, SMM believes that zinc prices still have a strong support.

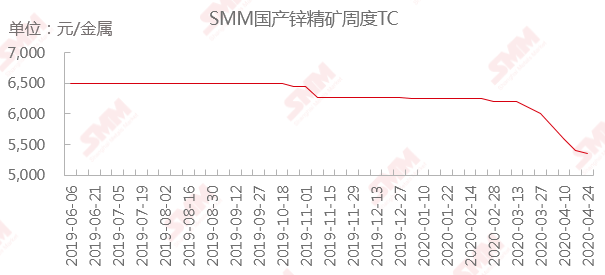

In April, the overseas epidemic is still fermenting, coupled with Peru and other countries once again extended the ban time, the supply of overseas mines has not been restored, the supply of imported mines is still tight. However, due to the heavy fall in zinc prices, seriously squeezing domestic mine profits, reducing production in some mines, and controlling sales in some mines, according to SMM research, the TC of domestic zinc concentrate in April was 5750 yuan / metal ton, down 350 yuan / metal ton compared with March. It is expected that there is still room for a reduction in short-term processing fees, and follow-up attention will be paid to the recovery of overseas mines.

"apply for free access to the SMM metal industry chain database

On the supply side, in April, smelters mainly resumed production and increased production, while due to the shortage of raw materials in domestic smelters and other problems, some refineries chose to overhaul in advance and concentrated in May-June. Taken together, the supply of refined zinc is still abundant in the short term, and the reduction in May-June is expected to be reflected.

"apply for free access to the SMM metal industry chain database

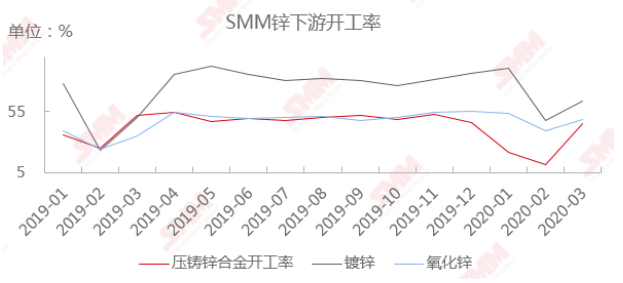

On the consumer side, in terms of galvanizing, some large galvanizing enterprises reached full capacity production in April, the pressure of superimposed finished product inventory was alleviated under the price reduction, and the demand for orders was significantly better than before. However, die-casting zinc alloy and zinc oxide plate due to export orders blocked, order demand fell significantly, die-casting zinc alloy enterprises in April orders fell by nearly half compared with March, zinc oxide orders in April were almost the same as in March.

In terms of zinc terminal consumption infrastructure, according to SMM research, the current resumption rate of projects under construction at the terminal site is 93.2%. Among them, the actual operating rate of the infrastructure industry reached 94.5%, an increase of 34.7% over the end of March. And the state strongly supports infrastructure, which is conducive to boosting the consumption demand of zinc terminals.

In real estate, investment in real estate development across the country totaled 2.1963 trillion yuan in the first quarter, down 7.7 percent from a year earlier, down 8.6 percent from January to February and narrowing the decline in investment in real estate development, according to the Bureau of Statistics. The central government has always adhered to the principle of "housing does not speculate" and has made clear the general direction of real estate market policy in the future. At present, there is no overheating in China's real estate market. In the future, the supply and demand of real estate will be released synchronously, and the overall real estate will still operate moderately.

In terms of cars, according to the data of the China Automobile Association, China's automobile production and sales reached 1.422 million and 1.43 million respectively in March, an increase of four times and 3.6 times over the previous month. With the gradual landing of the national automobile stimulus policy, the future automobile market may pick up somewhat.

SMM expects that in May, some refinery maintenance will affect the supply increment, but because the current inventory level is still high, and the previous inventory reduction is essentially the transfer from social warehouse to other warehouses and downstream inventory, the actual consumption may not be optimistic, and still rely on galvanized structure enterprises as a whole. Affected by the resumption of highway tolls in May, perhaps some downstream enterprises will replenish the warehouse in advance, but the subsequent consumption of inventory pressure is still relatively large. In the short term, zinc price fundamentals are mainly supported by the supply side, consumer increments still need to pay attention to whether galvanized orders can be sustained, and whether alloy enterprises can pick up.

"Click to sign up for SMM" 2020 (15th) lead and Zinc Summit

Scan the QR code to sign up for the lead and zinc summit and fill in the personal information at the end of the page, and the conference staff will contact you later!