Non-ferrous

Non-ferrous

Base Metals

Rare Earth

Scrap Metals

Minor Metals

Precious Metals

New Energy

Price CenterDatabaseProReportsEventsCar Insight

Language:

Language:

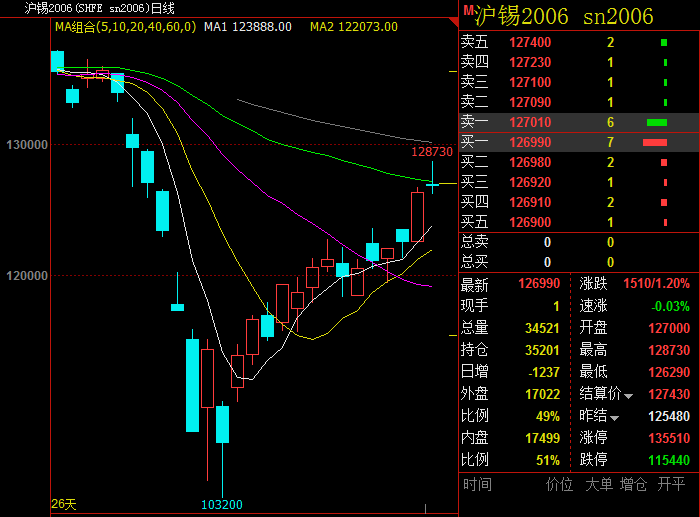

SMM4 13: April 13, Shanghai tin continued the recent trend continued to rise, as of the end of the day, Shanghai tin main contract 2006 closed at 126990 yuan / ton, an increase of 1.2%. After a sharp fall in late March (23 March), tin prices began to recover gradually. Today, Shanghai tin rose to 128730 yuan / ton, the highest since March 16.

On the supply side, many tin producers have recently announced that they will cut production or stop production. Tianma, the world's largest tin producer, announced that it would delay some exports in March after the outbreak, cutting production by 20 to 30 per cent while measuring global demand. JFX sales fell 38 per cent in March from a month earlier to 4605 tonnes. Sales of refined tin fell in March through Jakarta Futures Exchange (JFX), Indonesia's main tin exchange, after Tianma announced a cut in production. Alpha Ming's tin concentrate production fell 5 per cent in the first quarter, with total concentrate production of 2119 tons in the first quarter, down 116 tons from the fourth quarter of 2019. In addition, (MSC), the Malaysian smelting group, and Minsur of Peru, the world's third and fourth largest refined tin producers, have recently announced a moratorium on production. AfriTin Mining of Namibia and Minera ã o Taboca, a subsidiary of Minsur in Brazil, also suspended production after Indonesian tin miner PT Timah announced a temporary cut in production and delayed exports, as did Bolivia's EM Vinto.

Raw material market, according to SMM research, the recent import of tin ore is still in a tense state, at present, the West Mine raw material quotation and shipment volume is less, processing fees, recently due to the smelter demand for tin ore is different, the actual transaction price also has different fluctuations. In terms of inventory, according to the SMM survey, the invisible inventory of domestic smelters in March increased by 11% compared with February, mainly because the previous February retained relatively more inventory, most of the enterprises produced normally in March, and the output increased compared with the previous period, and since the middle and late March, the purchasing will of downstream enterprises and traders is weak, and the market as a whole is generally weak, resulting in the high hidden inventory in March. Overall, domestic smelter inventories rose in early April from the previous month.

On the production side, SMM data showed refined tin production of 12000 tonnes in March, up 59.9 per cent from February. The obvious increase in refined tin production in March over February is mainly due to the limited production time of some refineries affected by the epidemic situation during the Spring Festival holiday in February, resulting in a relatively small base of refined tin production data in China. In March, most refineries gradually resumed production, and some of the raw materials before the Spring Festival finished tin ore inventory imported into China, refined tin production has been significantly increased. However, as the overall operating rate of Myanmar's tin mining enterprises remains relatively low, the continuity of short-term tin supply remains to be seen, and some refineries affected by tin supply say that there may be a reduction in production in April. Refining tin production is expected to shrink to around 11000 tons in April.

Institutional point of view:

Jinrui Futures

Medium-and long-term contradiction: the degree of decline in the output of Burmese mineral resources.

Short-term contradiction: the impact of the spread of the epidemic on short-term refined tin consumption.

Viewpoint: the decline in the number of new outbreaks overseas last week has caused panic in the market to repair, and the current price rebound is more driven by short-term supply contraction at home and abroad. On the one hand, overseas production cuts are obvious, with South America accounting for about 12% of global production and Southeast Asia accounting for 30% of global production. On the other hand, raw material factors increase the maintenance of domestic refineries. The closure of some ports and restrictions on the movement of people in Myanmar have led to a decline in tin exports. Short-term supply disturbances exacerbate price volatility, but we need to focus on the demand side. With the spread of overseas outbreaks and some export-oriented downstream, orders have fallen significantly, and leading domestic contract factories have closed some factories or reduced hiring. Therefore, in the later stage, on the one hand, we need to pay attention to the implementation of production cuts, on the other hand, the epidemic will drag on demand for a long time. We think that the rebound in tin prices should not be overly optimistic.

Investment strategy: it is appropriate to wait and see, as production cuts stimulate price rebound to be further implemented, consumption drag or duration is longer.

Founder medium term futures

As the epidemic in Europe and the United States approaches the inflection point, market sentiment triggered by demand expectations continues to warm and tin prices continue to repair. On the supply side, tin mine imports still have the problem of supply constraints, smelter raw material supply is facing a tight situation, some refineries are considering reducing or suspending production in response to this situation; tin mining enterprises have stopped production one after another, tin mine resource countries or ushered in the peak of the epidemic to continue to lower supply expectations, supply-side tightening will support tin prices; tin stocks in the previous phase continue to decline. Supply, demand and inventory are all conducive to the remedial rise of tin prices.

From a technical point of view, the first support level is 121000 yuan of the 10-day moving average, and the second support level is 110000 yuan, which is unlikely to fall below the 110000 integer level. In terms of resistance level, the first resistance level is 131500 yuan for the 60-day moving average, and the second resistance level is 137000 yuan. It is expected that after the improvement of the epidemic in Europe and the United States, Shanghai and tin will quickly repair to 131500-137000 shock adjustment, if there is a major outbreak in Indonesia, Myanmar, Russia and Africa, the supply side will continue to tighten, prompting Shanghai and tin to rise above 137000 yuan resistance level.

On the whole, the demand-side and supply-side weak pattern affected by the epidemic is still the current main pattern, and the decline in demand caused by the epidemic is still the leading factor in the trend of Shanghai and tin. At a time when the epidemic in Europe and the United States is approaching the inflection point to boost market sentiment, the shutdown and production reduction on the supply side makes the supply closer, and both ends of supply and demand support the continuous restorative rise of Shanghai and tin. If there is a greater deterioration of the overseas epidemic, it will usher in a weak operating stage, the decline of the market is the opportunity to build positions, can continue to layout more than one. Tin prices will continue to rise above 135000 in the second quarter.

Scan QR code, apply to join SMM metal communication group, please indicate company + name + main business

For queries, please contact Lemon Zhao at lemonzhao@smm.cn

For more information on how to access our research reports, please email service.en@smm.cn