SHANGHAI, Feb 21 (SMM) –

Transportation activity in coastal provinces has started to return to near normal levels in recent days, but that inland remains more restricted. Overall economic activity remains muted due to the 14-day self-quarantine rules in most cities which are limiting the ability of factories and construction to restart. However, in most areas this activity is expected to resume over the next few weeks and overall confidence in future demand remains solid. The government especially continues to push supportive messages towards helping the economy maintain its targeted growth rate and offsetting the slowdown from the disruption so far with clear monetary policy support and encouragement for factories and construction activity to resume as quickly as possible.

We still believe that there is little significant aggregate demand loss, more just a delay in demand as activity takes time to recover, but this is causing inventory to rise for most metals especially at producers. However, inventory always rises post CNY ahead of demand going into its strong season. Nonetheless the key issue now is how quickly the producer held inventory can be moved to end users as they resume activity through March. Should the activity remain slow and inventory rise to levels which hurt cashflows and cause producers to cut output, then this could be harmful to prices. However, should the inventory move smoothly and enable producers to avoid cash flow and production issues, then the overall impact to prices should be limited and encourage more upside based on the underlying view that demand for the year will be strong across the board.

Please see below for more details on the impact to each metal, and we will also keep you posted on the latest updates via our website www.metal.com and our social media channels- Linkedin and Twitter. Also, please stay tuned for our webinars in March as we continue to connect you with the latest happening in the China ferrous and nonferrous metals market.

Steel

Most steelmakers and traders of hot-rolled coil in China have seen greater inventory pressure and tighter cash flows as the downstream demand has yet to recover significantly amid the coronavirus (COVID-19) outbreak.

The financial strain, however, has not posed a significant threat to hot-rolled coil production. SMM remains optimistic about the near-term demand recovery, which is expected to ease the cash burden and send the inventory levels back to normal.

Inventory of hot-rolled coil at traders currently stands 2-3 times of the normal levels, with stocks of some traders that stockpiled large amounts of cargoes before the Chinese New Year holiday having four times of the normal levels.

About 90% of HRC traders are grappling with cash flow issues due to the severe cargo backlog. 80% of traders said their current funds could only guarantee payment of long-term annual contracts, while purchases via temporary contracts and tenders have to be suspended. On the other hand, 20% of traders have difficulties in fulfilling annual purchase agreements.

SMM research found that HRC mills that signed long-term contracts with traders had cash flows able to maintain their operations, while steel plants without long-term agreement with consumers and sell based on spot prices already faced with funding constraints amid declining orders and sluggish downstream demand.

Well-funded steelmakers increased liquidity by putting some rolling lines into maintenance. Meanwhile, some private steel mills were compelled to clear inventories at lower prices in order to improve cash flow.

Copper

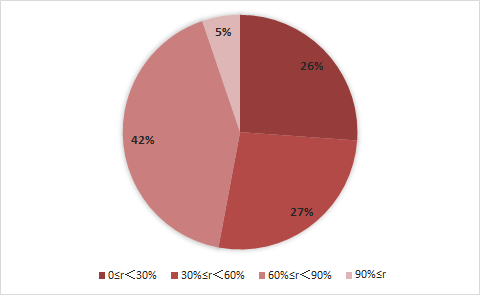

Most of copper downstream companies in China have resumed production, and overall production improved from last week after authorities loosened transport restrictions, according to the SMM survey conducted in the week ended February 20. Some plants in northern regions such as Shandong and Hebei remained shut on the back of tight transport restrictions, while other plants did not resume production. The SMM survey showed that about 42% of copper downstream companies have recovered to 60-90% of their normal production levels, while about 27% have recovered to 30-60%.

The survey also showed that production recovery is progressing well in south and east China, the major production and sales hubs of copper products. Most of the copper products producers resumed operations and recovery rate increasing.

In east China, most of the copper semis producers have resumed operations in anticipation of the return of workers after being quarantined for two weeks. Eased logistical constraints also encouraged plants to resume operations. Cargo shipment is allowed with pass access, and the removal of trans-provincial restrictions after February 17 also helped in the recovery of cargo shipments. While a shortage of truck drivers kept transportation slow, overall logistics recovered better than previously expected.

In the major copper consuming hub of south China, situations are similar to east China. Most of copper processors have resumed operations. Cargoes have to get an access pass from the firm before entering industrial parks. In terms of manpower, workers have returned to work, except for those from regions such as Hubei and Wenzhou where have been severely hit by COVID-19. Recovery rates across copper processors in south China now hold at 50-80%.

In central China, especially Henan, virus containment measures have been pretty stringent, with transportation and travel restrictions as well as quarantine rules preventing plants from reopening. Following the recovery of logistics, most of firms in central China have resumed production, but the recovery is slower than east and south China. While the delivery of orders from import clients has recovered, inventories of finished or semi-finished goods expanded. In-plant stocks are likely to recover to normal in the short term, as logistics gradually recovers.

In other regions such as north, northeast and southwest China, road transport within or across provinces still faces restrictions, while rail and maritime transport is better. Some companies saw higher inventories of finished goods or delayed deliveries of orders, but most of their employees have returned to work.

Copper Scrap: Trades of copper scrap in Foshan of southern Guangdong province, which is one of China’s main metal recycling centres, will resume gradually next week as the government urges producers to recover operations. However, copper scrap recycling and dismantling may return to normal only by next month given the existing transportation curbs and quarantine requirements for migrant workers.

The Foshan copper scrap distribution centre remained shut as of February 19, due to an absence of resumption of workers, and this resulted in limited availability of copper scrap and muted trades in the market. Operations of scrap-using copper rod producers were also impacted amid disruption of raw materials supply.

Downstream scrap-consuming producers restarted work as early as February 10, but they only used cargoes purchased before the Chinese New Year holiday rather than replenishing the stocks. Most producers faced dwindling raw materials stocks, suggesting great pent-up demand.

Major copper scrap trades in Foshan said they will resume operations by February 24, and some traders took an even pessimistic prospect, expecting the return of workers by end of the month. The Foshan government said on February 18 that businesses no longer need to seek prior approval before resuming operations and they need not require returning workers to show the proof of their health status.

Chart 1: Rates of production resumption at copper downstream producers

Aluminium

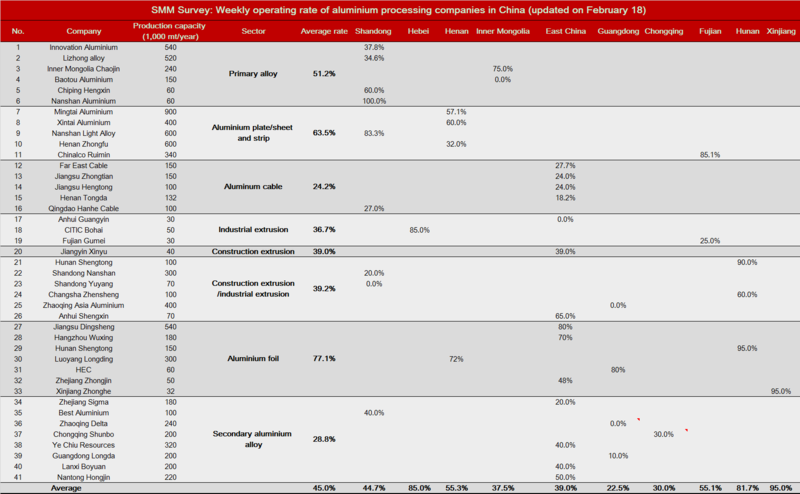

Primary aluminium alloy: Operating rates at primary aluminium alloy producers fell sharply when compared to levels before the Chinese New Year as inventories of finished products were piling up. Wheel makers gradually resumed production and purchases this week. This, together with increased trucking capacity, slightly eased inventory pressure at primary aluminium alloy producers, who are expected to focus on working through stockpiles and keep operating rates stable next week.

Aluminium plate/sheet and strip: Large aluminium plate/sheet and strip producers continued to produce during the Chinese New Year, but some of them were forced to cut output after the holiday as transport restrictions amid the COVID-19 outbreak made it difficult for them to secure raw materials and ship out finished products. Small and medium-scale producers resumed between February 10-17, but operated at reduced capacity. Henan, Shandong, Jiangsu and Zhejiang provinces saw higher operating rates than south-west China, Hubei and Hunan where some producers remained shut. The main hurdles to resumptions are delayed return of staff, logistics issues and mandatory guidance. Orders this month underperformed the same period last year, with domestic orders weaker than export orders. SMM has not heard of overseas clients rejecting shipments.

Aluminium wire and cable: Operating rates at aluminium wire and cable producers remained low, even after production gradually resumed from February 10. Cash crunch and production restrictions prompted some producers to only produce copper wire and cable at the expense of aluminium wire and cable and deliver urgent orders. Most of the producers faced little pressure of raw material inventories as they signed orders directly with aluminium smelters and have hedged positions in the futures market. They did not show much interest in restocking aluminium ingots and rods.

Secondary aluminium: Major secondary aluminium producers resumed operations progressively this week, but the epidemic impact kept the recovery schedule varied. Top producers in Jiangsu, Zhejiang, Shanghai and Shandong mostly resumed operations last week, and the operating rates increased significantly as of February 21. Producers in Chongqing, Guangdong, Jiangxi and Zhejiang, areas that were badly hit by the virus outbreak, may receive approval for resumption from this week, and are unlikely to operate as normal this week. Major secondary aluminium smelters mostly held offers at the levels before the Chinese New Year holiday, at 14,400-14,600 yuan/mt, and fulfilled pre-holiday orders. Delayed approval for resumption and greater cash flow burden drove medium-scale and small producers to cut offers by 300 yuan/mt, to 13,700-13,800 yuan/mt. On the raw material front, no quotes have been seen in the aluminium scrap market as scrap suppliers are mostly of small scale and have not returned from holidays. An increase in aluminium scrap supply in March is expected to weigh on prices of aluminium scrap and ADC12 aluminium.

Aluminium extrusion: Producers of aluminium extrusion resumed operations at an overall fast pace this week. Operating rates edged higher from a week ago in Shandong, Jiangsu and Anhui that felt a relatively smaller impact from the epidemic, and a great number of producers in Guangdong reopened this week. Top producers such as Jianmei, Fenglv and Huachang have restarted work, but companies in a few areas still faced delayed resumption due to a lack of workers, logistics restrictions and policy issues. This is especially the case in Hubei, where companies are not allowed to reopen before March 10. The resumption rate of the industrial extrusion sector is higher than that of the construction extrusion sector, but the overall operating rates may unlikely to see a significant rebound in the short term.

Aluminium foil: Operating rates in the aluminium foil industry picked up from the two weeks post-holiday, but the increase remained capped by the continued output cut at most producers as the motor traffic curbs disrupted raw materials supply and lifted inventories of finished products. Orders from overseas consumers outperformed that from the domestic market, after some producers resumed export business on February 18. But current high delivery costs and limited transportation capacity deterred the cargo shipment from producers to ports, making some companies to delay the delivery to foreign buyers till early April. Aluminium foil producers will continue to clear backlogged inventories of finished products next week. Gradual recovery of the raw material supply will support a rally in the operating rates.

Chart 2: Weekly operating rate of aluminium processing companies in China (updated on February 18)

Stainless steel

More stainless steel producers in China restarted operations as the government urged factories to resume following weeks of stoppages due to the coronavirus outbreak, a SMM survey showed as February 20.

In Jiangsu, producers can resume production only after receiving approvals from local authorities. The Oriental Steel City, a major market in Jiangsu, remained shut and the resumption date was undetermined. This kept most stainless steel processors from recovering operations, while companies outside of the Oriental Steel City restarted production successively. Producers in Foshan, Guangdong province are in smooth resumption, and a full recovery is expected by end-February.

Chart 3: Operation status update of stainless steel sector

Most stainless steel mills are operating normally, and a major producer in Jiangsu has returned from the CNY holiday. A blast furnace at a producer in central China has not resumed operations due to environmental inspections, and some small stainless steel plants failed to recover as scheduled on February 10. Large-scale stainless steel mills have sufficient inventories that could guarantee production, and their procurements could be delayed due to logistics issues.

As of early this week, some major stainless steel traders in Foshan said they planned to postpone their resumption till February 17 due to the epidemic impact, and some medium-scale and small traders will restart production on the basis of local requirements.

On the downstream front, a small number of consumers including machinery manufacturers and small home appliance producers have resumed operations, but the purchases of steel products remain affected by the existing transportation curbs and the suspension of traders. But enquiries online have increased.

In Foshan, some warehouses reopened on February 10. But goods were rejected in stainless steel storage warehouses amid muted trades and transportation restrictions, SMM learned. The Foshan government said on February 18 that businesses no longer need to seek prior approval before resuming operations and they need not require returning workers to show proof of their health, a move aiming to accelerate the resumption of the industry chain and reduce the impact of the virus outbreak.

Over 50% of industrial enterprises above designated size in Guangdong, Jiangsu, Shanghai have restarted operations, the State Department said in a press conference on February 19.

Zinc

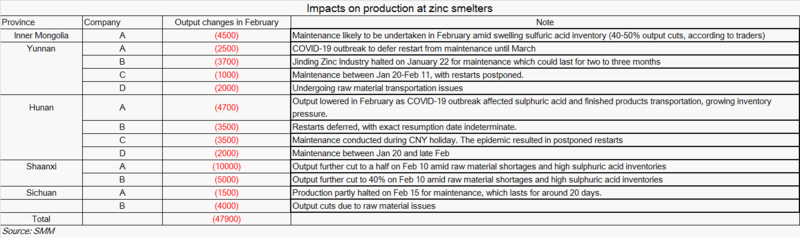

Smelter: Some of large-scale smelters were forced to cut output amid a backlog of finished product inventories, cash flow issues, higher sulfuric acid inventories and tight raw material supply, which is driven by logistics issues and deferred downstream restarts.

High profits prompted large smelters to maintain high production during CNY holiday, growing finished product inventories. Treatment charges (TCs) of zinc concentrate (50%) stood at a high of 6,000-6,500 yuan/mt with metal content, leaving profits at 1,000-1,500 yuan/mt. SMM expects refined zinc output in the survey sample to have stood at 388,399 mt as of February 20, a drop of 54,800 mt or 12.3% from January.

Chart 4: Impact on production at zinc smelters

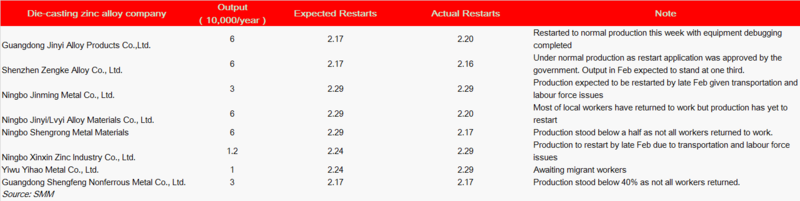

Die-casting zinc alloy plants: Several plants resumed production last week, while some restarted this week. Most of the plants kept production at 30-50% of normal levels. Production is unlikely to be fully restarted until cross-municipal and cross-provincial automobile transportation returns to normal and all migrant workers return to work.

At a press conference held by the State Council last week, off-peak commuting and travel are encouraged.

Many regions lifted approvals for production resumption applications depending on the degree of COVID-19 infection. Producers in Foshan, Ningbo, Jiangmen, Wuxi and Chengdu that meet requirements of virus prevention and control are allowed to restart after reporting to relevant authorities. Most of die-casting zinc alloy plants are distributed in east and south China.

Currently, most of die-casting zinc alloy plants are facing manpower and raw material purchases and sales issues as well as a lack of end-user orders. The quarantine and road block prevented some of the workers from returning to work, keeping operating rates low. Raw material purchases and sales are affected as logistics, especially cross-municipal and cross-provincial automobile transportation, has yet to fully recover. Some of producers saw sparse new orders from end-users, and are restocking finished product inventories.

Chart 5: Updated production restarts at some die-casting zinc alloy producers

Currently, most of die-casting zinc alloy plants are facing manpower and raw material purchases and sales issues as well as a lack of end-user orders. The quarantine and road block prevented some of the workers from returning to work, keeping operating rates low. Raw material purchases and sales are affected as logistics especially cross-municipal and cross-provincial automobile transportation has yet to fully recover. Some of producers saw sparse new orders from end-users, and are restocking finished product inventories.

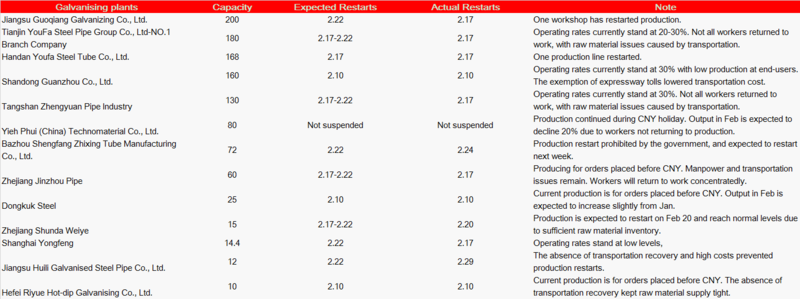

Galvanising: SMM understood that most of galvanising plants have completed production resumption. But issues remain that the failure of some of workers in returning to work resulted in low operating rates. Unrecovered cross-provincial transportation hampered restocking of raw materials, limiting production. Low production at end-users kept galvanising plants executing orders placed ahead of CNY.

China released more policies encouraging production restarts this past weekend. The rate of production restarts at over 20,000 major production-oriented plants, controlled by 96 state-run companies (excluding those in the commercial and trade, finance and real estate sectors), stood at 81.6%, according to a video conference on February 15 by the State-owned Assets Supervision and Administration Commission of the State Council (SASAC). Manpower, material and transportation issues limited restarts at building construction companies. Many governments also lifted production restarts approval procedures.

Chart 6: Galvanising plants operation update

Lead

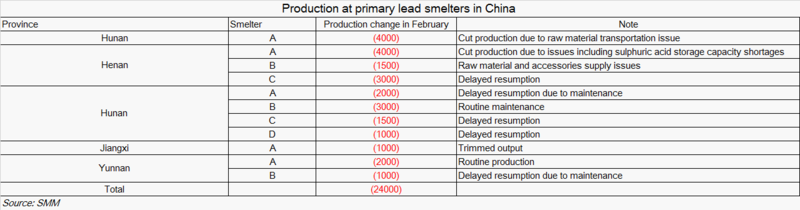

Primary lead: The coronavirus outbreak has had limited impact on production at primary lead smelters in China, according to the latest SMM survey.

Chart 7: Primary lead smelters operation update

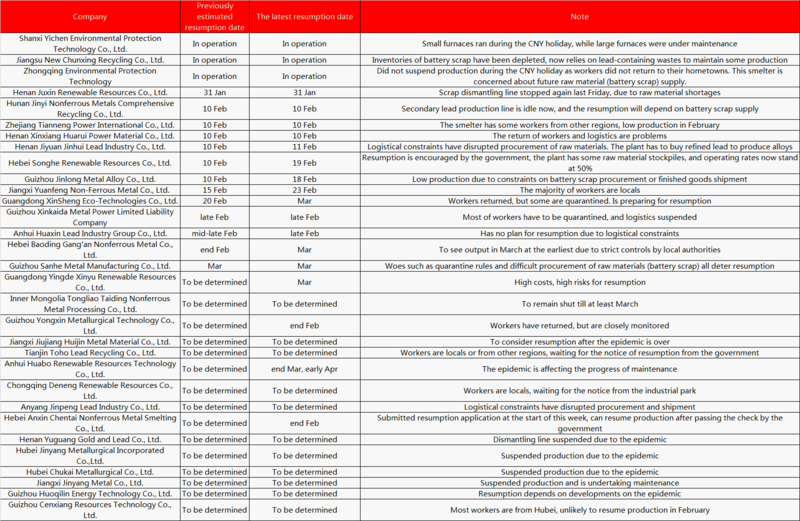

Secondary lead: Secondary lead smelters in Guizhou, Hebei, Guangdong and other regions are preparing for production recovery, as authorities push for business resumption following an easing in the epidemic situations. But manpower shortages as a result of quarantine rules and transportation restrictions (especial between provinces) that will constrain finished goods shipments and supply of raw materials―battery scrap and secondary lead bullion, deterred some smelters from resuming production.

Chart 8: Secondary lead smelters operation update

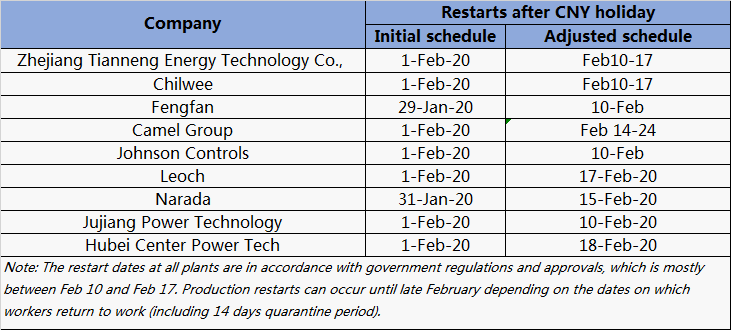

Lead-acid battery: About two-thirds of lead-acid battery producers in China have resumed operations as of the third week of February, but manpower shortages and logistical constraints limit operating rates, showed the latest SMM survey. The proportion of resumed battery producers is high in Jiangsu, Shandong, Jiangxi and Guangdong, lower in Anhui, Henan and Zhejiang, and the lowest is seen in Hubei, the epicentre of the coronavirus epidemic.

Leading companies took the lead and resumed operations in the week of February 10. Large and medium-sized firms followed suit in the week of February 17, while strict virus containment measures forced companies in some regions to remain shut and they had to delay the resumption to this week.

Operating rates at Chinese lead-acid battery producers now are 30-60%, and companies with the majority of workers being locals could operate at a rate of about 70%.

Lead-acid battery producers are unlikely to recover to stable production until early March, given the 14-day quarantine rules and battery shipping constraints.

Chart 9: Battery companies operation update

Cobalt/Lithium

Producers of cobalt and lithium products have recovered successively in Jiangxi, Jiangsu and Sichuan as of February 20. Smelters in Hubei, the epicentre of the coronavirus outbreak, remain suspended, while some plants in Hebei, Zhejiang, Guizhou and Yunnan plan to delay their resumption till next week.

Producers in Hubei have not received official approval for recovery as of noon on February 20. Companies in Jiangxi are allowed to restart production after reporting to authorities. A slew of producers of cobalt salts, lithium salts, ternary precursor and lithium manganese oxide (LMO) in Jiangxi resumed this week, while some lithium iron phosphate (LFP) plants will reopen in early March.

In Jiangsu, producers in Wuxi restarted production earlier this month. Some production lines at plants in Haimen maintained operations over the Chinese New Year holiday, and some lithium salts producers received the green light to restart work last Thursday and Friday.

Lithium salts plants in Sichuan resumed operations this week, while several producers of ternary precursor and ternary materials have not been allowed to resume and may postpone the recovery till next week.

Major producers in Hebei did not halt operations during the CNY holiday, but cut the operating rates to 30%. A handful of local producers plan to reopen next week. Zhejiang also saw more plants recovering production this week, but the continued strict regulations amid a virus outbreak will keep the operating rates at low levels in February.

In Guizhou, major producers of ternary precursor continued to produce during the holidays, while some LMO plants resumed operations on February 20, with more producers to return next week.

Some battery producers in Guangdong resumed operations this week. Recovery of some plants in Yunnan, however, has been delayed. Battery mills in Henan have not received official approval as the area was badly hit by the virus.

On the raw material front, some cobalt salts plants continued to face import restrictions. But top producers of cobalt salts and batteries reported sufficient supply of raw materials that could guarantee production by end-February, primarily due to lower operating rates on the virus impact and stockpiles stored up pre-holiday.

Most downstream producers also have raw materials that could meet demand till the end of this month, as they scaled back operations in February. Only several top producers of ternary precursor and ternary materials showed greater demand after they maintained production over the holidays. Bullish prospects for prices drove some large-scale producers of lithium cobalt oxide (LCO) to lock in orders of cobalt salts and cobalt (II, III) oxide.

Import of intermediate product for hydrometallurgy may recover next week, SMM learned from market participants. But it requires time for smelters to normalise operations, which may see the operating rates this month only at 30-40%.

Some logistics hurdles have been removed this week. The recovery of operating rates across the chain, however, remains at a slow pace due to the quarantine requirements for returning workers.

Tin

Transportation restrictions that could constrain raw material procurement and finished goods shipments remained the biggest drag on the recovery of the tin industry chain, the latest SMM survey showed.

Tin ore: While cargoes could make declaration at customs, tin ore imports from Myanmar remained disrupted as shipment to the domestic market has yet to recover. That, coupled with quarantine rules on workers back to Myanmar, is expected to prevent tin ore imports from recovering for some time.

Smelters: In Yunnan, some of the smelters maintained production, while the others are likely to remain shut till end of February or early March. While some smelters have yet to resume production, their sales have resumed, and quotes were slightly higher than market prices. Some smelters required their clients to take the delivery of cargoes on their own given logistical constraints.

In Jiangxi, only a few smelters maintained production during the Chinese New Year holiday. Some resumed production this week, and their quotes and shipments also recovered. But there were some smelters will remain shut until next week. Small brand supply on the market is likely to gradually recover.

Downstream: Tin consumers in Guangdong have gradually resumed operations, but operating rates failed to climb to high levels due to manpower shortages and the absence of approvals from authorities. The operating rates are set to increase with more workers returning to work, but the recovery will continue to be subdued by trans-provincial logistical restrictions that will affect raw material procurement and orders.

Warehousing: Warehouses that house tin all have resumed normal operations.

Logistics: Cargo transportation still faces restrictions between provinces, and manpower shortages have lifted transportation costs.

Further Reading

High-grade silicon prices jumped from pre-holiday levels (Feb 19, 2020)

Foshan rolled out stimulus for car market amid coronavirus outbreak (Feb 19, 2020)

SMM Hot News-China Metal Special Report 5: Impact of COVID-19 on China metals market (Feb 18, 2020)

![Vale Plans to Increase Mineral Reserve and Resource Volumes; Overnight, Both LME Copper and SHFE Copper Closed Higher [SMM Copper Morning Meeting Summary]](https://imgqn.smm.cn/usercenter/XBbTq20251217171709.jpg)