SMM12, March 19: 2019, the nickel price wide shock, the overall center of gravity up, and although the market attention to the main contradiction is still the "old" laterite nickel ore-nickel pig iron-stainless steel logic, but because the market expectations for the future are affected by different events in different periods, the views of all parties are also different.

Looking forward to the global nickel market in 2020, SMM believes that in 2020, China's nickel pig and iron plant will be forced to reduce production in the absence of nickel mine preparation. At the same time, the speed of implementation of new production capacity in Indonesia is also uncertain, and the pattern of concentrated existing production capacity will not change in the near future. In addition, there is a period of tight raw material supply, wet projects and waste in the new energy industry chain, and nickel sulfate manufacturers need to use more pure nickel. It is not difficult to judge that even if the output of Indonesian nickel pig iron catches up and finally meets the demand, the contradictions caused by many uncertainties in the industrial chain still have the possibility of fermentation. These possibilities are not only beneficial to the good nickel price. There are also significant potential negative aspects, such as the slowdown in global stainless steel production, and so on. Overall, nickel prices are bound to continue to be choppy in 2019.

Some of the charts and data in this paper are intercepted from the SMM China Nickel Industry chain report 2019-2022. If you need consultation and subscription, you can dock the SMM Nickel Research Group according to the contact information at the end of the article.

1. China's nickel pig iron market: a shortage of nickel mines is imminent. A partial reshuffle of nickel pig iron plants is inevitable.

Photo: 2013-2022E imports of nickel laterite from China

Source: SMM

The main suppliers of nickel mines in China are the Philippines and Indonesia. In addition, New Caledonia and Guatemala also have a small supply each year, with Indonesia and the Philippines accounting for more than 95 percent. Before 2014, Indonesia was the largest supplier of nickel laterite mines in China, accounting for more than half of the total imports. Since the ban in 2014, the supply pattern of laterite nickel mines in China has changed. The Philippines has become a major importer. Indonesia's imports in 2015 and 2016 were basically zero. Indonesia liberalized some nickel mine exports in 2017, requiring Indonesia to make progress in the construction of domestic nickel smelters and use certain tastes of low taste nickel mines to qualify for nickel ore export quotas, corresponding nickel ore taste should be less than 1.7%. After 2017, China's imports of Indonesian nickel mines gradually resumed, and in 2018, Indonesia zhan, China imported 1/3 of the supply of laterite nickel mines. When Indonesia opened up some laterite nickel mines in 2017, it said it would relax exports for only five years and would reclose the export window for laterite nickel mines in 2022.

At the end of August 2019, the Indonesian government made a sudden statement to ban mines ahead of time, bringing forward the ban on nickel mines originally scheduled for 2022 to January 2020. As soon as the incident occurred, Indonesia's nickel mine imports rose 94.2% month-on-month in September 2019. With the start of the mining ban in Indonesia in 2020, the supply pattern of nickel mines in China has developed into a dominant state in the Philippines, and the supply of nickel laterite imported from China is expected to increase to around 93 per cent by 2022.

SMM estimates that Philippine nickel laterite exports could be around 45 million wet tons in 2020, up 9.3 percent from 41.18 million wet tons in 19 years. The equivalent metal content is about 345400 metal tons, of which high nickel mines account for about 60 percent, and the equivalent metal content is about 249100 metal tons. As a result of the depletion of high-grade resources in the Philippines, the taste of imported nickel mines will decline significantly next year, with an average grade within the range of 1.4%-1.45%. With the exception of the Philippines, countries such as Guatemala and New Caledonia expect to import 3.5 million wet tons of high-grade nickel ores with a grade of about 2 per cent in 2020, equivalent to 43600 metal tons.

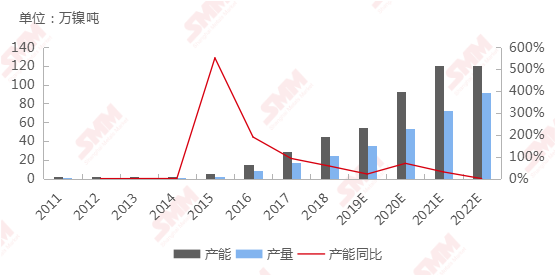

Figure: 2011-2022E trend chart of production capacity of nickel pig iron in China

Source: SMM

SMM predicts that after Indonesia bans nickel exports in 2020, domestic nickel pig iron production will begin to shrink after peaking in the first half of 2020 and accelerate in 2022, when it will reach 100000 tons. Nickel ore resources are scarce and prices are difficult to fall, coupled with the impact of Indonesian products on the domestic nickel pig iron industry, it is expected that the difficulty of operation will increase sharply, and the accelerated elimination of high-cost enterprises and processes and the shrinkage of production capacity are inevitable. In December 2019, in the high nickel pig iron market, we can already see a certain scale of low-price Indonesian supply impact on the market, accelerating the decline of high endogenous pig iron prices.

2. Indonesian Nickel Market: profit transfer Game between Nickel Mine and Nickel Pig Iron smelter

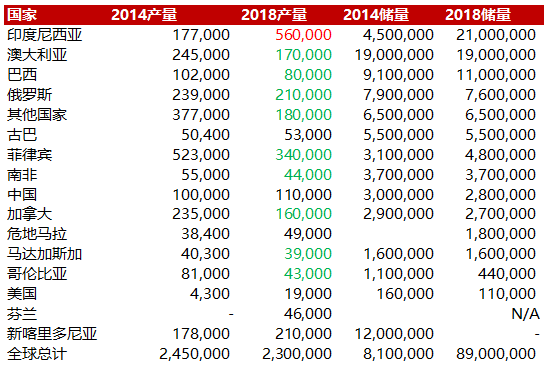

Figure: 2014 VS 2018 Nickel reserves and production in countries around the world by 2018 reserves

Source: USGS

The industrial pattern of a metal is fundamentally closely related to the distribution characteristics of mines. China accounts for half of the world's primary nickel consumption, but it is a nickel-poor country. The main nickel producing countries are highly concentrated in the top few countries, while the laterite nickel ore, which has the most cost advantage, is distributed in the equatorial belt, Indonesia has gained the leading advantage, and there are contradictions in the industrial chain from the very beginning. After the laterite nickel mine has been fully developed and utilized, the biggest problem is not the balance of global supply and demand, but the distribution of profits in various countries and industrial chains.

Indonesia, as the largest stockholder and producer of laterite nickel mine, made the decision to ban nickel mine export in advance in 2020. It can be predicted that its policy will continue to have a significant impact on the market in the following time. Just take the last two news as an example:

Policy 1: increase in franchise tax rates

On December 10th Indonesia raised the right to use tax on nickel ore sales from 5 per cent to 10 per cent, according to the SMM. It was learned that the news was basically true. If Indonesian nickel mines are sold in circulation on the market, the cost will include not only mining costs, but also taxes and transportation costs. The tax and fee involved in this adjustment is one of the more important taxes and fees levied by the government on the mine, which is the "mine concession fee" (royalty). Operators speculate that the tax rate will be adjusted for the purpose of driving up the domestic trade price of Indonesia's nickel mines.

Policy 2: proposed minimum pricing of nickel mines?

On November 15, the Indonesian government announced that for the first time, the Indonesian laterite nickel mine with a grade of 1.7% was priced at US $30, according to industry insiders, which is the price of domestic trade in Indonesia. According to SMM, because the local nickel mine resources are rich and the smelter capacity is concentrated, and has a say in nickel mine pricing, the mine price has been at a low level before, 1.7% laterite nickel mine is generally 17-18 US dollars / wet ton, 1.8% laterite nickel mine is 27-28 US dollars per wet ton, and the mine profit level is meagre. Once the official pricing is implemented, it will significantly increase the cost of Indonesia's nickel pig iron smelter, so the industry expects that the implementation of the rule will continue to be controversial for some time.

Source: SMM

From 2020 to 2022, the growth rate of nickel pig iron production in Indonesia will be 49%, 35% and 28% respectively. The growth rate will slow down gradually because with the sufficient supply of NPI, it will slow down spontaneously after fully tapping the downstream demand. Normally, the growth rate will gradually tend to the production growth rate of 300 series stainless steel plants.

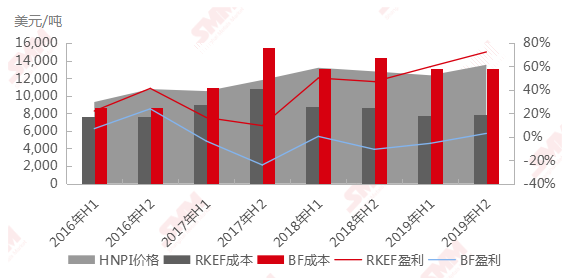

Figure: changes in the cost of nickel pig iron in Indonesia from 2016 to 2019

Source: SMM

In 2019, the average price of high-nickel pig iron remained high compared with 2018. Indonesia's RKEF was profitable, while the BF operating rate remained low. The average profit of RKEF is around 60-70 per cent, while the theoretical profit of BF is negative, so the actual operating rate is very low, contributing less than 10, 000 nickel tons to production for the whole year.

Indonesian RKEF high-nickel pig iron has been operating under high profits in the past two years, which is not only related to its inherent advantages in raw materials and energy, but also to the long-term surplus and oversupply of Indonesia's domestic nickel mining market. If high profits are to be sustained, they will always face external challenges. In addition to controlling production, smelters will also have to play games with ore suppliers who have been seeking high profits. At present, most operators believe that in the case of an obvious oversupply over demand, it is difficult to achieve an increase in the price of Indonesian domestic trade ores, and if the policy means intervene, there will be room for this part of the profits to be narrowed.

Overall, Indonesia's RKEF production capacity is the final bottom line of the global nickel market, well below $10000 / ton, this share of the increase, in the long run, the lower limit of nickel prices under deep pressure, for 2021-2022, whether new energy expectations can actively boost nickel sulfide and pure nickel consumption will be crucial, once this part of demand is lower than expected, nickel lost the premium given by new energy, its price U-turn will be very fierce.

3. Stainless steel market: there is still a certain growth rate in China and Indonesia, which is still highly competitive in 2020.

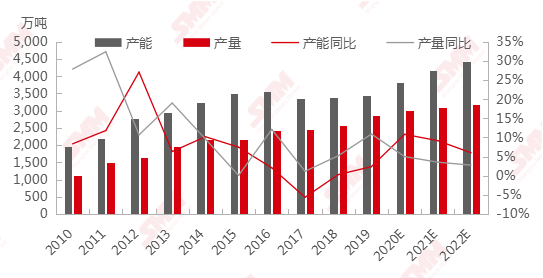

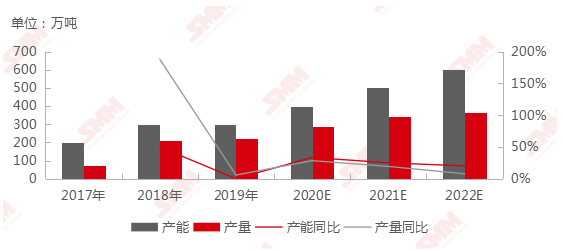

Figure: 2010-2022E capacity and output of stainless steel in China

Source: SMM

For China's stainless steel industry, 2020 will be a year of fierce competition, raw materials red delivery is still the main competitiveness of the development of steel mills, China's stainless steel production growth is expected to slow, but the total increase in 2020 is expected to be 5.3%.

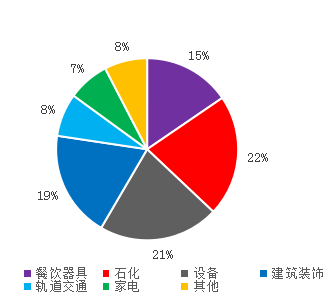

Figure: proportion of downstream consumption of stainless steel in 2019

Source: SMM

Figure: production capacity of stainless Steel in Indonesia from 2017 to 2022

Source: SMM

Indonesia has benefited from its rich laterite nickel resources and its remarkable cost advantages. It has continuously attracted foreign investment to build nickel smelters and stainless steel plants there. As China levies anti-dumping duties on stainless steel imported from Indonesia and other places, the utilization rate of stainless steel capacity in Indonesia will be limited in the future. In the future, Indonesia will take nickel pig iron as the main export product.

SMM expects Indonesian stainless steel capacity growth to remain around 33 per cent from 2019 to 2020, mainly due to the commissioning of stainless steel in Delong, Indonesia.

4. Global refined nickel market: the resumption of production enterprises is highly sensitive to nickel prices and is expected to increase production is relatively limited.

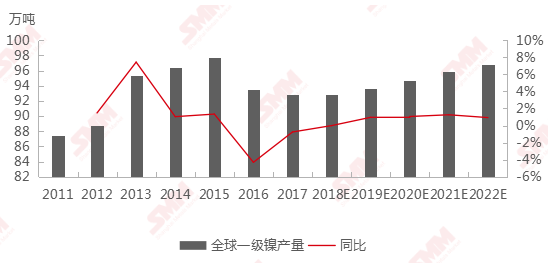

Figure: 2011-2022 E global first-class nickel production

Source: SMM

Between 2019 and 2022, SMM expects global first-level nickel production to increase slightly, with some shutdown capacity willing to resume production, but remains concerned about the interference of nickel price changes on production.

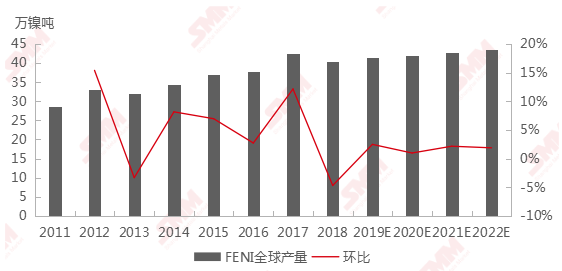

Figure: 2011-2022 E Global Water extraction Nickel production

Global Feni production fell slightly in 2019, mainly due to the Dagong Mountain project in Myanmar, which was overhauled in the first quarter, and the Koniambo spill in New Caledonia. Production of these two projects will resume in 2020, in addition to the planned resumption of the Vale Onca Puma nickel mine project, it is expected that the corresponding Feni project capacity utilization will be improved and global Feni production will increase.

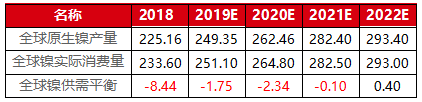

5. Balance sheet and point of view

For 2020, SMM's main views on the global native nickel balance sheet are as follows:

The global primary nickel gap in 2020 is 23400 tons, slightly larger than that of 17500 tons in 2019. Global nickel consumption is expected to grow by 5.46% in 2020, while supply growth is slower than consumption growth by 5.26%.

Table: 2018-2022E Global balance of Nickel supply and demand

Unit: 10,000 tons of nickel

Source: SMM

"2019-2022 China Nickel Industry chain report" is about to be released, more detailed data and analysis of the nickel industry, welcome to contact the SMM Nickel Research Group for consultation and subscription.

Contact: Liu Yuqiao 021-51666804, QQ 2881050930

Wu Tingting 13795448891

Catalogue of China Nickel Industry chain report 2019-2022:

Annual report Summary: 2011-2022 E Global balance of Nickel supply and demand 4

1. Aspects of Nickel consumption

1.1 Analysis of stainless Steel Industry in China and India

1.1.1 Chinese Market Analysis of stainless Steel

1.2.2 Indonesian Market Analysis of stainless Steel 1

1.2 Battery Industry

1.2.1 New Energy Battery Industry

1.2.2 Analysis of Nickel consumption of traditional E Battery from 2014 to 2022

2. Overview of nickel supply

2.1 Market Analysis of Primary Nickel

2.1.1 balance sheet and Price Forecast of Global first-level Nickel supply and demand for 2011-2022

2.1.2 Analysis of Global first Class Nickel production from 2011 to 2022

2.1.3 Analysis of first Class Nickel production in China from 2013 to 2022

2.1.4 quantitative Analysis of China's Import of Primary Nickel from 2009 to 2019

2.1.5 Analysis of global first-level nickel stocks from 2014 to 2019

2.2 Analysis of Secondary Nickel Market

2.2.1 balance between supply and demand and Price Forecast of E Nickel Pig Iron from 2012 to 2022

2.2.2 Global Nickel Iron production capacity 2011-2022

2.2.3 Global profit Analysis of Nickel Pig Iron from 2016 to 2019

2.2.4 Analysis of Global Nickel Pig Iron stocks from 2014 to 2019

2.2.5 Analysis of production capacity of E Global Water extraction Nickel (feni) from 2011 to 2022

2.3 Nickel Sulfate

2.3.1 Analysis of Nickel Sulfate Industry in China and the World

2.3.2 Global Nickel Sulfate production from 2016 to 2022

2.3.3 balance Table and Price Forecast of Nickel Sulfate supply and demand in China from 2014 to 2022

2.3.4 comparison of production cost of Nickel Sulfate with different mainstream Raw Materials

2.3.5 Global Nickel Intermediate production capacity 2017-2022

2.3.6 comparison of Global Intermediate Investment costs

2.4 Nickel ore

2.4.1 supply and demand balance and Price Forecast of Chinese laterite Nickel Mine from 2013 to 2021

2.4.2 quantitative analysis of nickel laterite imported from China from 2013 to 2021

2.4.3 inventory Analysis of laterite Nickel Mine in Chinese Port from 2014 to 2019

Scan 2D code, apply to join SMM metal communication group, please indicate company + name + main business