SHANGHAI, Dec 13 (SMM) –Hoshine Silicon, a Zhejiang-headquartered major silicon producer in China, will build 800,000 mt/year of silicon metal capacity in Zhaotong, Yunnan province.

Although electrical power costs in Zhaotong are higher compared with other cities in Yunnan, sustainable availability of high-grade silicon ore has made Zhaotong ideal for investment, amid supply tightness of high-quality ore in China.

Yunnan currently has an annualised designed capacity of 1.3 million mt, located mostly in the western part of the province, including Dehong, Baoshan, Nujiang, and Lincang that boast rich hydro-power resources.

The capacity utilisation rate, however, stands at low levels in Yunnan due to maintenance and dry season issues. The monthly average operating rate at silicon producers in the province stood at 46% in 2018.

China’s silicon industry features low concentration ratios, as small and medium-scale producers with a capacity below 40,000 mt/year accounted for 89% in terms of number and 53% in terms of production capacity of the total silicon producers in China.

Silicon plants in Yunnan are mostly of medium-scale with an annualised capacity of 20,000 mt, invested by companies in Fujian and Zhejiang provinces before 2010. The past decade saw limited silicon capacity addition and expansion projects in Yunnan.

The opportunity of expansion/merger of Yunnan's existing small and medium-scale silicon companies came even smaller as the local implementation of desulfurisation methods over the past two years, ahead of other major silicon production areas in China, increased the cost of investment by around 10%.

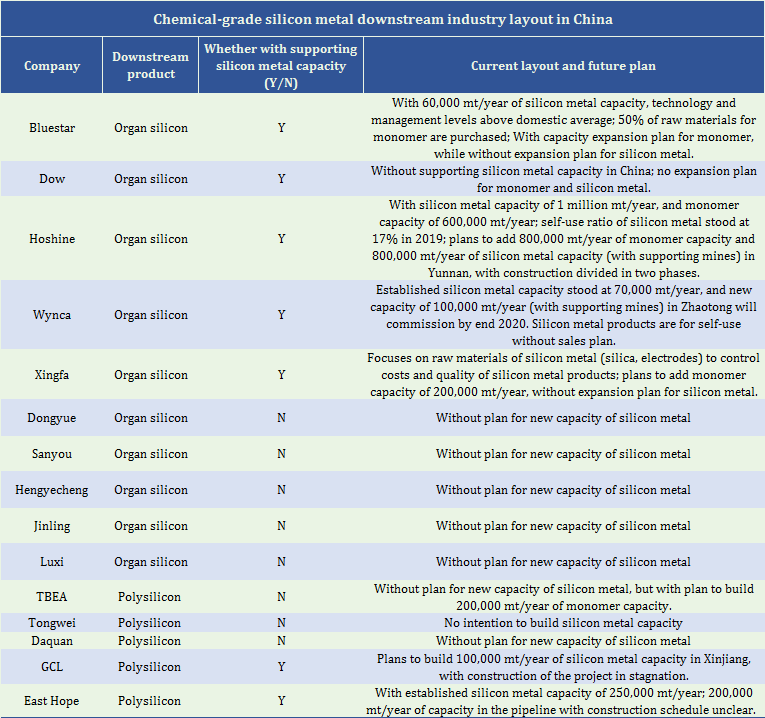

Silicon metal can be categorised into metallurgical-grade and chemical-grade products based on downstream applications. Metallurgical-grade silicon, used to produce aluminum alloy, also sees limited chances of new investment due to demand bottleneck in the downstream car market, which is the main consumer of silicon-aluminium alloy. Besides, silicon accounts for only 3-7% of the feedstock to make silicon-aluminium alloy.

There will be more opportunities to invest in chemical-grade silicon on the back of the domestic shortage of high-quality ore and the trend in demand growth. Chemical-grade silicon is used mostly in organ silicon monomer and polysilicon, which have higher requirements for the stability and composition element of raw materials.

For instance, chemical-grade silicon metal has to reach certain standards of content regarding not only main impurities such as iron, aluminium, and calcium, but also trace elements like phosphorus, boron, titanium, and carbon.

On the policy front, major production areas such as Yunnan and Xinjiang have imposed controls on the total silicon capacity, but a national-level production quota scheme has not been introduced. Yunnan aims to control silicon metal capacity within the province below 1.3 million mt/year by 2020, while boosting production and capacity of the top five producers to above half of the market share.

New silicon projects in Yunnan should be equipped with downstream facilities to obtain government approval.

Xinjiang enjoys the advantages of lower electricity prices and thermal power plants that could guarantee production all year round without the impact of seasonality. In terms of production capacity, Xinjiang has surpassed Yunnan to become the top silicon metal producer in China in 2015.

Addition of silicon capacity and construction of new self-owned power plants in Xinjiang face greater restrictions since 2018 as Xinjiang shifted its focus to high-level development.

As a total 2 million mt silicon metal capacity quotas were all issued in Xinjiang, large companies are mulling acquisition or replacement of unrealised quotas for their further expansion.

Besides capacity quotas, limitations on carbon emissions in each province will also be closely monitored.

Some silicon producers in Xinjiang were forced to cut or halt production due to depletion of carbon emissions quotas, a SMM survey showed. Some silicon mills in Fujian even purchased emissions quotas to extend production.

A severe mismatch between the production capacity and carbon emission quotas has been seen across silicon production areas in China.