Non-ferrous

Non-ferrous

Base Metals

Rare Earth

Scrap Metals

Minor Metals

Precious Metals

New Energy

Price CenterDatabaseProReportsEventsCar Insight

Language:

Language:

SMM, October 18, this morning, the non-ferrous metals market rose and fell each other, as of noon, Shanghai nickel fell 0.72%, Shanghai lead dived before noon down 0.15%, Shanghai tin, Shanghai aluminum, Shanghai copper rose slightly.

This morning, the National Bureau of Statistics released data for the third quarter of China's GDP growth of 6% year on year. According to preliminary accounting, the gross domestic product (GDP) in the first three quarters was 69.7798 trillion yuan, an increase of 6.2 percent over the same period last year. On a quarterly basis, it grew by 6.4% in the first quarter, 6.2% in the second quarter and 6.0% in the third quarter. In terms of sub-industries, the added value of the primary industry was 4.3005 trillion yuan, up 2.9 percent; the added value of the secondary industry was 27.7869 trillion yuan, up 5.6 percent; and the added value of the tertiary industry was 37.6925 trillion yuan, up 7.0 percent. National Bureau of Statistics: China's GDP grew 6% in the third quarter compared with the same period last year

In addition, industrial production above scale rose 5.8 per cent in real terms in September 2019 from a year earlier (the following growth rates were real growth rates excluding prices), 1.4 percentage points higher than in August. From a month-on-month point of view, in September, the value added of industries above scale increased by 0.72% over the previous month. From January to September, the value added of industries above scale increased by 5.6% compared with the same period last year. Of this total, the ferrous metal smelting and Calendering industry grew by 9.5%, the non-ferrous metal smelting and Calendering industry grew by 7.7%, the automobile industry grew by 0.5%, the railway, shipbuilding, aerospace and other transport equipment manufacturing industry grew by 4.7%, the electrical machinery and equipment manufacturing industry increased by 12.1%, and the computer, communications and other electronic equipment manufacturing industry increased by 11.4%.

Internationally, EU leaders agreed on Thursday (October 17) to a new Brexit agreement with Britain, which helped the pound hit a five-month high of 1.2990, but Prime Minister Johnson needs to enlist parliamentary support for Brexit if he wants to lead Brexit on October 31. Johnson said he believed Congress would support his deal.

On the nickel side, Shanghai nickel has fallen continuously in recent days, but it has been below hovering since the start of trading this morning, and there is no continuing downward trend for the time being. Huatai Futures said that in the market, most of the short-term benefits of Indonesia's mining ban have been digested by prices, and if supplies from other major nickel producers (the Philippines and Singapore) do not change much in the fourth quarter, there may not be enough incentive to continue to rise in nickel prices for the time being. At present, the nickel negative is still limited, nickel price may have some support, lack of power. The factors that break the shock pattern are the supply changes in other major nickel producing countries (upward) or the significant reduction in production of 300 series stainless steel (downward). Recently, the progress of Indonesian nickel and iron production has accelerated, the production of traditional nickel enterprises has increased month-on-month, the output of 300 series stainless steel has declined slightly, the main LME nickel bulls have closed their positions through delivery, and the short-term nickel price may have the risk of adjustment.

On the copper side, Barrick Gold (Barrick Gold) said a few days ago that although its gold production in the third quarter was lower than in the second quarter due to restrictions on the operation of the North Mara gold project in Tanzania, its full-year production continued to move towards the target limit of 510-5.6 million ounces. In terms of copper production, copper production in the third quarter was higher than in the second quarter as a result of the increase in production at the Lumwana copper mine in Zambia.

On the aluminum front, the National Bureau of Statistics announced on October 18 that the output of primary aluminum (electrolytic aluminum) in September was 2.9 million tons, down 1.6% from the same period last year, and the total output from January to September was 26.37 million tons, an increase of 1.1% from the same period last year. In addition, according to Indian media reports on Wednesday, due to a shortage of coal, India's national aluminum (NALCO) production has been seriously affected. "Coal shortage forces India's national aluminium (NALCO) to shut down electrolytic cells

On the black side, the black system generally fell before noon, but the overall decline was smaller than yesterday. In the morning, the National Bureau of Statistics announced that China's steel output in September was 104.37 million tons, up 6.9 percent from the same period last year, and the cumulative output from January to September was 909.31 million tons, up 10.6 percent from the same period last year. In real estate, national investment in real estate development in January-September 2019 was 9.8008 trillion yuan, up 10.5 percent from a year earlier, the same growth rate as in January-August. Of this total, residential investment was 7.2146 trillion yuan, an increase of 14.9 percent, and the growth rate was the same. Commercial housing sales, January-September, commercial housing sales area of 1.19179 billion square meters, down 0.1% from the same period last year, a decline of 0.5 percentage points from January to August.

Crude oil fell 1.44% in the previous period. The decline was limited by a new deal between the UK and the EU to leave the EU as data showed that US commercial crude oil inventories rose faster than expected last week. Analysts said that if the new Brexit agreement was approved by the British Parliament, it could avoid leaving the European Union without an agreement, which is expected to boost economic growth and oil demand. Focus on Saturday's parliamentary vote.

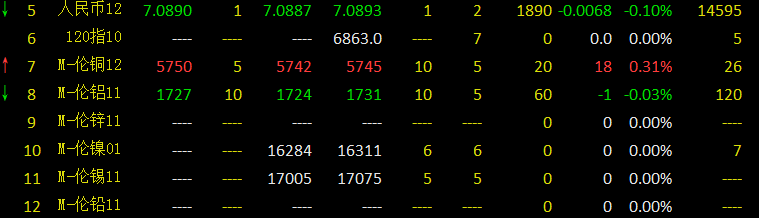

As of 11:45, the new LME Metal Mini Futures quotation launched by the Hong Kong Stock Exchange shows:

Today's stock

Lead: Guangdong market South China lead 17075 yuan / ton, the average price of SMM1# lead up 50 yuan / ton quotation; southern storage south 17035 yuan / ton, 1911 contract discount 20 yuan / ton; lead price high dive downward, recycled primary price difference further opened to 500-600 yuan / ton, downstream priority to buy recycled refined lead. Henan Yuguang, Wanyang and other smelters mainly to long single transaction; Jinli 16925 yuan / ton, the average price of SMM1# lead discount 100 yuan / ton quotation. Lead price diving downward, downstream fear of heating up, the market transaction continues a light trend. Other areas such as: Hunan Shuikoushan 16925-16975 yuan / ton, the average price of SMM1# lead discount to 50 yuan / ton quotation (traders); Hunan Jingui 16875 yuan / ton, the average price of SMM1# lead discount 150 yuan / ton; Jiangxi copper industry 17055 yuan / ton, the average price of SMM1# lead rose 30 yuan / ton; the revitalization of Yunnan 16725 yuan / ton, the average price of SMM1# lead discount of 300 yuan / ton. Lead price fast dive, downstream consumption is light, the overall transaction is in the doldrums.

Zinc: the mainstream transaction of zinc in Shanghai was 18880-18900 yuan / ton, and that of Shuangyan and Huize was 18890-18910 yuan / ton. The average transaction of zinc was 110-120 yuan / ton in November. Shuangyan and Huize reported 120-130 yuan / ton in November. The mainstream transaction of zinc was 18810-18830 yuan / ton. The trend of Shanghai zinc was relatively stable in 1911, closing at 18760 yuan / ton in the first trading session of the morning market. The first trading session, the morning holder quite high water quotation, with the market offer on the 1911 contract rose 130 yuan / ton, but the market transaction is light, the holder lowered the rising water quotation to 120 yuan / ton, but the transaction is still light, the market mainstream to the SMM net average price discount 5 yuan / ton transaction; in the second trading session, the zinc price continues the concussion market, the holder maintains the rising water quotation to the 1911 contract liter water 110-120 yuan / ton, each brand still maintains the priceless difference; the second trading session, the zinc price continues to fluctuate the market, the holder maintains the rising water quotation in the 1911 contract liter water 110-120 yuan / ton, each brand still maintains the priceless difference; Trading in the trade market is active, downstream enterprises meet bargains to replenish the warehouse, but still maintain in the rigid demand inventory, the market as a whole, the transaction is still good.

Guangdong zinc mainstream transaction in 18760-18800 yuan / ton, the quotation focused on Shanghai zinc 1911 contract discount 5-10 yuan / ton, Guangdong market than Shanghai stock market discount expanded from 100 yuan / ton to 110 yuan / ton. Refinery normal shipment, the market supply circulation is more abundant. In the morning, the quotation of the holder is about 20 yuan / ton for the 11 contract, but the receiver is not strong, and the transaction is concentrated around 10 yuan / ton for the 11 contract. Entering the second trading period, the market transaction is concentrated near the flat water of the 11 contract, and some of the holders are selling a small discount of 5 yuan / ton to the 11 contract. The market transaction is slightly boosted, and most of them are mainly received by traders. Downstream rigid demand procurement, the overall transaction atmosphere is slightly cooler than yesterday. Yi Qilin, Cishan, Tiefeng, Mengzi mainstream transactions in 18760-18800 yuan / ton near.

The mainstream transaction of zinc ingots in Tianjin market was 18820-20250 yuan / ton, the mainstream transaction of ordinary brands was 1877018930 / ton, the 1911 contract rose 70-200 yuan / ton, and the rising water of Tianjin market was stable at 30 yuan / ton compared with Shanghai stock market. Refinery shipments are normal today. In the market, the supply tension has eased slightly, but the overall situation is still tight. The quotation of high-priced brand source is concentrated in about 160-200 yuan / ton of 11 liter water, and the quotation of ordinary brand source is about 70-140 yuan / ton of 11 liter water. Disk finishing operation, rising water is still deadlocked, the market buying interest is lower, the shippers are more willing to ship, but the downstream receiving interest is not high, the holders slightly down the rising water, the downstream buying is slightly better. Overall, today's deal continues yesterday's light trend. Zi Zijin, Hongye, Bailing, Chi Hong, Xikuang, etc., were traded near 18820-18980 yuan / ton, and Qiao Zijin, Chi Hong and Hongye were traded at 18770-18930 yuan / ton.

< updating >

"Click to sign up for a thousand people event in China's non-ferrous metals industry.

Share the China Nonferrous Metals Industry Annual meeting registration link to the circle of friends or WeChat group of more than 100 people, and send screenshots to the WeChat account below to get the right to view "SMM Metal Breakfast" for one year (the original price is 300 yuan / year).

Scan QR code plus WeChat

For queries, please contact Lemon Zhao at lemonzhao@smm.cn

For more information on how to access our research reports, please email service.en@smm.cn