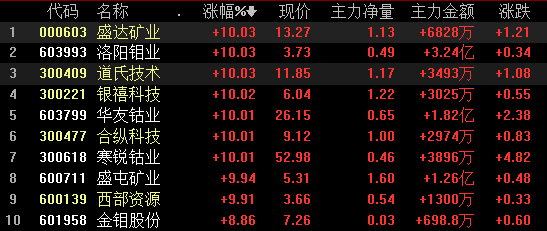

August 7 SMM8 news: August 7, the concept of cobalt rose in the front, as of press, cold cobalt industry, Huayu cobalt industry closed, Luoyang Mo industry, Pengxin resources, Shengtun mining and other collective rose.

It is reported that Glencore (Glencore Plc) plans to suspend production of Mutanda, one of the world's largest cobalt mines, after plummeting battery metal cobalt prices and rising project costs.

The Mutanda project may stop production by the end of the year and receive so-called care and maintenance. Last year, the Mutanda project produced 27300 tons of cobalt, more than half of Glencore's total production. SMM believes that if the suspension of production is really implemented, there is a significant direct effect on the boost of cobalt prices. In fact, cobalt prices have begun to pick up last week, but the news did vibrate the A-share small metal plate.

From the point of view of Huayu cobalt industry and cold cobalt industry, two stocks sealed a word board in early trading this morning, and rose by the limit at the beginning of trading. From a spot point of view, the price of electrolytic cobalt has been showing signs of a pullback since last week, coupled with news of the shutdown of Glencore cobalt mine, which is good news to stimulate the share prices of both companies to rise.

Cobalt prices rose first and then fell in 2018. Cobalt prices continued to rise in the first quarter, after May, due to oversupply of raw materials and other factors, cobalt prices began to fall, all aspects of the industrial chain generally began to reduce inventory, reduce the volume of individual purchases, at the same time, some traders and institutions profit selling exacerbated the price decline. In particular, after entering the fourth quarter, the price of domestic cobalt products accelerated to fall.

From the point of view of Huayu cobalt industry, cobalt raw material is the key resource of cobalt products production enterprises in Huayu cobalt industry. Since 2003, Huayu Cobalt Industry has begun to inspect and expand its business in Africa. After many years of efforts, the company's DRC subsidiary has established a cobalt and copper resources development system integrating mining, mineral processing, cobalt-copper hydrometallurgy and pyro-smelting in the main mining areas of the Democratic Republic of the Congo. Effective preservation of cobalt raw materials is the key resource for cobalt production enterprises.

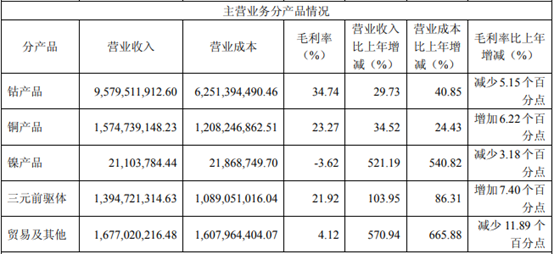

In 2018, Huayu Cobalt Industry followed the industry trend, seized the market opportunity, accelerated the pace of transformation and upgrading to the new energy lithium power material industry, and gave full play to the industrial synergy advantages of resources, smelting, materials and market. The output and sales volume of leading products have increased. For the whole year, the production of ternary precursors was 12834 tons, an increase of 20.24 percent over the previous year, and the sale of ternary precursors was 13111 tons, an increase of 57.39 percent over the previous year. 24354 tons of cobalt products were produced in the whole year (including 375tons of commissioned processing and 1726 tons of entrusted processing), and the production scale of cobalt products continued to lead the world.

In fiscal year 2018, Huayu Cobalt realized operating income of 14450762951.95 yuan, an increase of 49.7% over the previous year, a net profit of 1524665501.53 yuan, down 19.14% from the previous year, and a net profit of 1528098517.04 yuan belonging to the owner of the parent company, down 19.38% from the previous year. The company achieved a net profit of 1.912 billion in the first three quarters, but in the fourth quarter, due to the rapid decline in the price of domestic cobalt products, the company needed a certain period from the purchase of raw materials to the shipment of finished products. The decline in prices led to the loss of raw materials and unsold products, but also weakened the profitability of cobalt products.

Description of production and sales

Looking at the operating situation of the cold sharp cobalt industry, in 2018, the total operating income was 518.3963 million yuan, down 29.69% from the same period last year, of which the main business income decreased by 29.71%. In the current period, the net profit attributable to the common shareholders of listed companies was-55.3208 million yuan, down 121.71% from the same period last year. The decline in operating income and the decrease in net profit attributable to common shareholders of listed companies were mainly due to the decline in cobalt prices and the provision for lower inventory prices.

From the basic production and management status of Huayu cobalt industry and cold sharp cobalt industry, cobalt production and processing enterprises have been greatly affected by the decline of cobalt prices in 2018. Now cobalt prices have risen to the bottom, which is expected to reduce the pressure on the production and operation of related enterprises.

Hong Lu, a senior analyst at SMM, expects the cobalt electrolysis rebound to be about 20 per cent. The price of cobalt salt, which is highly bundled with the new energy vehicle industry chain, will rise with the rebound in the price of electrolytic cobalt.

Cobalt prices are expected to fluctuate upward. Benefiting from the rebound in cobalt prices, the profit inflection point of listed companies in the cobalt industry is expected to have arrived.

Shengang Securities said that at the current time, lithium battery-related targets have a very strong configuration value. On the industrial side, due to the uncertainty brought about by the end of the transition period at the end of June in May and June, and the overdraft effect brought about by the switch from country five to country six, the market is more cautious, and battery companies and material manufacturers in various links have reduced the operating rate, mainly to digest inventory. As July officially enters the post-transition period, the start-up rate will pick up under the stimulus of policy, and the third quarter will become an inflection point of profit. Superimposed overseas lithium battery production expansion began to accelerate, will drive the industrial chain related companies to achieve a rebound in performance.

"Click to enter the registration page

Scan QR code and apply to join SMM metal exchange group, please indicate company + name + main business