SMM7, 19th, news:

Part I: starting with the amount of products sold by the project

1. Three industry giants join hands: Qingmeibang New Energy Materials Co., Ltd.

According to an announcement issued at the end of September 2018, Jingmen Greenmei, a subsidiary of the company, signed a joint venture agreement with Xinzhan International (a subsidiary of Qingshan Iron and Steel Co., Ltd.), Guangdong Bangpu, Indonesia's IMIP Park, Osaka and Societe Generale on September 28, 2018, on the construction of a battery-grade nickel chemical (nickel sulfate crystal) (50, 000 tons of nickel per year) project produced by Indonesia's laterite nickel mine.

The name of the joint venture is "Qingmeibang New Energy Materials Co., Ltd." and its English name is "PT.QMB New Energy Materials". The joint venture has a total investment of US $700 million and a registered capital of US $210 million. Business scope: nickel resources development and sales, battery grade high purity nickel sulfate, cobalt sulfate, manganese sulfate development, production and sales, electrodeposition of copper and other chemical raw materials production, purchase and sale. It is expected that the initial goal is to build a wet production and smelting capacity of not less than 50, 000 tons of nickel metals and 4000 tons of cobalt metals, and to produce 50, 000 tons of nickel hydroxide intermediates, 150000 tons of battery-grade nickel sulfate crystals, 20, 000 tons of battery-grade cobalt sulfate crystals and 30, 000 tons of battery-grade manganese sulfate crystals, so as to adjust the product structure and expand the production scale according to the needs of the global market in the future.

The project plans to jointly invest US $700m, of which 21 per cent is owned by Aoyama Capital, 36 per cent by Jingmen Greengmei, a wholly owned subsidiary of Greengmei, 25 per cent by Guangdong Bang Pu Circular Technology, which has a stake in Ningde era, and 18 per cent by Indonesia's IMIP Park and the Japanese company Osaka and Societe Generale.

At the same time, Greene said in the announcement that the foreign investment will be funded in instalments through its own funds or through other forms of financing, and will not adversely affect the financial and operating conditions of the company.

In January 2019, the foundation laying ceremony of Qingmeibang New Energy Materials Company was held in Qingshan Park, Indonesia Economic and Trade Cooperation Zone.

2. Calculation: is the valuation of the project related to the price of nickel? Compared to September 2018 and now

Come to the conclusion directly:

After the calculation of option 1, it is concluded that because the cobalt price is too weak, even if the nickel price is pulled up, and even affects the nickel salt price, it is not very helpful to the total value of the project. If it is really for the total value of this financing project to drive the nickel price, I am afraid the "pig teammate" cobalt price is more critical.

Plan 2 after the calculation of the conclusion: according to metal prices, crazy nickel prices turn the tide, not only let their own value return, but also successfully make up for the decline in cobalt prices caused by the decline in the amount of the project.

The project is determined to go into production in 2020, so 2019 is a key investment and construction period, but there has been no news of further progress since the foundation was laid in January.

According to Indonesian Industry Minister Airlangga Hartarto in an interview, the factory has a total investment of US $700 million and can earn US $800 million a year, creating 2000 jobs.

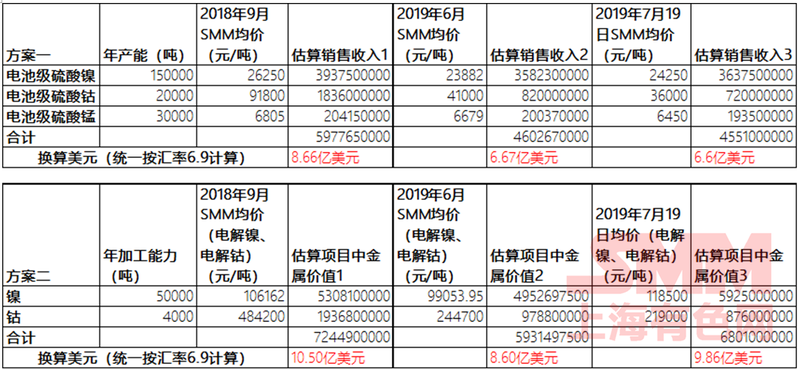

SMM extracted two time points in September 2018 and May 2019 to measure the value of products that can be sold after full production (using the domestic ex-factory price including tax, regardless of tariffs, miscellaneous fees, freight and other factors):

The results show that, at a uniform exchange rate of 6.9, the total value of the project could easily exceed $800 million for each product at September 2018 prices.

If, according to gossip, the bank evaluates the value of the project at an 80% discount when applying for financing, the latest product sold under either option will not be worth $800 million.

Part II: from the perspective of nickel industry chain

3. Cost advantage analysis of nickel sulfate production by MHP

Conclusion: in the long run, for nickel sulfate enterprises, if new capacity leads to overcapacity in the future and the nickel sulfate industry enters a low-profit state, assuming that only low-cost enterprises can survive, then enterprises using MHP to produce nickel sulfate have a real cost advantage. Due to the existence of nickel bean dissolution route, the excess capacity of nickel sulfate is inevitable in the future.

For the latest analysis of the profit margin advantage of MHP in the production of nickel sulfate, see SMM "[SMM Analysis] does the sharp rise in nickel prices lead to the recovery of factory profits in the nickel sulfate market?" One article

The nickel sulfate production of the project follows the route of laterite nickel ore-MHP (nickel cobalt hydroxide)-nickel sulfate. If questioned, will it also be related to the "competition" between the raw materials of nickel sulfate or the cost of producing MHP?

According to the understanding of SMM, most of the products in the global nickel intermediate industry are high ice nickel, MSP (nickel sulfide cobalt) and so on, which are distributed in Indonesia, Cuba, New Caledonia, Philippines, Finland, Australia and other countries. The process routes include HPAL, pressure leaching, biological heap leaching and so on. Some enterprises also produce intermediate products such as nickel carbonate, nickel oxide and so on.

Using HPAL technology and laterite nickel ore to produce MHP (nickel cobalt hydroxide), at present, there is only one enterprise that has been put into production, China Metallurgical Ruimu, with an annual MHP capacity of 32000 tons and overloading in 2018. The project was approved by the government in 2000. After the feasibility study and the signing of the agreement, the foundation laying ceremony was held in 2006 and put into production in December 2012. the total investment was 12.3 billion yuan, and the initial profit in 2018 was 232 million yuan.

According to its 2018 annual report, during the reporting period, the project continued to produce stable and high yield, with an average yield of 108.4 percent for the whole year. The cumulative production of nickel cobalt hydroxide containing nickel and cobalt metals was 35354 tons and 3275 tons respectively, both of which reached new highs. Both of them entered the top ten ranks in the world, and the production cost was lower than that of similar international projects. The main production technology and consumption indicators were better than the design indicators. The comprehensive operation management ability is in the leading level in the international similar project, realizes the sales income 2.6569 billion yuan, the project profitability enhances significantly, realizes the annual profit for the first time.

Although there has been previous experience, there has been a certain accumulation of technology, but the amount of investment in the early stage of the project is huge, and there are not many new projects that can be used for reference. So in the long run, do companies that use MHP to produce nickel sulfate have an advantage over those that use nickel beans? SMM analyzes:

Due to the fundamental cost gap, the proportion of nickel sulfate produced by nickel beans is not high, up to 25%, and intermediates and waste are still the mainstream raw materials for nickel sulfate production. Under extreme assumptions, if all of the nickel beans in LME stock were used to produce nickel sulfate, 700000 tons could be produced in a stock of about 140000 tons of LME, almost enough for the current year's consumption. In practice, therefore, in the foreseeable coming years, in the event of a shortage of nickel sulfate, the production of nickel sulfate from nickel beans as a supplement to the gap is sufficient, at least from a supply point of view.

(link: [SMM Analysis] the proportion of primary nickel used in the production of loss-making nickel sulfate from nickel beans / nickel powder in the precursor plant will be reduced to 0%? Https://news.smm.cn/news/100943856)

4. Cost analysis of MHP production from laterite nickel mine

Conclusion: the nickel intermediate product superimposed the long-term expectation of the increase of new energy demand, and the demand situation in the future is considerable. However, the huge investment in the early stage is a big problem to be solved in the production of MHP project in laterite nickel mine. If nickel prices remain depressed for a long time, it will indeed have a significant impact on the expected return on investment in new projects that produce intermediates.

From the point of view of the cost of producing intermediate products: according to SMM research, enterprises producing intermediate products in nickel sulphide mines are limited by resources, costs and other reasons. Some overseas mining enterprises are carrying out feasibility studies because of the hot concept of new energy, but there are also long processes that can not be put into production in the short term. Only Zorlu Holding has a potential new capacity of 10, 000 metal tons / year in Turkey. The cash cost of existing capacity ranges from $5000 to $12,000 per metal ton.

In the next few years, the new production capacity of intermediate products will be concentrated in Indonesia and the Philippines. The minimum cash cost of producing MHP from laterite nickel mine is only US $6000 / metal ton, which is obviously superior to that of other routes, but considering depreciation, the total cost can reach more than US $10000 / metal ton. "bitter before sweet" can be said to be the only way for this kind of project. If the nickel price is low for a long time, it will indeed affect the expected return on investment of the new project for the production of intermediate goods to a great extent.

Related links (panoramic, Castle Peak Holdings Group official website):

Grimm: announcement on the signing of the Joint Venture Agreement on the Construction of Battery-grade Ni Chemicals (Nickel Sulfate crystals) (50, 000 tons of Ni / year) by Jingmen Greimei, a subsidiary of the Company, with Xinzhan International, Guangdong Pang Pu, IMIP Park, Indonesia, Osaka and Societe Generale

Grimm: announcement on the project progress of the "Indonesian laterite nickel mine production of battery grade nickel chemicals (nickel sulfate crystals) (50,000 tons of nickel per year)" invested by the company's subsidiaries and the foundation laying activities held in Indonesia

Minister of Industry: Molowali Industrial Park becomes the driving force for the decline of the metal industry

Scan QR code and apply to join SMM metal exchange group, please indicate company + name + main business