Non-ferrous

Non-ferrous

Base Metals

Rare Earth

Scrap Metals

Minor Metals

Precious Metals

New Energy

Price CenterDatabaseProReportsEventsCar Insight

Language:

Language:

SMM July 05 News:

More than halfway through 2019, the new energy industry is gradually shuffling off the flashy, facing the dilemma of reshuffle. At this special time, the SMM New Energy Analysis team investigates and integrates the production data of China's core battery materials, summarizes the trend characteristics of the price trend, and makes a judgment and forecast of the price trend in the second half of the year.

This is the third part of a series of analysis reports, which describes the conclusions and forecasts of the core data of the positive industry:

From January to June 2019, the total output of ternary materials in China was 111000 tons, up 67.2 percent from the same period last year and 34.9 percent from the second half of 2018. SMM expects the output of ternary materials to be 134000 tons in the second half of 2019, up 64.9 percent from the same period last year.

From January to June 2019, China's total production of lithium iron phosphate was 41000 tons, up 62.6 per cent from a year earlier and 3.6 per cent from the second half of 2018. SMM expects lithium iron phosphate production to be 68000 tons in the second half of 2019, up 68.1 per cent year-on-year.

From January to June 2019, China's total production of lithium manganate was 27000 tons, up 9.6 per cent from a year earlier and 9.2 per cent lower than in the second half of 2018. SMM expects lithium iron phosphate production to be 33000 tons in the second half of 2019, up 10 per cent year-on-year.

From January to June 2019, the total output of lithium cobalt acid in China was 27000 tons, up 4 per cent from the same period last year and 0.6 per cent lower than in the second half of 2018. SMM expects lithium cobalt acid production to be 29000 tons in the second half of 2019, up 4.8 per cent year on year.

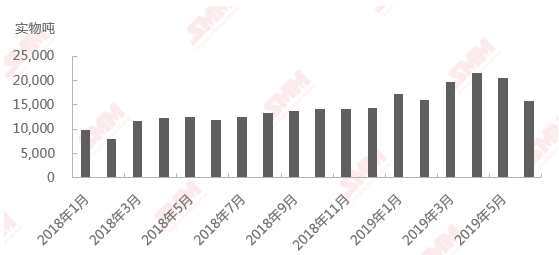

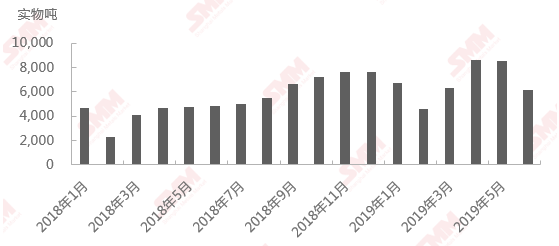

Production of Ternary Materials in China since January 2018

From January to June 2019, China's total output of ternary materials was 111000 tons, an increase of 67.2 percent over the same period last year and 34.9 percent over the second half of 2018. Of these, production exceeded 20,000 tons in April and May. In the first half of the year, two enterprises produced more than 10,000 tons, with CR10 of 67.6 per cent and CR5 of 43.9 per cent. In June 2019, China's total output of ternary materials was 15725 tons, an increase of 32.6 percent over the same period last year and a decrease of 23.3 percent from the previous month, the biggest drop since 2018.

According to SMM research, the output of ternary materials has been at an inflection point since May and declined to a large extent in June, mainly due to the following reasons:

1. The "Guowu" model has a far-reaching impact on the depot effect, a large number of short-term demand for new energy passenger cars has been replaced, and there is still room for future demand to be squeezed.

2. The transition period of superimposed new energy subsidies is over, and the industry enters a cold period after "rush loading";

3. Because of the frequent accidents of new energy vehicles in the first half of the year, consumers' attitude towards safety is in doubt, and the state strengthens the safety supervision of the industry, which will also directly affect the demand of new energy vehicles in the future.

As a result, the large-scale shutdown of ternary cells occurred in June, and it was transmitted to the manufacturers of ternary materials in the middle and late June to reduce their orders one after another, which was affected by the production reduction of C and B plants, and the single crystal 5 series and 6 series reduction was the main part of the ternary materials.

At present, the total production capacity of ternary materials has exceeded 420000 tons, the situation of overcapacity is obvious, and the competition among market participants is fierce. At the same time, with the leading effect trend of downstream battery factories, the customer structure is gradually concentrated, once the downstream battery customers come out.

Now large-scale production reduction, if the upstream raw material production plan is not adjusted in time, inventory will rise rapidly and passively in a short period of time. Considering that the raw material nickel, cobalt and lithium prices are in the downward channel, the material factory is not willing to keep more inventory, and is still aimed at active shipment. Therefore, once the terminal demand is less than the expected risk, the material factory has a strong willingness to reduce the opening rate.

According to SMM, there is no more good news in the current power market, the price game between mainframe factories and battery factories is still continuing, and the market demand is cold. SMM expects the three-way material plant to continue to be de-stocked in July, with production likely to decline further. At present, the battery enterprises represented by C are gradually transitioning the product system to high nickel, the order of 8-series ternary materials is less affected by the market fluctuation.

SMM estimates that in the third quarter, as the industry enters the traditional off-season, mainframe factories will take "high temperature leave" one after another, resulting in flat overall demand. However, with the launch of new models such as the Red Flag E-HS3, GAC AION LX, Mercedes-Benz EQC, MINI, Ford territorial EV and Toyota C-HR EV/ Yi Ze EV in the fourth quarter, the operating rate of battery plants may pick up somewhat, but due to the drag on demand in the second half of the year, the production and sales of new energy vehicles and power batteries may not be expected, and the output of ternary materials in the second half of the year is expected to be 134000 tons.

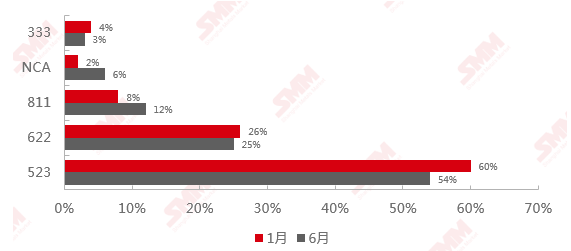

Comparison of Product structure of Ternary Materials in China in January and June 2019

From the point of view of yield structure, the trend of high nickel content is becoming more and more prominent. In June, the proportion of ternary material 523 accounted for 54%, which was 6%-622% lower than that in January this year, and slightly lower than that in January. High nickel 811% and NCA accounted for 12% and 6%, respectively, which were significantly higher than that in January.

Recently, the "whitelist" of power batteries has been officially cancelled, which has undoubtedly opened the door for foreign battery enterprises to enter China. At present, the products of Japanese and Korean enterprises represented by Panasonic, LG, Samsung SDI and SKI are mainly composed of 6 series and high nickel. For domestic battery factories, in the face of the upcoming international competition, it is the only way to develop high nickel technology to upgrade the performance structure of products. However, the development of technology is by no means overnight. If it is blindly promoted, it will pose a threat to the safety of new energy vehicles. In the first half of the year, whether the energy density requirement of the new energy subsidy policy in 2019 was not raised, or the Ministry of Industry and Information Technology carried out investigation on the hidden safety risks of the mainframe plant, it shows that the importance of safety has always been put in the first place. SMM expects that the output of high nickel ternary materials will increase steadily with the entry of foreign batteries and the strategic adjustment of leading battery factories in the second half of the year, but the growth space is limited, and the product structure of ternary materials will still be 5 series and 6 series.

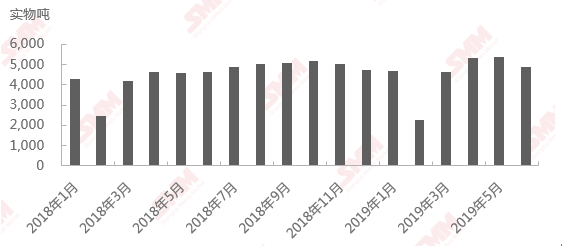

Lithium Iron Phosphate production in China since January 2018

From January to June 2019, China's total production of lithium iron phosphate was 41000 tons, an increase of 62.6 percent over the same period last year and 3.6 percent over the second half of 2018. In the first half of the year, the output of lithium iron phosphate in two enterprises exceeded 6000 tons, CR10 was 90.4% and CR5 was 65.4%. In June 2019, China's total production of lithium iron phosphate was 6180 tons, an increase of 28.5 percent over the same period last year and a decrease of 27.4 percent from the previous month.

Under the periodic influence of new energy bus, the production of lithium iron phosphate is mainly concentrated before the end of the year and the end of subsidy transition period. Since the second half of 2018, lithium iron phosphate battery has become the mainstream battery of new energy special vehicle because of its excellent safety performance and low cost. However, because the new energy special vehicle is still limited by the "right of way" and other factors in the first half of 2019, the output increase is not enough to pull the decline of the new energy bus market, and the demand for lithium iron phosphate is limited.

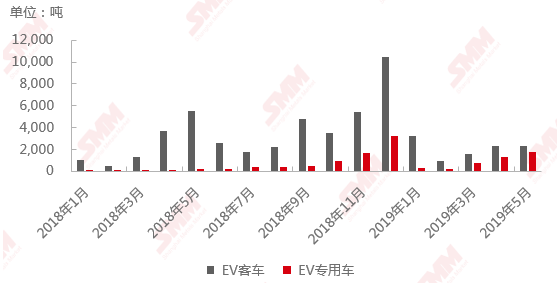

Demand for Lithium Iron Phosphate in 2018 / 2019.6 EV passenger cars and EV Special purpose vehicles

At the same time, affected by the depression of the new energy vehicle market, the leading battery factory reduced the production line of all types of batteries "equally" in June. Lithium iron phosphate battery market in 2018 has experienced a round of reshuffle, the concentration of market participants, corresponding to the upstream cathode material manufacturers are also obvious. At present, lithium iron phosphate is mainly used in the power market, because the energy storage market is still in the early stage of development, the support for market demand is limited. Once the leading battery plant has a large-scale reduction in production, affected by the higher concentration of the industry, the overall decline of lithium iron phosphate will be higher than that of ternary materials.

With the continuous decline of the new energy subsidy policy, mainframe plants require higher battery costs. At present, the cost of mainstream lithium iron phosphate single cell is 0.2 yuan lower than that of ternary single cell. At the same time, the advantage of safety performance of lithium iron phosphate battery is obvious. SMM believes that the loading rate of low speed passenger vehicles and special vehicles will continue to increase in the second half of the year. At present, the leading battery factory has also carried out the corresponding strategic adjustment to the production line, and gradually transferred some of the medium nickel production line to the high nickel and lithium iron phosphate production line, which has a certain support for the subsequent demand of lithium iron phosphate material. SMM estimates that production of lithium iron phosphate may pick up since July and is expected to be 68000 tons in the second half of the year.

Lithium manganate production in China since January 2018

From January to June 2019, China's total production of lithium manganate was 27000 tons, an increase of 9.6 percent over the same period last year and a decrease of 9.2 percent from the second half of 2018. In the first half of the year, five enterprises produced more than 2000 tons, with CR10 of 71.8 per cent and CR5 of 43.6 per cent. In June 2019, as a result of entering the traditional off-season of consumer batteries, demand for lithium manganate was reduced. The total output of lithium manganate in China was 4900 tons, an increase of 7.9 percent over the same period last year and a decrease of 8.6 percent from the previous month.

Lithium manganate downstream demand is scattered, due to low prices, mostly used in consumer batteries and small power and other cost-sensitive markets, especially in the second and third quarters of 2018, the price of ternary materials remained high, a large number of battery enterprises through the use of lithium manganate doping production to reduce costs.

SMM believes that the future consumer market, electric bicycles and electric tools market performance is good, the demand is more optimistic; power market, affected by the decline of subsidies, the follow-up power market or in order to reduce costs and improve battery stability, lithium manganate will be used for doping with ternary materials. As the lithium manganate market is more mature, the product structure is stable and there are many market participants, the periodicity of monthly output is more obvious. SMM expects demand for lithium manganate to rise steadily in the second half of the year, with production expected to be 33000 tons.

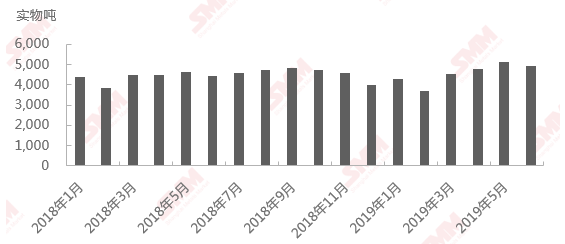

Lithium Cobalt production in China since January 2018

From January to June 2019, China's total production of lithium cobalt acid was 27000 tons, up 4 per cent from a year earlier and 0.6 per cent lower than in the second half of 2018. CR10 was 95.7% and CR5 was 78.4%. In June 2019, the total output of lithium cobalt acid in China was 4906 tons, an increase of 11 per cent over the same period last year and a decrease of 3.9 per cent from the previous month.

Lithium cobalt material and battery industry chain is mature, because it is mainly used in the traditional 3C field, with the formation of downstream customer oligopoly market, the concentration of material plants is also very high, and the monthly output change is mainly affected by the periodic changes of the industry.

SMM believes that 5G technology is still in its infancy, base station construction is mainly carried out in the second half of the year, and the large-scale promotion of 5G mobile phones will still take some time. At present, most consumers are in a wait-and-see state, the demand for replacement has been reduced, and the stimulation of lithium cobalt acid batteries in the downstream market may appear next year. SMM expects lithium cobalt to produce 29000 tons in the second half of the year.

SMM Cobalt Lithium Research team

Hong Lu 021 51666814

Ning Ziwei 021 51666780

Qin Jingjing 021 51666828

For queries, please contact Lemon Zhao at lemonzhao@smm.cn

For more information on how to access our research reports, please email service.en@smm.cn

![[SMM Report] Global and China's Lithium Resource Scarcity and Forecast](https://imgqn.smm.cn/production/admin/news/cn/thumb/cfGVG20180704164535.png?imageView2/1/w/176/h/110/q/100)

![[SMM Review] Cobalt & Lithium Prices May Record New Highs Post the CNY Holiday](https://imgqn.smm.cn/production/admin/news/cn/thumb/YZsRy20181023090947.jpeg?imageView2/1/w/176/h/110/q/100)