SMM, June 26, 2010:

According to a document issued by the Ministry of Industry and Information Technology on the 24th, "with effect from June 21, 2019, the Standard conditions for the Automobile Power Battery Industry shall be abolished (Ministry of Industry and Information Technology notice No. 22 of 2015), and the first, second, third and fourth batch of enterprise catalogues that meet the requirements of the specifications shall be abolished at the same time."

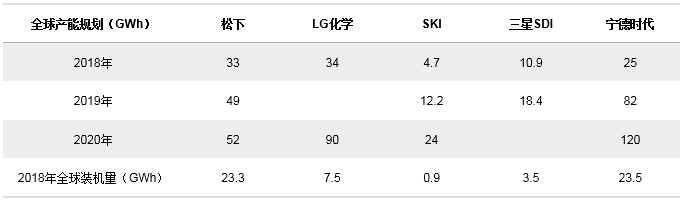

On March 24, 2015, the Ministry of Industry and Information Technology formulated the Standard conditions for Automobile Power Battery Industry. Since November 2015, the Ministry of Industry and Information Technology has issued a list of four batches of enterprises that meet the requirements of the specifications. A total of 57 battery enterprises have been shortlisted, and all of them are domestic battery enterprises. Since then, the "New Energy vehicle Promotion and Application recommended vehicle New catalogue" has also been gradually related to it. Only those new energy vehicles that are on sale are equipped with power batteries that meet the requirements and enter the "white list" catalogue, can they enjoy subsidies for new energy vehicles, while power batteries outside the catalogue cannot be subsidised. This has also directly led to LG, Samsung, Panasonic and other foreign battery enterprises slowly fade out of the Chinese market, on the contrary, it has greatly promoted the rise and development of domestic power battery enterprises. Ningde era ranks first in the global power battery installation volume in 2018 with the installed capacity of 23.5GWh.

In fact, with the sharp decline of China's new energy subsidy policy this year, foreign battery companies have been eager to re-enter China, the world's largest electric vehicle market. Panasonic has accelerated the pace of expansion in the domestic market since the beginning of the year. It has entered the supply chain system of FAW Toyota and Guangzhou Auto Toyota respectively. LG, Samsung and SKI have also stepped up their efforts to invest in battery factories in China. The cancellation of the "whitelist" has further accelerated the speed of market-oriented competition of domestic power batteries.

Throughout the current global power battery competition pattern, mainly around China, Japan and South Korea. According to this, SMM collates the latest development of power battery enterprises in Japan and South Korea. In the upcoming market competition, domestic battery enterprises know themselves and know each other, and constantly upgrade their own technical barriers, so that they are expected to stand firm in the reform and development of the industry.

First of all, from the three aspects of product performance, capacity planning and supply chain relationship, the representative power battery enterprises of China, Japan and South Korea are summarized as follows:

1. Panasonic

Panasonic's Chinese factory is located in Dalian, Liaoning. In 2015, Panasonic established a joint venture with Dalian Liao Wuer Electric Appliance Co., Ltd.

Dalian Panasonic Automotive Energy Co., Ltd., and invested 2.7 billion yuan to build a square lithium battery factory in Dalian for electric vehicles and

Plug in the hybrid car. On March 13, 2018, Panasonic Dalian factory officially produced and supplied goods with a production capacity of close to 5GW, which can meet the supporting demand for 200000 electric vehicles.

In addition, Panasonic has also set up a joint venture factory between Suzhou and Suzhou Jiexing to produce 18650 lithium-ion batteries used by Tesla.

It went into production in the second half of 2017 and achieved the annual production capacity of 100 million cells that year. Since then, the joint venture Lianyi New Energy landed in Jiangyin, Wuxi, on September 27, 2018, with a total production capacity of 30GWh. the first phase of the production capacity of 5GW is expected to be completed in September 2019.

Despite previous rounds of speculation, domestic Tesla's battery suppliers have finally spent on Panasonic, an old partner, which has also proved that Panasonic has a strong product technology system and customer stickiness. "cost + performance" of power batteries in the future is the king of development.

II. LG chemistry

LG Chemical officially entered the power battery market in 2009 and cooperated with Hyundai Kia of Korea to apply lithium battery products to commercial hybrid vehicles for the first time. On July 17, 2018, LG Chemical and Jiangning Binjiang Development Zone held a signing ceremony in Nanjing, with a total investment of US $2 billion LG chemical battery project settled in Binjiang. The construction and production of the Nanjing plant is an important step for LG Chemical to participate in the competition in the Chinese market. It is the third largest power battery factory after the Wukang Plant in South Korea and the Holland Plant in the United States. It will also be the most important power battery production base in the world for LG Chemical.

LG Nanjing factory construction began on October 23, 2018, the project will achieve full production in 2023, the annual production of power battery 32GWh. mainly produces power battery, energy storage battery and small battery. The factory plans to build 23 electrode and cell production lines, including 16 power batteries, 3 energy storage batteries and 4 small batteries. It is expected that the first phase of the project will achieve mass production in the fourth quarter of 2019.

III. SKI

SKI lithium electricity division has been concerned about the Chinese market for a long time, as early as 2013, with BAIC Group and Beijing Electronics holding Co., Ltd., established Beijing Electronic Control Aiskai Technology Co., Ltd., mainly produces the core of pure electric vehicles-power battery, with a total investment of 1 billion yuan, is the first Sino-foreign joint venture battery enterprise in China at that time. Of these, Beijing Electronic holding Co., Ltd. and Beijing Automotive Group Co., Ltd. jointly own 60 per cent of the shares, while SKI holds 40 per cent of the shares.

Since then, affected by China's new energy subsidy policy, SKI has failed to enter the list of Chinese battery companies, and it is difficult to compete with its peers without government subsidies. SKI announced the suspension of production at its joint venture plant in China in February 2017. Until entering the "whitelist of Automobile Power Battery and hydrogen fuel Cell Industry (first batch)" released in May 2018, SKI announced at the end of 2018 that it would restart the project of setting up a joint venture battery plant with BAIC Group and Beijing Electronics holding Co., Ltd., in Changzhou, Jiangsu Province, and will invest RMB 5 billion to build a power battery factory with annual production of 7.5GWh in Changzhou. The new plant is expected to be completed in the second half of 2019 and start production in early 2020.

IV. Samsung SDI

Samsung SDI is a leader in square power batteries. In 2008, Samsung SDI and Bosch formed a joint venture with SBLimotive, a power battery company, to start the car power battery business. In 2015, Samsung SDI Tianjin plant was established, mainly engaged in the development and production of circular lithium-ion batteries, including automotive energy power batteries, and later said at the end of 2018 that it would adjust part of the product structure of Tianjin plant and invest in new projects such as power battery production line and vehicle MLCC plant (multi-layer ceramic capacitors). In addition, the Xi'an plant (Samsung Huanxin), a joint venture between Samsung SDI and Anqing Huanxin and Gaoke Group, was completed and put into production in October 2015, but the expansion plan was suspended in 2017 due to obstacles to the development of the domestic market. Since then, until December 2018, Samsung SDI will restart the second phase of the power battery production base in Xi'an, where it will invest a total of 1.7 trillion won (10.5 billion yuan). Upon completion of the project, five 60Ah lithium-ion power battery production lines will be formed.

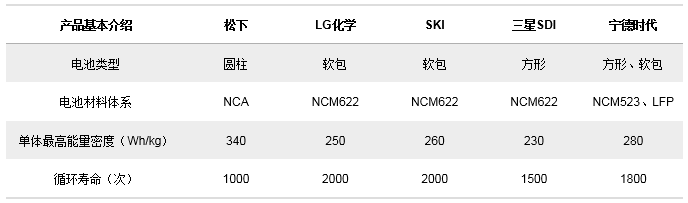

As China's largest power battery enterprise Ningde era battery system is still dominated by NCM523, and South Korean battery enterprises have transitioned to the NCM622 system, and plans to launch high nickel products in 2019, and Panasonic also has the highest energy density products on the market by virtue of the NCA system, we believe that the cancellation of the "white list" will also speed up the process of domestic power battery enterprises to transition to high nickel products. According to SMM, the current Ningde era has begun to suspend the nickel production line, to high nickel production line, this trend will be more obvious in the second half of the year.

SMM Cobalt Lithium Research team

Hu Yan 021 51666809

Hong Lu 021 51666814

Ning Ziwei 021 51666780

Qin Jingjing 021 51666828