Berita SMM, 7 Juli:

Pasar logam:

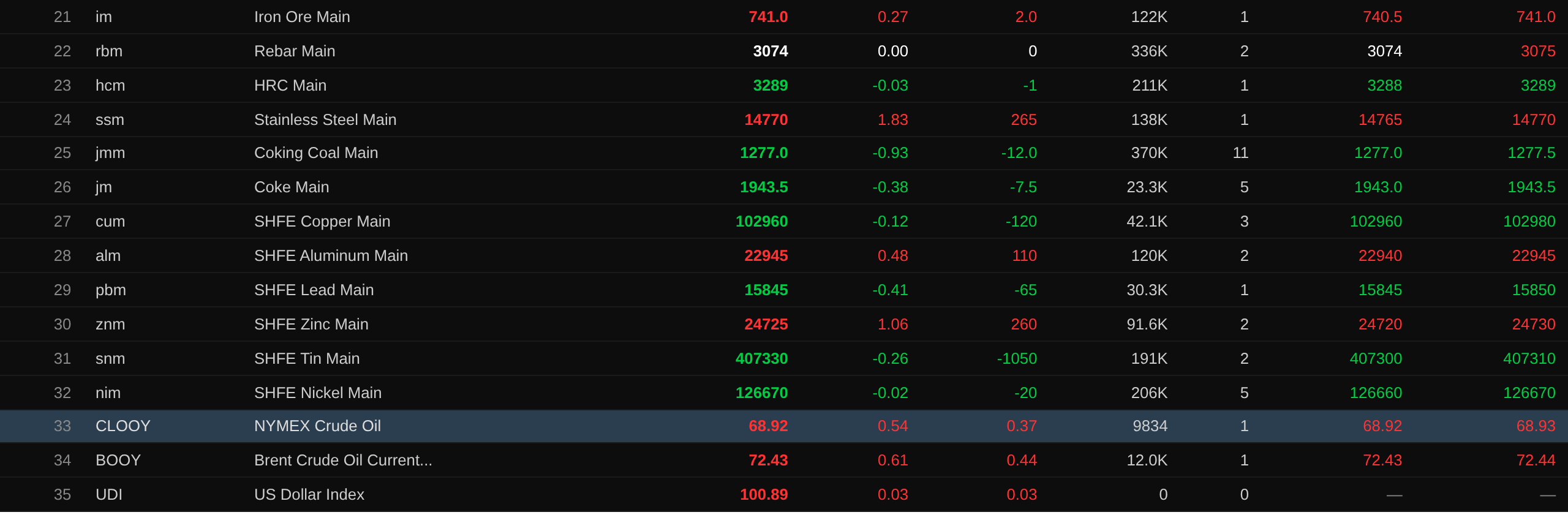

Hingga penutupan siang, logam dasar di pasar domestik sebagian besar melemah, dengan tembaga SHFE turun 0,12% dan aluminium SHFE naik 0,48%. Timbal SHFE turun 0,41%. Seng SHFE naik 1,06%. Timah SHFE turun 0,26%. Nikel SHFE turun 0,02%.

Selain itu, kontrak berjangka aluminium tuang yang paling aktif naik 0,42%, sementara kontrak alumina paling aktif turun 0,44%. Kontrak litium karbonat paling aktif turun 2,22%. Kontrak logam silikon paling aktif turun 0,24%. Kontrak berjangka polisilikon paling aktif sedikit melemah.

Logam ferrous sebagian besar melemah. Bijih besi naik 0,27%, rebar datar di 3.074 yuan/mt, dan hot-rolled coil sedikit turun. Baja tahan karat naik 1,83%. Untuk kokas batubara dan kokas: kontrak kokas batubara paling aktif turun 0,93%, dan kontrak kokas paling aktif turun 0,38%.

Logam dasar luar negeri: hingga pukul 11:42, logam LME sebagian besar melemah. Tembaga LME turun 0,32%, aluminium LME naik 0,22%, dan timbal LME turun 0,19%. Seng LME naik 0,25%, timah LME turun 0,92%, dan nikel LME turun 0,79%.

Logam mulia: hingga pukul 11:42, emas COMEX turun 0,57% dan perak COMEX turun 1,48%. Logam mulia domestik: emas SHFE turun 0,83%, dan kontrak perak SHFE paling aktif turun 2,3%.

Selain itu, hingga penutupan siang, kontrak berjangka platinum paling aktif turun 1,72%, dan kontrak berjangka paladium paling aktif turun 0,98%.

Hingga penutupan siang, kontrak berjangka kontainer pengiriman Eropa paling aktif melanjutkan penurunan hari perdagangan sebelumnya, turun lebih lanjut 5,03% menjadi 2.446,5 poin.

Hingga pukul 11:42 pada 7 Juli, pergerakan siang pada beberapa kontrak berjangka:

Pasar Spot dan Fundamental

Aluminium: Hari ini, kontrak berjangka terus naik, sementara spot di Tiongkok Selatan tertekan dan melemah. Kemarin, selisih harga spot-futures sempat menguat tajam, ditambah dengan harga absolut yang naik empat sesi berturut-turut ke level lebih tinggi. Dengan kedua indikator yang tinggi, sebagian besar pemasok aktif menjual untuk merealisasikan keuntungan, dan pemotongan harga semakin umum; beberapa memilih menahan harga tetapi dengan efek minim. Kuotasi utama berada pada diskon -10 hingga 0 yuan/mt, dan peredaran melonggar...

Sisi Makro

Tiongkok:

[Bank Dunia Pertahankan Proyeksi Pertumbuhan PDB Tiongkok 2026] Pada 7 Juli, Bank Dunia merilis Update Ekonomi Tiongkok terbaru di Beijing. Laporan tersebut menyatakan bahwa meskipun menghadapi pasokan yang kuat, permintaan yang lemah, dan guncangan pasokan energi global, pertumbuhan ekonomi Tiongkok secara keseluruhan tetap tangguh, dan pertumbuhan ekonomi Tiongkok pada 2026 diperkirakan 4,4%. Dibandingkan dengan update sebelumnya yang dirilis Desember tahun lalu, proyeksi pertumbuhan tetap tidak berubah. (Xinhua News Agency)

[Operasi Reverse Repo PBOC Menghasilkan Penarikan Neto 59,5 Miliar Yuan pada Hari Ini] Hari ini, PBOC melakukan operasi reverse repo 7 hari sebesar 10 miliar yuan. Karena 69,5 miliar yuan reverse repo 7 hari jatuh tempo hari ini, menghasilkan penarikan neto 59,5 miliar yuan pada hari ini. (Aplikasi Jinshi Data)

[John Lee: Sistem Kliring Sentral Emas Hong Kong Mulai Uji Coba Hari Ini; Kontrak Berjangka Emas dalam Denominasi RMB Sedang Dipertimbangkan] Pada 7 Juli, John Lee mengumumkan bahwa Sistem Kliring Sentral Emas Hong Kong memulai uji coba hari ini dan pengembangan kontrak berjangka emas baru dalam denominasi RMB sedang dipertimbangkan. Hong Kong Exchanges and Clearing Limited akan menandatangani nota kesepahaman dengan PBOC tentang pembayaran dan kliring RMB lintas batas. Pasar emas Hong Kong mengalami peningkatan penting di tingkat infrastruktur, dengan sistem kliring dan penyelesaian emas resmi diluncurkan pada 7 Juli. Untuk mendukung sistem baru dan sekaligus menghidupkan pasar berjangka emas lokal, HKEX mengumumkan pembebasan biaya selama satu tahun untuk kontrak berjangka emas, berlaku mulai 7 Juli. (Wall Street CN) 》Klik untuk detail

Untuk dolar AS:

Hingga pukul 11:42, indeks dolar AS naik 0,03% menjadi 100,89. Gubernur Fed Waller menyatakan bahwa Federal Reserve AS tidak akan sengaja mempertahankan suku bunga rendah untuk membantu pemerintah AS membiayai defisit fiskalnya. Waller mencatat bahwa pasar tenaga kerja AS telah stabil, sementara inflasi kembali meningkat, yang berarti risiko dari inflasi kini melebihi risiko terhadap ketenagakerjaan—pembalikan total dari pertimbangan kebijakan setahun lalu. Ia menunjukkan bahwa meskipun ia mendukung pemangkasan suku bunga tahun lalu karena pelemahan pasar tenaga kerja, fokus kebijakan kini harus bergeser kembali ke pengendalian inflasi. Perhatian pasar beralih ke CPI Juni, yang akan dirilis pada 14 Juli, data inflasi penting terakhir sebelum pertemuan Fed pada 28-29 Juli. Meskipun harga minyak internasional telah turun ke sekitar $70/barel, pejabat Fed masih memperkirakan inflasi akan jauh di atas target 2% pada akhir tahun. Menurut alat CME "FedWatch": Probabilitas Federal Reserve AS mempertahankan suku bunga saat ini pada Juli adalah 74,3%, sedangkan probabilitas kenaikan suku bunga kumulatif 25 basis poin adalah 25,7%. Untuk September, probabilitas suku bunga tetap tidak berubah adalah 42,9%, probabilitas kenaikan kumulatif 25 basis poin adalah 46,2%, dan probabilitas kenaikan kumulatif 50 basis poin adalah 10,8%. (Aplikasi Jinshi Data)

Laporan PMI Jasa ISM AS menunjukkan bahwa aktivitas ekonomi sektor jasa terus meningkat pada bulan Juni. PMI Jasa tercatat 54, menandai bulan ke-24 berturut-turut berada di wilayah ekspansi. Miller, Ketua Komite Survei Bisnis Jasa ISM, menyatakan bahwa PMI Jasa Juni sebesar 54 turun 0,5 dari 54,5 pada Mei. Indeks Aktivitas Bisnis tetap di wilayah ekspansi, turun 2,3 dari 57,7 pada Mei menjadi 55,4. Indeks Harga turun menjadi 67,7 pada Juni, penurunan 3,6 dari 71,3 pada Mei, turun di bawah 70 untuk pertama kalinya sejak Februari. Indeks ini telah berada di atas 60 selama 19 bulan berturut-turut, dengan rata-rata 12 bulan sebesar 68. Diesel, bensin, minyak, dan komoditas terkait kembali disebut sebagai item dengan kenaikan harga terbesar pada Juni, namun beberapa responden juga melaporkan penurunan harga. Hal ini mungkin berasal dari perbedaan ketentuan kontrak untuk komoditas ini di berbagai perusahaan. Beberapa responden mencatat penurunan pembayaran untuk bensin dan diesel, namun ini bukan fenomena yang meluas. Kami memperkirakan situasi ini akan berlanjut selama beberapa bulan karena kenaikan harga minyak merambat melalui rantai pasok, namun dengan asumsi kemajuan terbaru dalam pengiriman minyak melalui Selat Hormuz berlanjut, akan ada sedikit keringanan pada musim gugur. (Aplikasi Jin10 Data)

Mata Uang Lainnya:

Menteri Negara untuk Kebijakan Ekonomi dan Fiskal Jepang, Shironai Minoru, mengatakan bahwa laporan media yang menyatakan pemerintahan Perdana Menteri Takaichi Sanae berusaha menurunkan suku bunga benar-benar tidak akurat. Berbicara dalam konferensi pers reguler di Tokyo pada hari Selasa, Shironai mengatakan, “Laporan bahwa pemerintah akan mendorong suku bunga rendah sebagai bagian dari kebijakan ekspansi fiskal tidak berdasar. Jika maksud kami tidak tersampaikan dengan tepat, kami akan bekerja lebih keras untuk meningkatkan pemahaman.” Pernyataannya muncul saat pasar keuangan mencermati bagaimana Takaichi Sanae akan menerapkan strategi ekonominya melalui investasi besar-besaran tanpa menambah beban utang yang sudah berat. Shironai menghadiri rapat dewan Bank of Japan bulan lalu sebagai perwakilan pemerintah, di mana para pembuat kebijakan menaikkan suku bunga acuan menjadi 1%, tertinggi dalam 31 tahun. (Aplikasi Jin10 Data)

Data:

Hari ini akan dirilis data produksi industri Jerman bulan Mei yang disesuaikan secara musiman (MoM), indeks harga rumah Halifax Inggris bulan Juni yang disesuaikan secara musiman (MoM), neraca perdagangan Prancis bulan Mei, perubahan mingguan tenaga kerja ADP AS untuk pekan yang berakhir 20 Juni, neraca perdagangan AS bulan Mei, dan cadangan devisa Tiongkok bulan Juni, di antaranya. Selain itu, perhatian harus diberikan pada: Turki menjadi tuan rumah KTT NATO hingga 8 Juli; kantor Perwakilan Dagang AS mengadakan dengar pendapat publik tentang usulan pemberlakuan tarif tambahan terhadap 60 ekonomi global; Samsung Electronics akan merilis panduan laba Q2-nya.

Minyak Mentah:

Hingga pukul 11:42, kedua harga minyak mentah acuan naik, dengan WTI naik 0,54% dan Brent naik 0,61%. Jendela singkat pelonggaran AS-Iran kembali menghadapi kebuntuan, mendorong harga minyak lebih tinggi. Pasar mengamati perkembangan geopolitik dan perubahan prospek pasokan-permintaan.

Jumlah kapal yang melintasi Selat Hormuz terus rebound. Menurut laporan, total 160 kapal melewati selat tersebut dari Senin hingga Sabtu pekan lalu, meskipun tingkat keseluruhan masih jauh di bawah norma sebelum perang. (Wall Street CN)

Seiring lonjakan pasokan global yang meningkatkan persaingan untuk pembeli, Arab Saudi memangkas harga jual resmi nilai utama minyak mentahnya untuk pelanggan Asia pada bulan Agustus sebesar yang terbesar dalam setidaknya 26 tahun. Menurut daftar harga, Saudi Aramco memotong harga minyak mentah Arab Light untuk Asia pada bulan Agustus sebesar $11 per barel, menjadi diskon $1,50 per barel terhadap patokan regional. Pemotongan ini lebih besar dari $8 per barel yang diharapkan dalam survei lembaga. Harga minyak mentah di Timur Tengah baru-baru ini turun. Setelah melanjutkan ekspor dari pelabuhan Ras Tanura di Teluk Persia, Saudi Aramco sementara menaikkan pengiriman minyak mentah menjadi sekitar 90% dari tingkat sebelum perang. Sebelum perang, Ras Tanura adalah pelabuhan muat utama untuk ekspor minyak mentah Saudi. Karena perang memblokir Selat Hormuz, Saudi Aramco mengalihkan sebagian besar aliran minyak mentahnya ke pelabuhan Yanbu di Laut Merah. Sebelumnya, kelompok produsen OPEC+ sepakat untuk melanjutkan peningkatan produksi kecil pada bulan Agustus. Sekarang, dengan kembalinya pengiriman di Selat Hormuz, produsen minyak Teluk seperti Arab Saudi, Irak, dan Kuwait akan dapat memanfaatkan kuota mereka yang lebih tinggi. (Aplikasi Jinshi Data)

Ikhtisar Pasar Spot:

►

►

►

►

►

►

►

►

►

►

►

![Dolar AS Garis Bulanan Turun, Garis Bulanan Minyak Mentah Melonjak Lebih dari 24%, LME Mengungguli SHFE, Garis Bulanan Tembaga, Aluminium, dan Emas Ditutup Positif [Pasar Semalam]](https://imgqn.smm.cn/usercenter/PeWqW20251217171735.jpg)

![Penarikan stok dari gudang menurun, tetapi pengosongan stok semakin cepat — Apakah logika pengosongan stok ingot aluminium di Tiongkok berubah? [Analisis SMM]](https://imgqn.smm.cn/usercenter/YYogD20251217171650.jpg)

![[SMM Flash News] Kinetic7 Mempromosikan Teknologi Hidrogen-on-Demand untuk Pasokan Energi Terdesentralisasi](https://imgqn.smm.cn/usercenter/JMPtY20251217171734.jpeg)