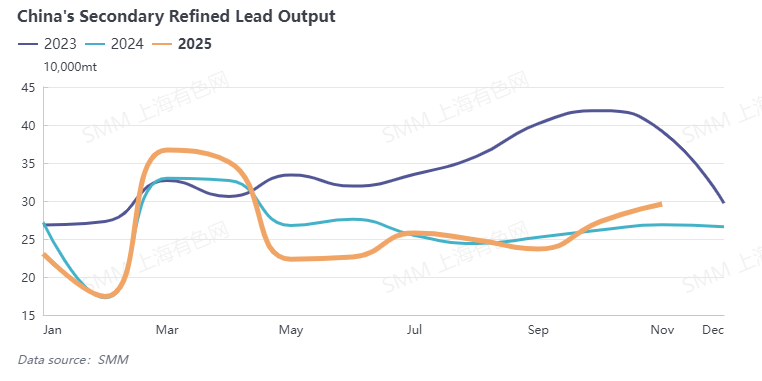

Secondary lead production in November 2025 increased significantly, up 7.78% MoM and 16.83% YoY; secondary refined lead production rose 8.5% MoM and 10.13% YoY.

Multiple secondary lead smelters in east China and north-west China resumed production in early November, while some smelters in central China and north China restarted in mid-November. In addition, smelters that resumed production in October operated stably in November, contributing significantly to the month's output. A large smelter in north China underwent maintenance and suspended production at the end of October due to equipment maintenance needs, and did not produce in November; a major secondary lead smelter in east China halted production in late November due to the renewal of its hazardous waste operation license; individual smelters in central China cut production in early November as environmental protection-related controls affected raw material arrivals. Elsewhere, sporadic production cuts occurred at some smelters in south-west China, south China, and east China due to weak lead prices.

Looking ahead to December, secondary lead production is expected to decline. A major secondary lead smelter in east China requires two months to renew its hazardous waste operation license, and its inability to produce in December is projected to reduce secondary lead output by over 5 kt MoM. Equipment upgrades or commissioning at certain large secondary lead smelters in central China and south-west China may collectively reduce secondary refined lead production by 4 kt. In addition, colder weather, environmental protection-related controls linked to heating-related air quality concerns in northern regions that may restrict smelter operations, the off-season for retiring e-bike batteries—the main type of waste lead-acid batteries—as well as a worsening supply-demand imbalance for raw materials and expectations of higher costs could dampen production enthusiasm among secondary lead smelters. Although smelters that resumed production in east China in November will ramp up output normally in December, providing some incremental supply, this will be "a drop in the bucket." Overall, December production is expected to decrease by approximately 10 kt MoM.