SMM November 28 News:

Key Points: The solid-state battery sector reached a critical period for industrialisation in November. Semi-solid-state batteries achieved breakthroughs in large-scale applications in consumer electronics, two-wheelers, ESS, and EV markets; all-solid-state battery R&D and pilot line construction accelerated, with Tinci, Solivis, and other companies making significant progress in the sulphide electrolyte field. Upstream material and equipment investment was active, and in the global competitive landscape, China demonstrated a clear speed advantage in industrialisation.

I. Review of Electrolyte Raw Material Production and Prices

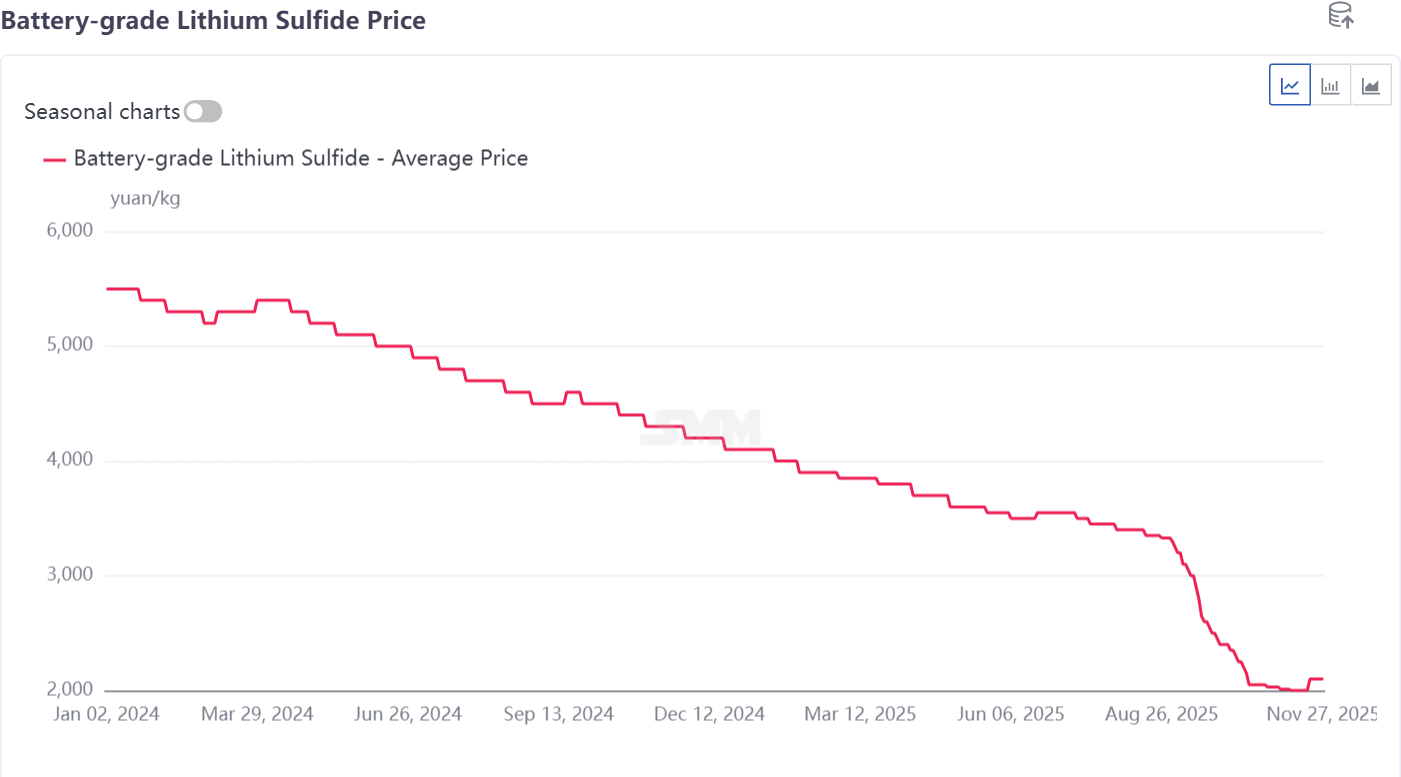

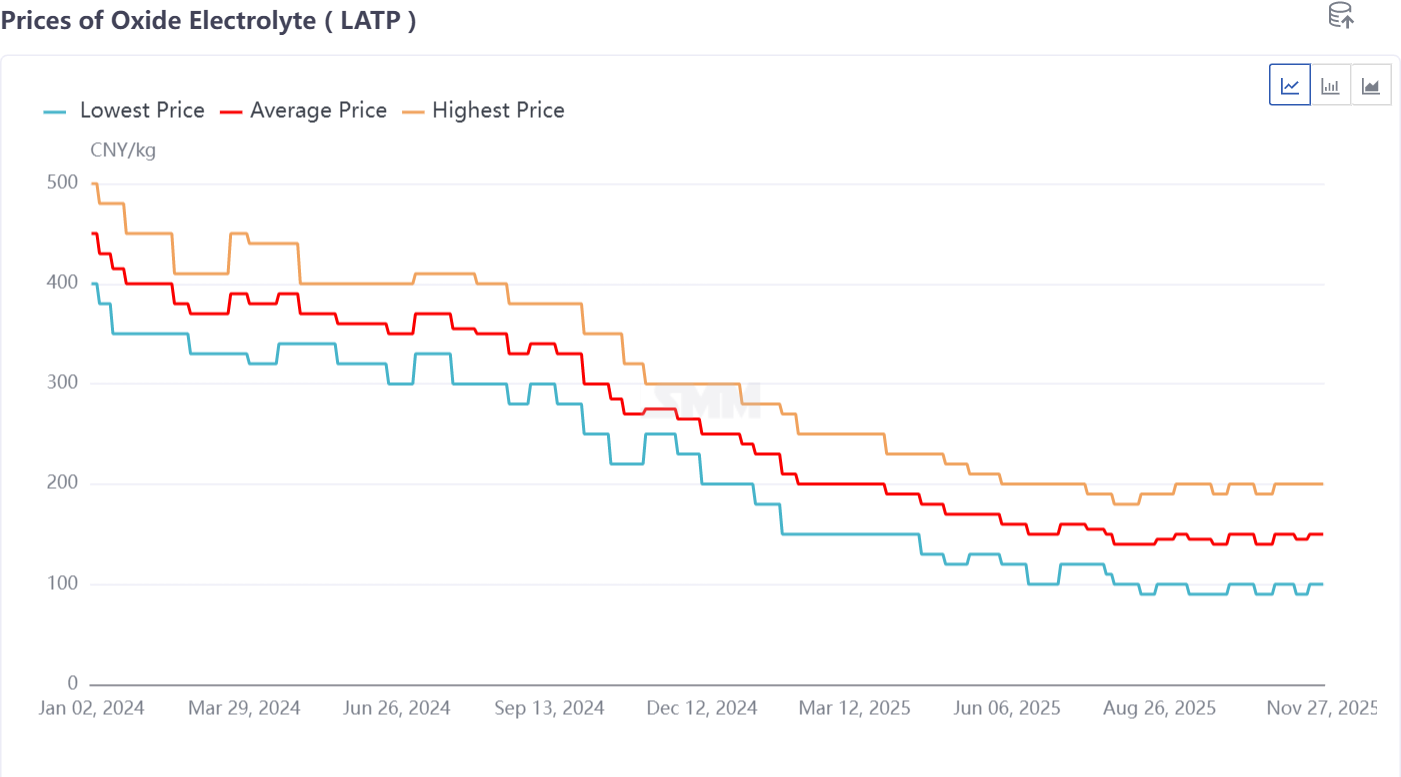

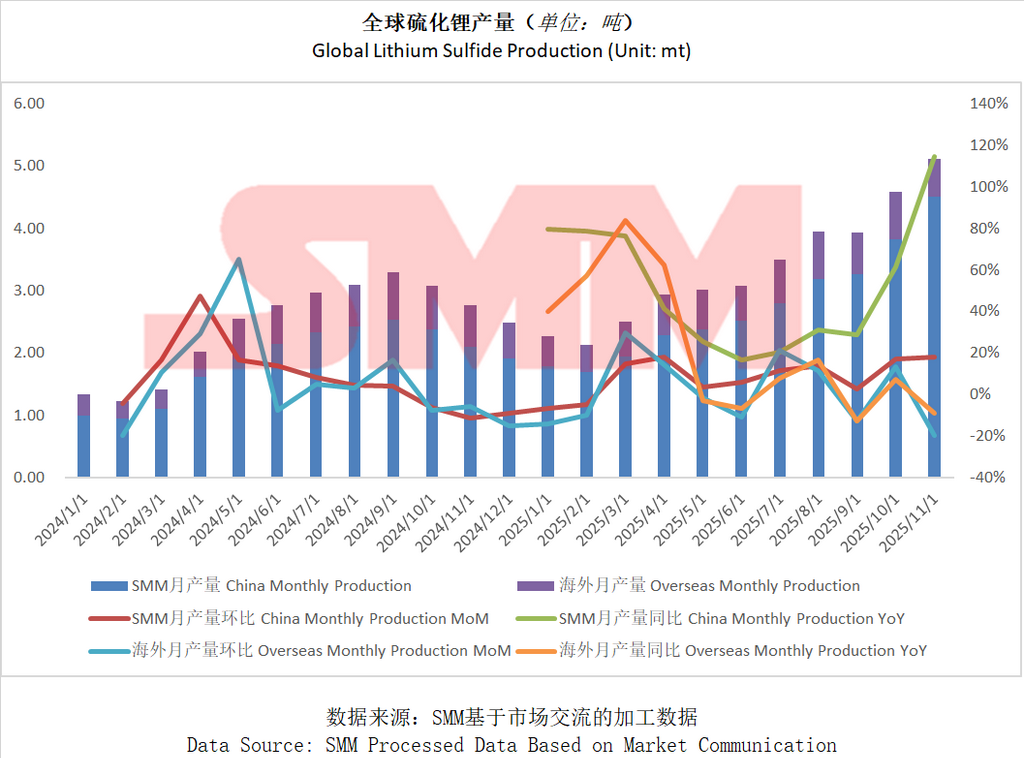

The price of lithium sulfide stabilised around 2,000 yuan/kg due to high market demand for cost-effective products. Meanwhile, the price of LATP oxide electrolyte steadily declined, currently hovering around 150 yuan/kg. Lithium sulfide production broke through 5 tons, setting a new record.

II. Technological R&D and Breakthroughs: Significant Progress in Core Materials for All-Solid-State Batteries

Electrolyte Material Competition Intensifies

The sulphide route became the focus this month. Tinci secured eight patents for sulphide electrolytes, establishing a high-performance technology system; South Korea's Solivis achieved the first batch production of sulphide electrolytes, with an ionic conductivity of 12 mS/cm and a significant reduction in costs.

Diversified Routes in Parallel: Ronbay Technology has kilogram-level preparation capabilities for sulphide and halide electrolytes; Yishitong's oxide electrolytes are in the laboratory stage; DFD's polymer route is ready for vehicle installation; Tsinghua University even developed an innovative soybean-based electrolyte.

Key Materials and Cell R&D

Cathode Materials: Ronbay Technology achieved ton-level shipments of 9-series high-nickel and 10-ton level shipments of 8-series.

Anode Materials: Silicon carbon anodes have become the mainstream direction, with Artisan New Materials commissioning a thousand-ton production line, Huayi Qingchuang launching low-cost products, and Tianmu Pioneer signing a 5 billion yuan major project.

Cell Performance: BAK Battery's polymer/oxide composite semi-solid-state cell achieved an energy density of 400 Wh/kg; TopTech's e-motorcycle-specific pouch semi-solid-state battery passed the needle penetration test.

III. Industrialisation and Market Penetration: Semi-Solid-State Batteries Lead the Market

Capacity Construction and Project Implementation

Semi-solid-state battery capacity expanded rapidly. Jingli New Energy's 150 million yuan project, producing 300,000 Ah per day, was quickly implemented; SVOLT Energy Technology built the world's largest 2.3 GWh semi-solid-state production line; Sunwoda's consumer semi-solid-state batteries exceeded 10 million units in cumulative production.

All-solid-state battery pilot lines were densely laid out. Tianqi Lithium and Yahua Group's 50-ton lithium sulfide pilot lines are expected to be completed by 2026; Sanwei Battery's 1 GWh sulphide solid-state battery project commenced.

Diversified Application Scenarios

Consumer Electronics: vivo Y500Pro smartphone was the first to use a 7,000 mAh semi-solid-state battery; Japan's CIO launched a semi-solid-state battery power bank.

ESS Sector: China Green Development's 200 MW/800 MWh semi-solid-state battery ESS station entered the final installation phase; Hovd One and EVE signed a contract to explore the application of solid-state batteries in outdoor power sources.

Power and Special Fields: GAC Group plans to conduct vehicle tests with all-solid-state batteries in 2026; Saik Power's sulphide solid-state battery project started, targeting the low-altitude economy.

IV. Industry Chain and Ecosystem Layout: Hot Investment in Equipment and Upstream Materials

Equipment Sector Benefits First

Lead Intelligent Equipment announced it had fully integrated the entire process for all-solid-state batteries, providing a complete line solution.

Haimuxing achieved exclusive technological leadership in ultra-thin coating and laser marking for solid-state battery-specific equipment.

Upstream Material Capacity Expansion

Lithium sulfide, as a core raw material, became a strategic investment focus. In addition to Tianqi and Yahua, Foshan Plastics and Zijin Mining, among others, jointly established a 100-ton project.

Oriental Zirconium invested 737 million yuan in chloro-oxide zirconium, a raw material for oxide electrolytes.

V. Policies and Capital: Dual Drivers for Industry Development

Strong Policy Support: MIIT, NDRC, and other departments issued consecutive documents, listing solid-state batteries and their key materials as key support areas for manufacturing pilot platforms and new energy consumption.

Continuous Capital Injection: Active financing and cooperation in the industry chain, such as the partnership between Hovd One and EVE, and BTRYAG securing $5.7 million in funding. Capital is concentrating on enterprises with core technologies and closed-loop technical capabilities.

VI. Summary and Outlook

In November 2025, the solid-state battery market exhibited distinct characteristics of "accelerated industrialisation, technological breakthroughs, and full-chain layout." As the current market leader, semi-solid-state batteries have successfully entered high-end consumer electronics, ESS, and EV sectors, achieving large-scale revenue. The competition for all-solid-state batteries focuses on patents, costs, and large-scale preparation capabilities for upstream core materials (especially sulphide electrolytes). The 2026-2027 period is expected to be a critical window for pilot line construction and validation. Overall, Chinese enterprises have established a first-mover advantage in industrialisation speed and depth of industry chain integration, and the global competitive landscape is taking shape.

According to SMM forecasts, all-solid-state battery shipments will reach 13.5 GWh by 2028, while semi-solid-state battery shipments will reach 160 GWh. Global lithium-ion battery demand is projected to reach approximately 2,800 GWh by 2030, with the EV sector's lithium-ion battery demand showing a CAGR of around 11% from 2024 to 2030, ESS lithium-ion battery demand at a CAGR of about 27%, and consumer electronics lithium battery demand at a CAGR of roughly 10%. Global solid-state battery penetration is estimated at about 0.1% in 2025, with all-solid-state battery penetration expected to reach around 4% by 2030, and global solid-state battery penetration potentially approaching 10% by 2035.

**Note:** For further details or inquiries regarding solid-state battery development, please contact:

Phone: 021-20707860 (or WeChat: 13585549799)

Contact: Chaoxing Yang. Thank you!