Non-ferrous

Non-ferrous

Base Metals

Rare Earth

Scrap Metals

Minor Metals

Precious Metals

New Energy

Price CenterDatabaseProReportsEventsCar Insight

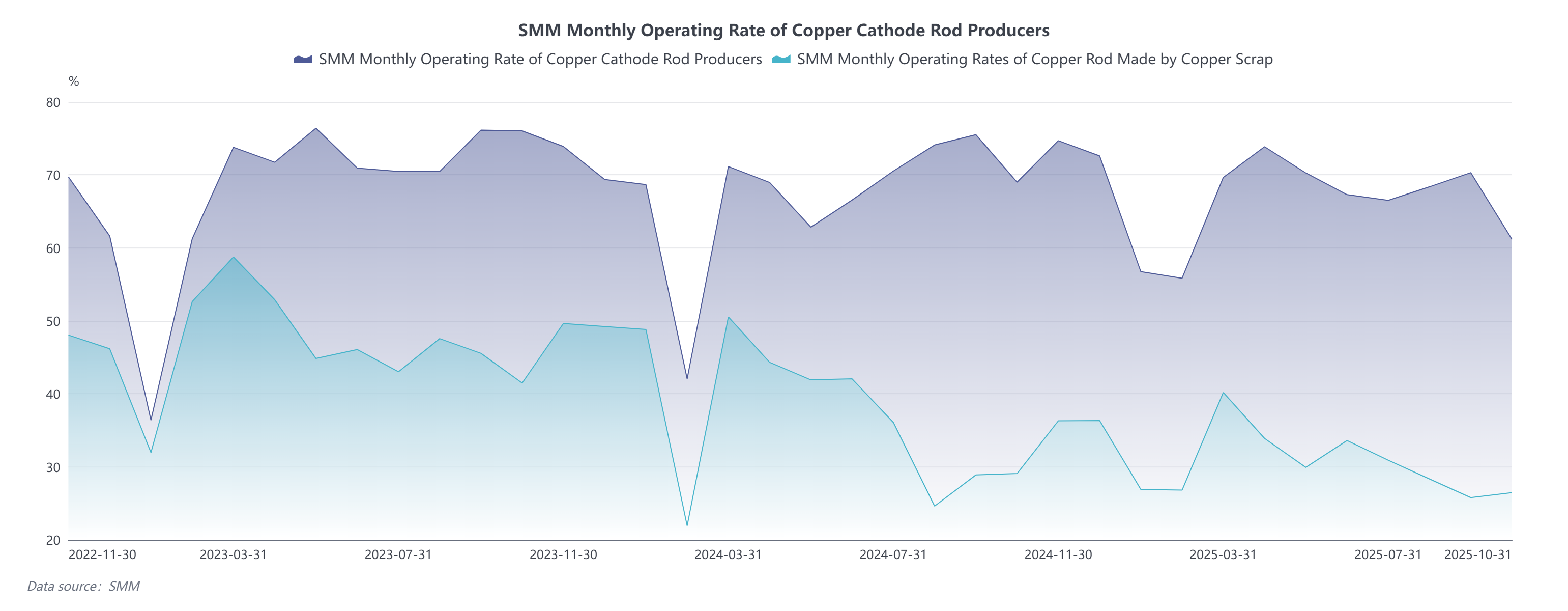

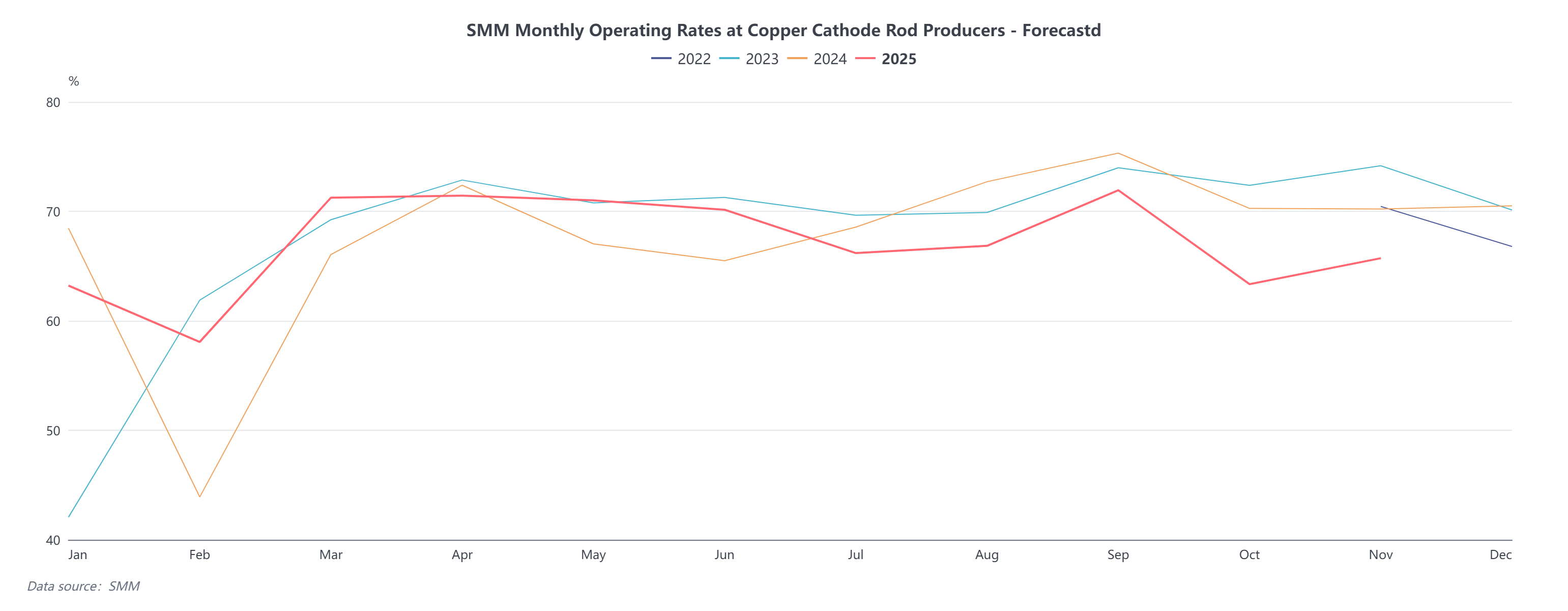

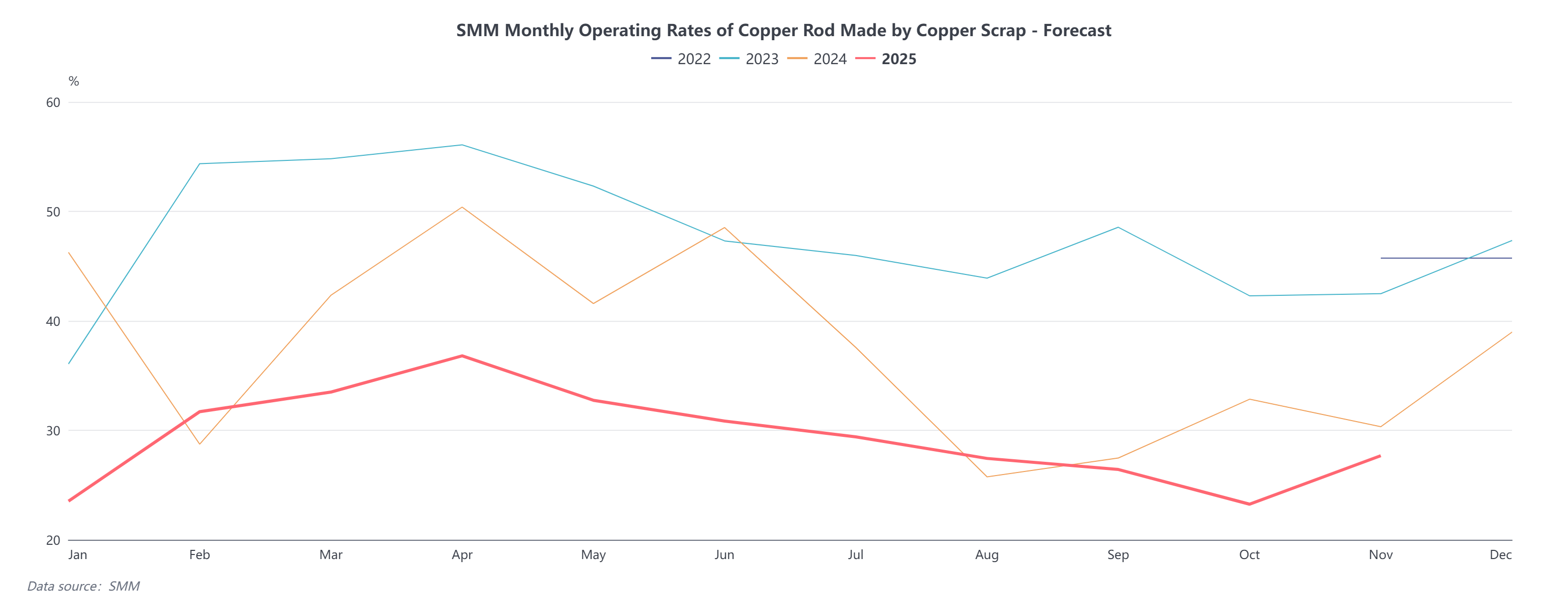

According to SMM statistics, national copper rod production in October was 984,600 mt, a decrease of 104,200 mt MoM, down 9.57%. Production of copper cathode rod recorded 838,100 mt, a decrease of 107,900 mt MoM, down 11.41%, dragging down the overall operating rate of the copper rod industry; production of secondary copper rod recorded 146,500 mt, an increase of 3,700 mt MoM, up 2.59%. In terms of operating rates, the operating rate for copper cathode rod enterprises in October was 61.15%, down 9.15 percentage points MoM and down 7.85 percentage points YoY (the operating rate in October last year was 69%); the operating rate for secondary copper rod enterprises in October was 26.46%, up 0.68 percentage points MoM and down 2.61 percentage points YoY (the operating rate in October last year was 29.07%).

I. Market Analysis of the Copper Cathode Rod Industry

The operating rate for copper cathode rod enterprises in October was 61.15%, down 9.15 percentage points MoM, and 2.2 percentage points lower than expectations; it decreased by 7.85 percentage points YoY. The core constraints for the significant decline in the copper cathode rod operating rate in October were the National Day holiday and surging copper prices, leading to the operating performance of copper cathode rod production in October 2025 falling short of expectations and being significantly lower than the same period last year.

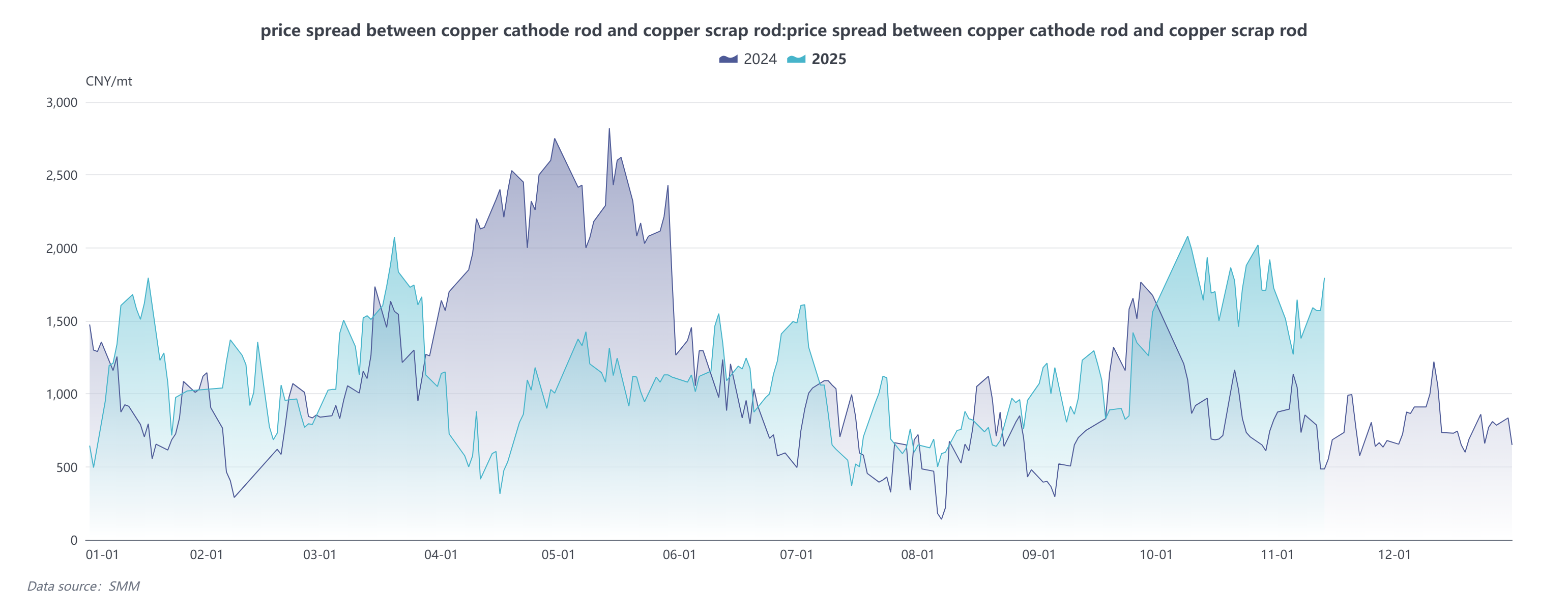

According to SMM analysis, the average price of SMM #1 copper cathode in October was 86,257.94 yuan/mt, up 5,593.62 yuan/mt MoM and up 9,294.88 yuan/mt YoY. Copper prices once again broke historical highs, severely suppressing procurement sentiment, with downstream acceptance of prices being low. Looking at specific consumption, the operating rate of downstream cable enterprises fell 4.37 percentage points MoM to 67.86%, and the operating rate of enamelled wire enterprises decreased 3.65 percentage points MoM to 64.47%. End-use demand was weak, peak season orders were not released as expected, and actual transaction demand downstream performed poorly. Most copper cathode rod enterprises reduced or halted production to consume finished product inventories. Additionally, the average price spread between copper cathode and secondary copper rod widened to 1,783.53 yuan/mt in October. To ease capital pressure, some downstream orders shifted to lower-cost secondary copper rod, further weakening demand for copper cathode rod.

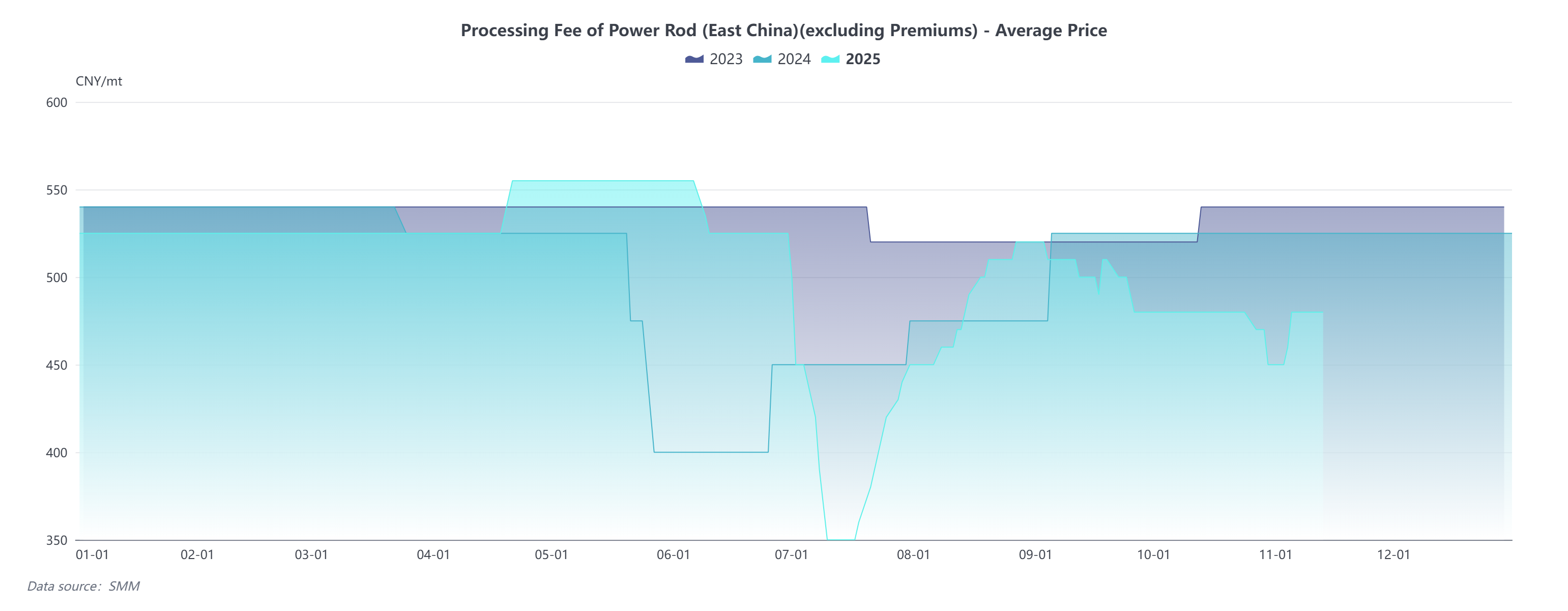

Price side, the processing fee for 8mm copper rod in east China showed a downward trend under pressure in October. The average processing fee excluding premiums and discounts in east China was 474.71 yuan/mt, down 28.02 yuan/mt MoM and down 50.29 yuan/mt YoY. Specifically, affected by high copper prices in October, downstream consumption remained weak, with processing fees from some traders reaching parity or even discounts. Copper cathode rod enterprises successively lowered processing fees to stimulate new orders. However, limited by production costs, the overall room for processing fee reductions was constrained.

II. Analysis of the Secondary Copper Rod Industry

The operating rate for secondary copper rod enterprises in October was 26.46%, up 0.68 percentage points MoM, but 0.64 percentage points lower than expectations, and down 2.61 percentage points YoY. The core reason for the slight MoM increase in the secondary copper rod operating rate in October was the gradual clarification of policies in certain regions and suppression by high copper prices, leading to a slight rebound in the operating rate, which remained lower than the same period last year.

Specifically, as support policies are expected to resume in some regions such as Jiangxi and Anhui in November, some enterprises resumed raw material procurement quotations and production at the end of October, boosting the overall industry operating rate. Furthermore, after the price difference between copper cathode and copper scrap widened, downstream wire and cable enterprises procured some secondary copper rod. However, suppressed by rising copper prices, new orders from end-users were limited, preventing significant improvement in secondary copper rod demand. Overall, in October, the secondary copper rod industry was affected by both wide fluctuations in copper prices and policy uncertainty, with the overall operating rate still lower than the same period last year.

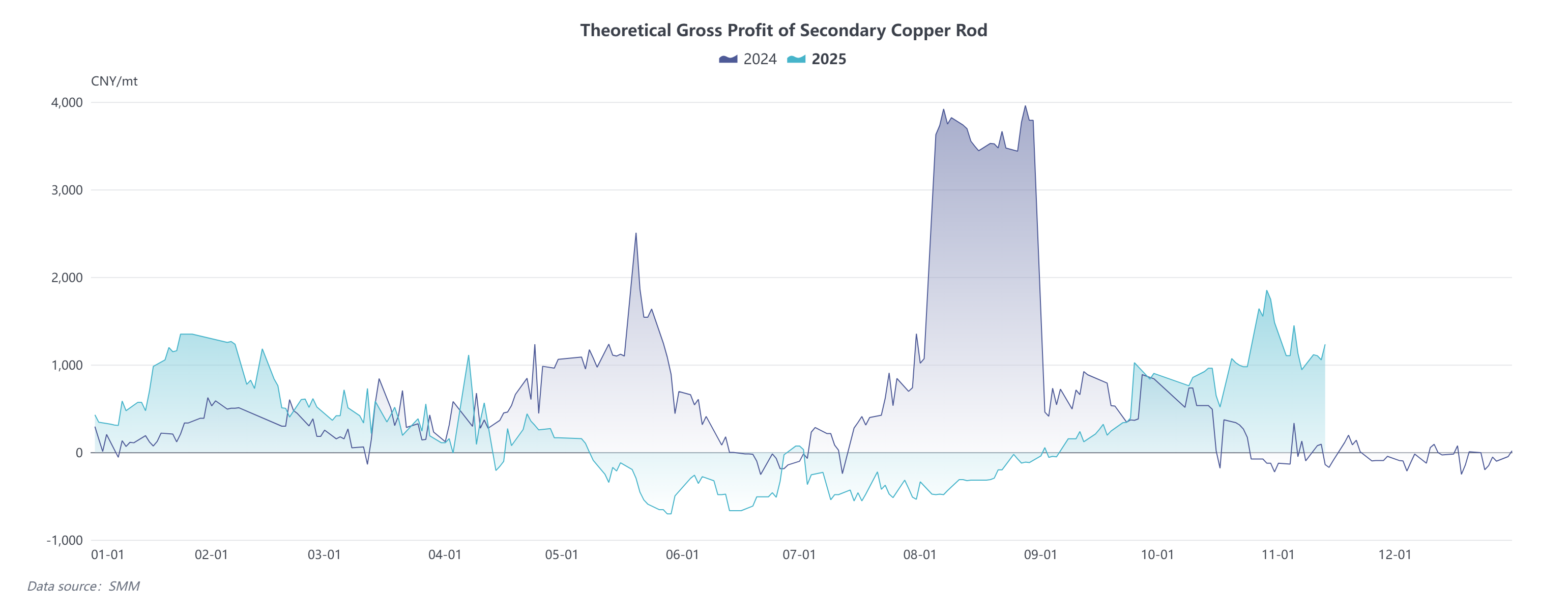

Price side, with copper prices continuing to surge, the average price spread between copper cathode and secondary copper rod in October widened by 697.39 yuan/mt MoM to 1,783.53 yuan/mt. The average discount of secondary copper rod in Jiangxi against futures widened by 796.5 yuan/mt MoM to 1,310.59 yuan/mt. The widening spread pushed the gross sales profit of secondary copper rod up by 808.48 yuan/mt MoM to 1,112.43 yuan/mt.

III. November Market Outlook

The operating rate for copper cathode rod enterprises in November is expected to be 65.72%, up 4.57 percentage points MoM and down 8.96 percentage points YoY; the operating rate for secondary copper rod enterprises is expected to be 27.68%, up 1.22 percentage points MoM and down 8.62 percentage points YoY. In November, copper rod enterprises resumed normal production, and the brief correction in copper prices at the beginning of the month stimulated a concentrated release of downstream orders. Meanwhile, although regions outside Jiangxi and Anhui have not yet received a clear response regarding supportive policies, secondary copper rod enterprises will maintain normal production to fulfill orders on hand as long as the policies are not explicitly canceled. Therefore, SMM expects total production in the copper rod industry to increase by 69,300 mt MoM to 1.0539 million mt in November.

By end-use industry, the operating rate in the cable industry is expected to rise by 4.01 percentage points MoM to 71.87% in November, supported by the resumption of normal production and the year-end push for annual output targets. The operating rate in the enamelled wire industry is projected to increase by 4.26 percentage points MoM to 68.73%, mainly due to the fading impact of the National Day holiday and relatively strong order performance in end-use sectors such as NEVs and transformers. The operating rate in the copper foil industry is anticipated to edge up 0.26 percentage points MoM to 84.49%, as demand across end-use sectors is expected to continue steady growth.

Overall, the national copper rod industry is expected to see a dual increase in the operating rates of both copper cathode rod and secondary copper rod in November, primarily benefiting from the dissipation of holiday effects, the correction in copper price center, and policy factors. Looking ahead to November, downstream acceptance of high copper prices is gradually improving, and the slight correction in copper prices is driving an increase in new orders, which is expected to boost the operating rate in the copper cathode rod industry. The secondary copper rod industry will maintain normal production amid ongoing policy uncertainty, with its future trajectory still depending on the specific implementation details of Notice No. 770.

For queries, please contact Lemon Zhao at lemonzhao@smm.cn

For more information on how to access our research reports, please email service.en@smm.cn