SMM November 16:

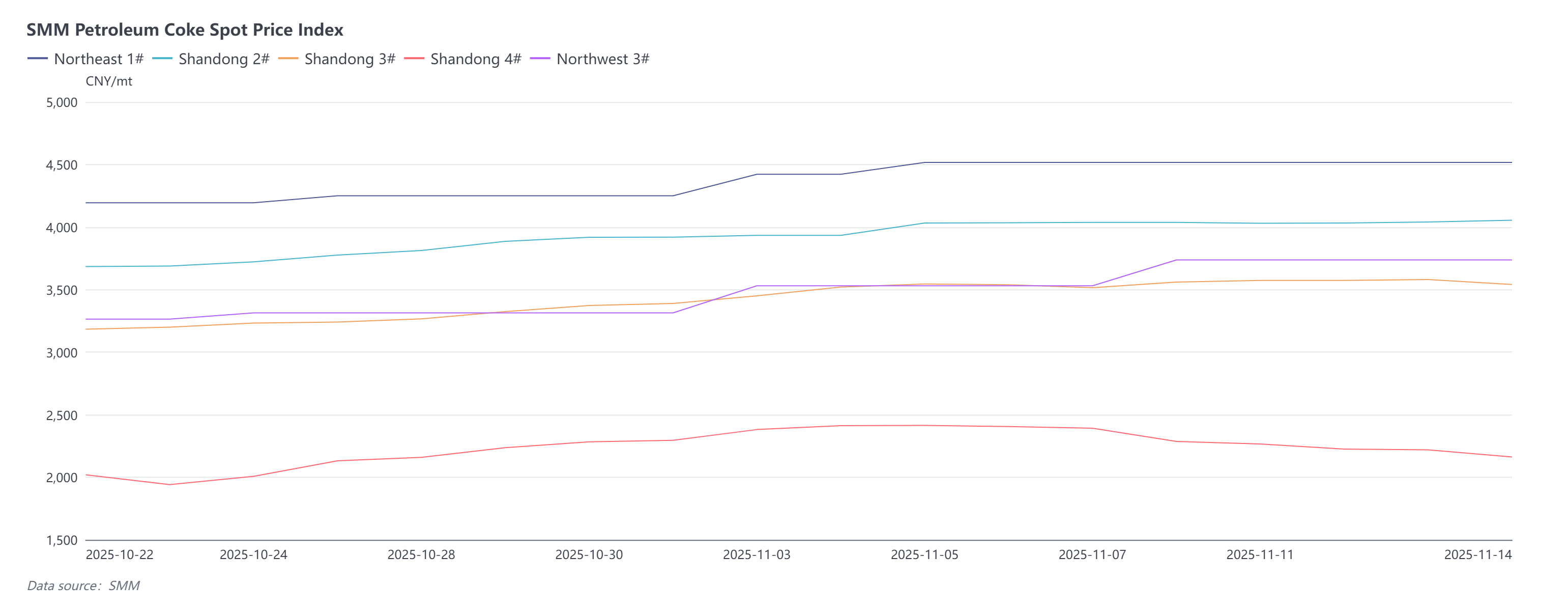

Petroleum coke market trading slowed down during the week, with refinery petroleum coke prices showing slight divergence. Mainstream refineries continued to raise petroleum coke prices, while local refineries faced weaker sales, with some prices starting to decline. Specifically, CNOOC refineries saw petroleum coke prices show mixed performance, though adjustments were limited, ranging between 20-50 yuan/mt. Taizhou Petrochemical and Binzhou Petrochemical increased prices by 20 yuan/mt, while Zhoushan Petrochemical decreased by 50 yuan/mt, with current prices concentrated at 4,450-4,650 yuan/mt. PetroChina's low-sulphur petroleum coke prices in north-east China remained stable, with prices currently ranging from 4,246-4,711 yuan/mt. Medium-sulphur petroleum coke prices in north-west China rose again, with SMM's north-west China #3 petroleum coke spot price index recorded at 3,737.42 yuan/mt, up 5.85% WoW. Sinopec refineries maintained good petroleum coke sales, with prices continuing to rise, mainly by 50-130 yuan/mt. Local refineries saw diverging sales performance, with #2 and #3 petroleum coke prices holding firm, while high-sulphur petroleum coke prices declined. Latest SMM data show Shandong's #3 petroleum coke spot price index at 3,540.84 yuan/mt, up 0.71% WoW, and Shandong's #4 petroleum coke spot price index at 2,162.66 yuan/mt, down 9.59% WoW.

The imported petroleum coke market fluctuated in line with the softening of domestic mainstream prices. Prices showed significant structural divergence, with medium- and low-sulphur grades performing firmly. Brazilian, Argentine, and US medium-sulphur petroleum coke prices remained stable, while high-sulphur petroleum coke prices pulled back, with Saudi, Formosa Plastics, and Russian high-sulphur petroleum coke prices declining to varying degrees. Due to the rapid rise in imported coke prices earlier and mediocre domestic medium- and high-sulphur petroleum coke market conditions, overall trading activity for imported petroleum coke noticeably decreased this week.

Supply side, petroleum coke market supply showed a rebound trend this week. The core increase came from production resumptions at Luoyang Petrochemical and Shandong Huaxing Petrochemical, while other domestic mainstream refineries maintained a steady production pace. Demand side, the concentrated restocking cycle in downstream industries is nearing its end, and subsequent procurement is expected to revert to rigid demand-driven patterns, with market trading activity projected to pull back further.

From a comprehensive supply-demand fundamental perspective, the current petroleum coke market is in a situation of increasing supply and tightening demand, coupled with downstream enterprises adopting a more cautious purchasing approach. SMM expects the price divergence of petroleum coke to persist in the short term. Among them, mainstream refineries are likely to maintain stable quotations, while local refineries may exhibit a generally stable with slight fall trend.

![Geopolitical Disruptions and a Stronger Dollar Combined to Keep Aluminum Prices Volatile Under Pressure [SMM Aluminum Morning Meeting Summary]](https://imgqn.smm.cn/usercenter/TFHUe20251217171651.jpg)

![Futures Rebound Drove Quote Increases, While Weak Transactions Capped Gains [SMM Cast Aluminum Alloy Morning Comment]](https://imgqn.smm.cn/usercenter/fFkYh20251217171651.jpg)