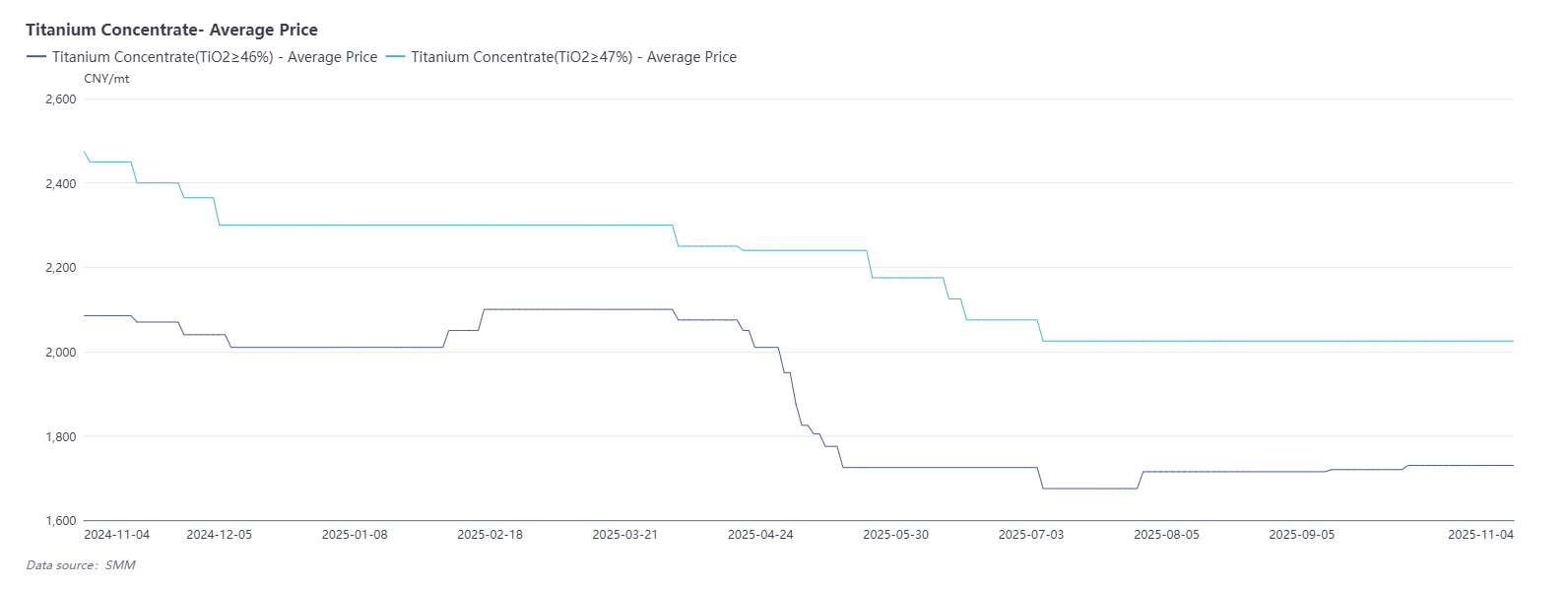

1. Titanium Concentrate

In October, the domestic titanium concentrate market generally showed a volatile yet relatively strong trend. Specifically, the quotation for TiO₂ ≥46% grade was in the range of 1,700-1,760 yuan/ton, with an average price of 1,730 yuan/ton; the quotation for TiO₂ ≥47% specification was in the range of 1,950-2,100 yuan/ton, with an average price of 2,025 yuan/ton. Overall prices saw a slight increase compared to September.

This round of price strength was mainly supported by two factors: On one hand, driven by the traditional "Golden September and Silver October" seasonal cycle, production demand in downstream industries such as titanium dioxide remained stable with an upward trend, leading to relatively strong procurement willingness for raw materials. On the other hand, domestic titanium ore supply remained relatively tight, with production limited in some main producing areas, further supporting firm price operations.

However, despite the steady performance in terms of prices, actual market shipment pressure gradually emerged. Affected by the continued weakness in the downstream market, trading activity for titanium concentrate was limited, and some actual transaction prices showed signs of softening. Against the backdrop of insufficient follow-up demand, market expectations for future price trends have weakened, and it is anticipated that titanium concentrate prices may face certain downward adjustment pressure.

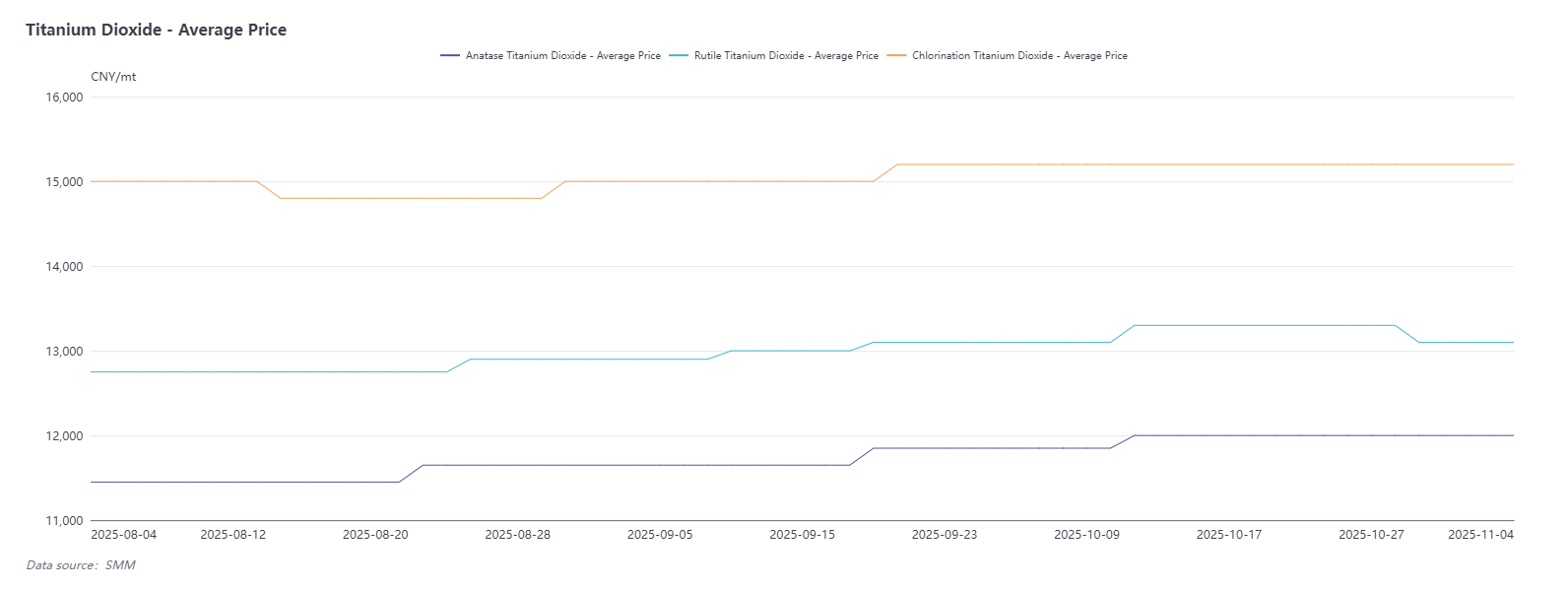

2. Titanium Dioxide

In October, the quotation for anatase titanium dioxide was 11,800-12,200 yuan/ton, with an average price of 12,000 yuan/ton; the quotation for rutile titanium dioxide was 12,700-13,500 yuan/ton, with an average price of 13,100 yuan/ton, and the FOB average price was $1,885/ton; the domestic quotation for chloride process titanium dioxide was 14,400-16,000 yuan/ton, with an average price of 15,200 yuan/ton, and the FOB average price was $2,100/ton.

Titanium dioxide prices showed a trend of rising initially then falling from high levels in October. At the beginning of the month, influenced by the concentrated release of September orders, some companies successively issued price adjustment letters to push prices higher. However, actual market transactions were still mainly focused on executing previous orders, with new orders being sporadic spot transactions. By mid-to-late October, domestic demand gradually weakened, market inquiries were light, and the signing prices of some companies fell back to the low range of September. The overall upward trend failed to continue effectively. Currently, both upstream and downstream players in the industrial chain have generally entered a wait-and-see mode, with trading activity significantly declining. Against the backdrop of limited external demand support and persistently weak domestic demand, market expectations are bearish, and it is anticipated that titanium dioxide quotations may face further downward adjustments in November.

According to SMM data, domestic titanium dioxide production in October was 326,000 tons, down 2.40% month-on-month; cumulative production from January to October 2025 decreased by 8.28% year-on-year. During the same period, producer inventories fell by 5.33% month-on-month.

The decline in production this month was mainly affected by the accident-related production halt of a leading enterprise in September. Although other regions saw slight production increases, the overall trend still showed a decline. In terms of inventory structure, small and medium-sized enterprises experienced some inventory drawdown, mainly concentrated in delivering September orders, while large enterprises still faced significant inventory pressure. In terms of external demand, overseas order volumes in October were relatively stable, but price pressure was widespread, keeping export prices under continuous pressure. Looking ahead to November, the titanium dioxide market will still rely on support from overseas orders. However, against the backdrop of high domestic inventories and no significant contraction in production, market expectations remain pessimistic. It is expected that by December, most companies may gradually shift towards production reduction.

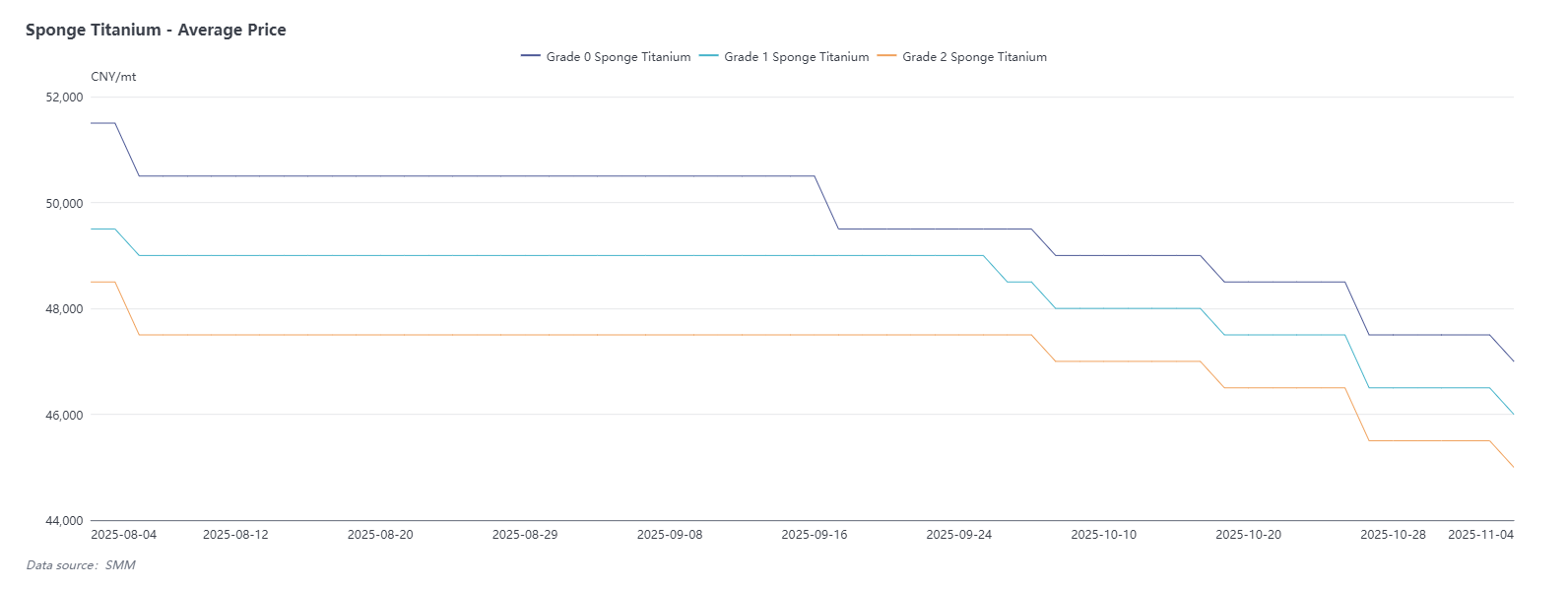

3. Sponge Titanium

In October, the sponge titanium market showed an overall downward price trend. Specifically, the mainstream quotation for Grade 0 sponge titanium was 46,500-48,500 yuan/ton, with an FOB quotation range of $6,600-6,650/ton; the quotation for Grade 1 sponge titanium was 45,500-47,500 yuan/ton; the quotation for Grade 2 sponge titanium was 44,500-46,500 yuan/ton. The full-month price cumulatively decreased by approximately 1,500 yuan/ton, continuing the downward trend.

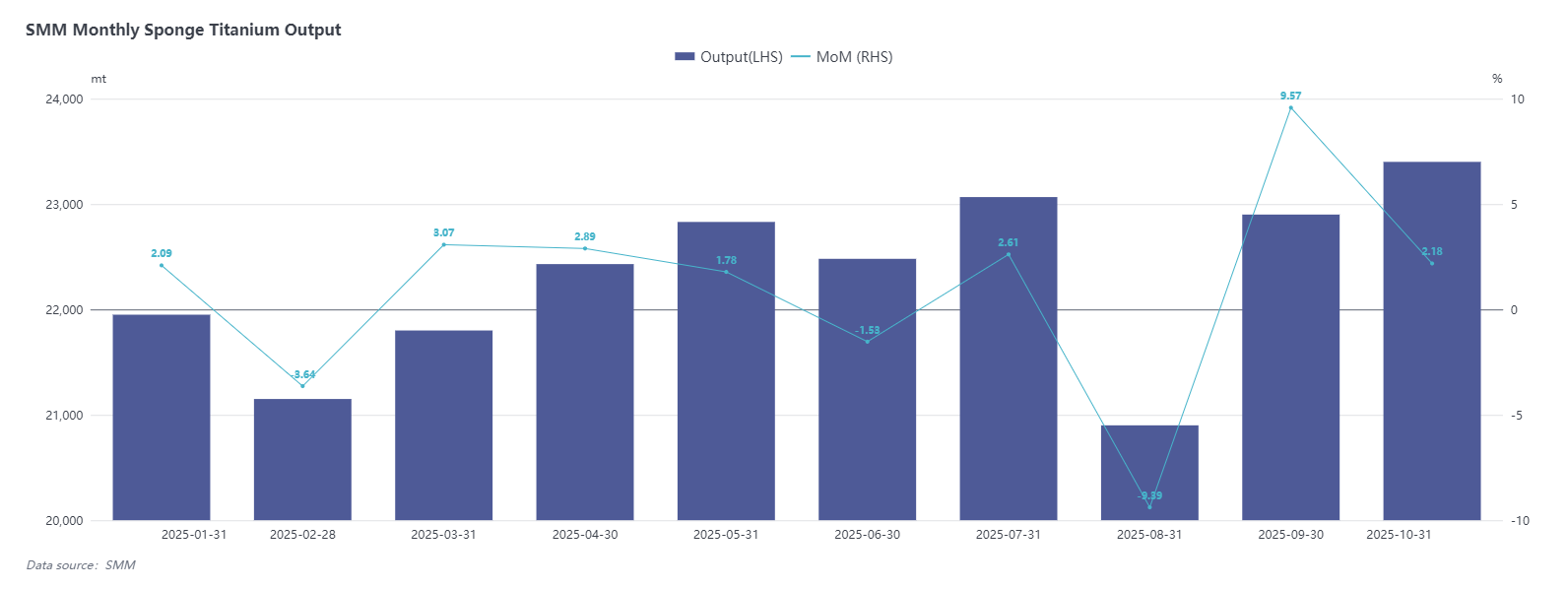

According to SMM statistics, China's sponge titanium production in October 2025 was approximately 23,400 tons, up 2.18% month-on-month, with cumulative production increasing by 3.03% year-on-year. Overall supply remained stable.

The slight rebound in production this month was mainly due to the fact that planned production cuts by some enterprises earlier did not materialize, and production gradually resumed. In terms of demand structure, the high-end sponge titanium market performed relatively steadily, but orders in the civil sector contracted. It is worth noting that some manufacturers adopted low-price sales strategies in late October, further driving down the overall market price level. In the long term, against the backdrop of continuous expansion of sponge titanium production capacity and insufficient follow-up of actual demand, prices still face certain downward pressure.

4. Market Summary

In October, the overall titanium market exhibited a pattern of weak supply and demand. Titanium concentrate prices were strong initially but weakened, showing softness in late October; titanium dioxide prices rose then fell, driven mainly by weak domestic demand; sponge titanium faced pressure across all grades, with a noticeable contraction in the civil sector. Looking ahead, the three major products are expected to remain under pressure: titanium concentrate faces downward adjustment pressure; titanium dioxide, hampered by weak domestic demand and high inventories, may see production cuts by year-end; sponge titanium, against the backdrop of overcapacity, is unlikely to reverse its downward trend. Overall, the supply-demand structure in the titanium market has not seen substantial improvement, and weak volatility is expected to continue in the short term.