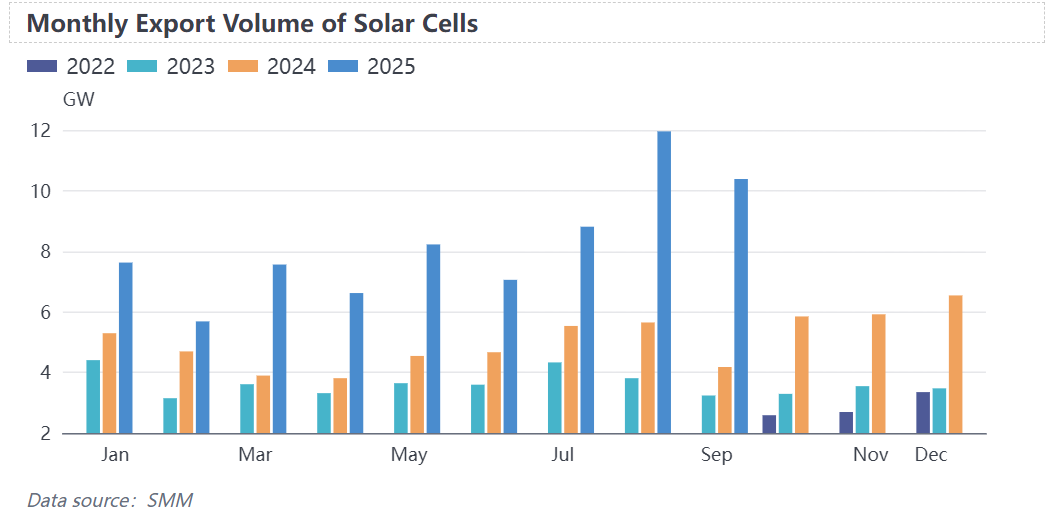

In September 2025, China's solar cell exports totalled 10.38GW, representing a 1.6% MoM decrease from August and a 6.2% YoY increase. Cumulative exports from January to September 2025 reached 73.91GW, marking a 74.9% rise compared to the same period last year.

One key driver behind the substantial export growth projected for 2025 is the phased demand for backlogs arising from the mismatch between overseas module and cell production capacity expansion rates. Compared to the module segment, cell production line expansion faces constraints including high equipment investment costs, stringent requirements for specialised production personnel, and significant negative externalities in manufacturing. Consequently, capacity release lags behind.

The export surge in the third quarter began to cool in September. On the one hand, major markets such as India and Turkey had already concentrated their procurement efforts in July and August, driven by policy expectations, thereby partially pre-empting subsequent purchasing demand. On the other hand, overseas inventories gradually rose following earlier concentrated arrivals, and some instances of over-purchasing further suppressed the release of new orders. Overseas demand is expected to decline further in the fourth quarter.

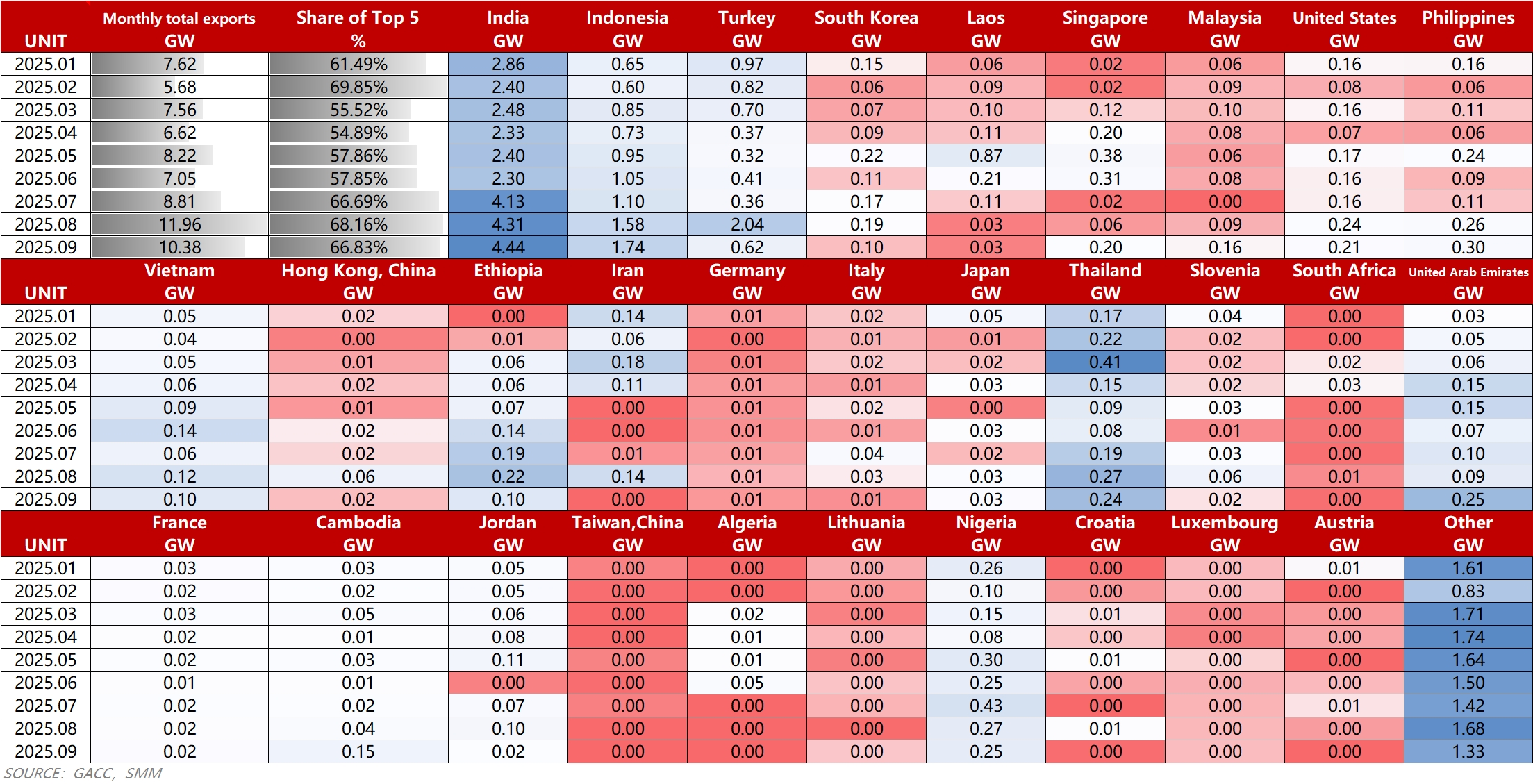

The concentration of the TOP 5 export destinations in September stood at 66.83%, down 1.33 percentage points from August. Major markets showed marked divergence under policy drivers, with emerging markets beginning to reveal their potential. September's TOP 5 destinations were India (4.44GW), Indonesia (1.74GW), Turkey (0.62GW), the Philippines (0.3GW) and the United Arab Emirates (0.25GW).

- China's exports to India increased by 3.0% MoM. Amid the ALMM Act and the announcement of India's AD/CVD investigations in mid-to-late September, local importers accelerated stockpiling during the window period.

- Indonesia: 10.1% MoM increase, with pronounced stockpiling demand observed locally ahead of the preliminary AD/CVD rulings against Indonesia and other nations by the United States.

- Turkey: 69.6% MoM decrease, as procurement demand returned to normal levels following the subsidence of August's stockpiling surge. Moreover, the policy of raising the minimum import price proved relatively limited in its short-term effectiveness to curb local cell imports.

- Philippines: 15.4% MoM increase. Against the backdrop of China's progressively tightening export policies, the Philippines' advantage in transshipment trade has been enhanced.

- United Arab Emirates: 177.8% MoM increase. Photovoltaic demand and production capacity in the Middle East are on a rapid upward trajectory, with local manufacturers increasing imports of solar cells to supplement domestic production capacity.