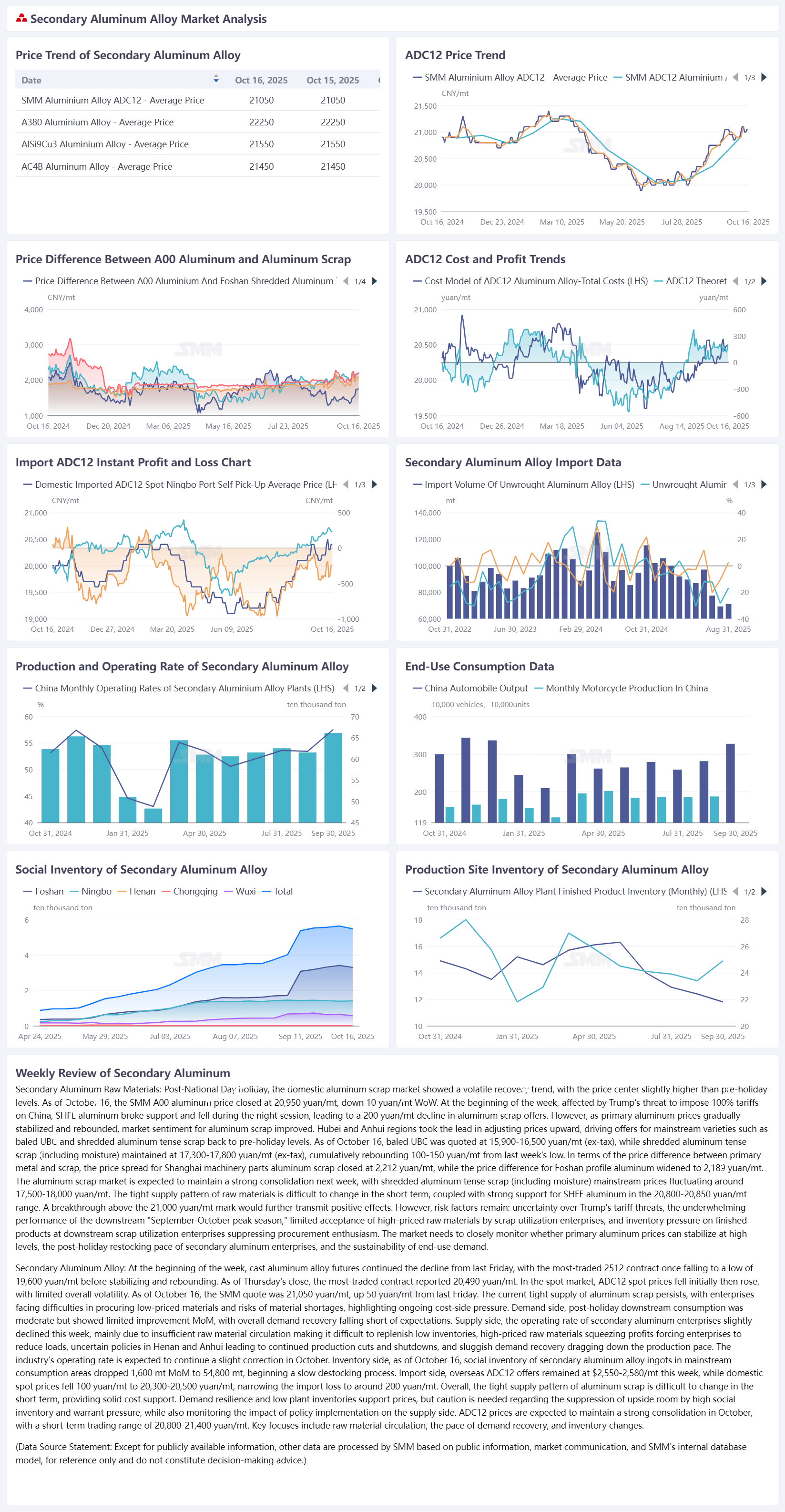

After the National Day holiday, the domestic aluminum scrap market showed a volatile and corrective trend, with the price center slightly higher than pre-holiday levels. As of October 16, the SMM A00 aluminum price closed at 20,950 yuan/mt, down 10 yuan/mt WoW. At the beginning of the week, affected by Trump's threat to impose 100% tariffs on China, SHFE aluminum broke support and fell during the night session, and aluminum scrap offers followed with a decrease of 200 yuan/mt. However, as primary aluminum prices gradually stabilized and rebounded, market sentiment for aluminum scrap improved. Hubei and Anhui took the lead in adjusting prices upward, driving offers for mainstream varieties such as baled UBC and shredded aluminum tense scrap back to pre-holiday levels. As of October 16, baled UBC offers were concentrated at 15,900–16,500 yuan/mt (ex-tax), while shredded aluminum tense scrap (water price) held at 17,300–17,800 yuan/mt (ex-tax), up 100–150 yuan/mt from last week's low. In terms of the price difference between primary metal and scrap, the price difference between A00 aluminum and shredded aluminum tense scrap in Shanghai closed at 2,212 yuan/mt, while the price difference for aluminum profiles in Foshan widened to 2,189 yuan/mt. The aluminum scrap market is expected to hold up well next week, with mainstream prices for shredded aluminum tense scrap (water price) fluctuating around 17,500–18,000 yuan/mt. The tight supply of raw materials is unlikely to ease in the short term, and coupled with strong support for SHFE aluminum in the 20,800–20,850 yuan/mt range, a breakthrough above the 21,000 yuan/mt mark would further transmit positive effects. However, risks remain: uncertainty over Trump's tariff threats, the underwhelming performance of the September-October peak season for downstream demand, and limited acceptance of high-priced raw materials by scrap utilization enterprises. Downstream scrap utilization enterprises face inventory pressure on finished products, which will curb purchasing enthusiasm. The market needs to closely monitor whether primary aluminum prices can sustain high levels, the restocking pace of secondary aluminum enterprises after the holiday, and the sustainability of end-use demand.

At the beginning of the week, cast aluminum alloy futures continued the decline from last Friday, with the most-traded ag2512 contract once falling to a low of 19,600 yuan/mt before stabilizing and rebounding. As of Thursday's close, the most-traded contract was quoted at 20,490 yuan/mt. In the spot market, ADC12 spot prices fell first and then rose, with limited overall volatility. As of October 16, the SMM price was 21,050 yuan/mt, up 50 yuan/mt from last Friday. The current tight supply of aluminum scrap persists, making it difficult for enterprises to procure low-priced materials and exposing them to material shortage risks, with cost-side pressure continuing to intensify. Demand side, post-holiday downstream consumption was moderate but showed limited improvement MoM, with overall demand recovery falling short of expectations. Supply side, the operating rate of secondary aluminum enterprises declined slightly this week, mainly due to insufficient raw material circulation making it difficult to replenish low inventories, high-priced raw materials squeezing profits and forcing load reductions, uncertain policies in Henan and Anhui leading to continued production cuts and shutdowns, and sluggish demand recovery dragging down the production pace. The industry's operating rate is expected to continue its slight correction in October. Inventory side, social inventory of secondary aluminum alloy ingots in mainstream consumption areas fell by 1,600 mt WoW to 54,800 mt on October 16, beginning a slow destocking process. Import side, overseas ADC12 offers held at $2,550–2,580/mt this week, while domestic spot prices fell by 100 yuan/mt to 20,300–20,500 yuan/mt, narrowing the import loss to around 200 yuan/mt. Overall, the tight supply of aluminum scrap is unlikely to change in the short term, providing solid cost support, while demand resilience and low plant inventories support prices. However, caution is needed regarding the suppression of upside room by high social inventories and warrant pressure, along with the impact of policy implementation on the supply side. ADC12 prices are expected to hold up well in October, with a short-term trading range of 20,800–21,400 yuan/mt. Key focuses include raw material circulation, the pace of demand recovery, and inventory changes.