SMM October 10 News:

Holiday Trend Review:

During the National Day holiday, SHFE zinc trading was suspended for the holiday, while LME zinc continued to rise to a yearly high. Specifically, after opening, LME zinc quickly climbed above $3,000/mt and then held up well with fluctuations, hitting a new yearly high of $3,048/mt during the period. As of Tuesday's close, LME zinc settled at $3,041.5/mt, with trading volume increasing to 13,813 lots and open interest rising to 223,000 lots compared to pre-holiday levels. As of Tuesday, LME zinc inventory decreased to 38,200 mt, down 2,750 mt from before the holiday, with the reduction mainly coming from Singapore warehouses.

Overall, the market experienced continuous macro events during the holiday. Domestically, the National Development and Reform Commission (NDRC) officially issued the fourth batch of ultra-long-term special treasury bonds for the year, totaling 69 billion yuan, to support consumer goods trade-in policies, while the central bank conducted 1,100 billion yuan in outright reverse repo operations on October 9. Overseas, the US August job openings data before the holiday fell short of expectations, coupled with escalating government shutdown risks, leading to a continuous decline in the US dollar index and a rise in LME zinc. During the holiday, the US September ADP employment data showed weakness, recording the largest drop since 2023, and the US Senate again rejected the temporary funding bill. Affected by funding issues, the US government entered a shutdown state for the first time in seven years. Driven by traders' risk aversion sentiment, LME zinc continued to rise. Subsequently, the US nonfarm payroll report was absent for the first time in 12 years, and the government remained shut down, intensifying current and future uncertainties, with LME zinc maintaining a fluctuating trend.

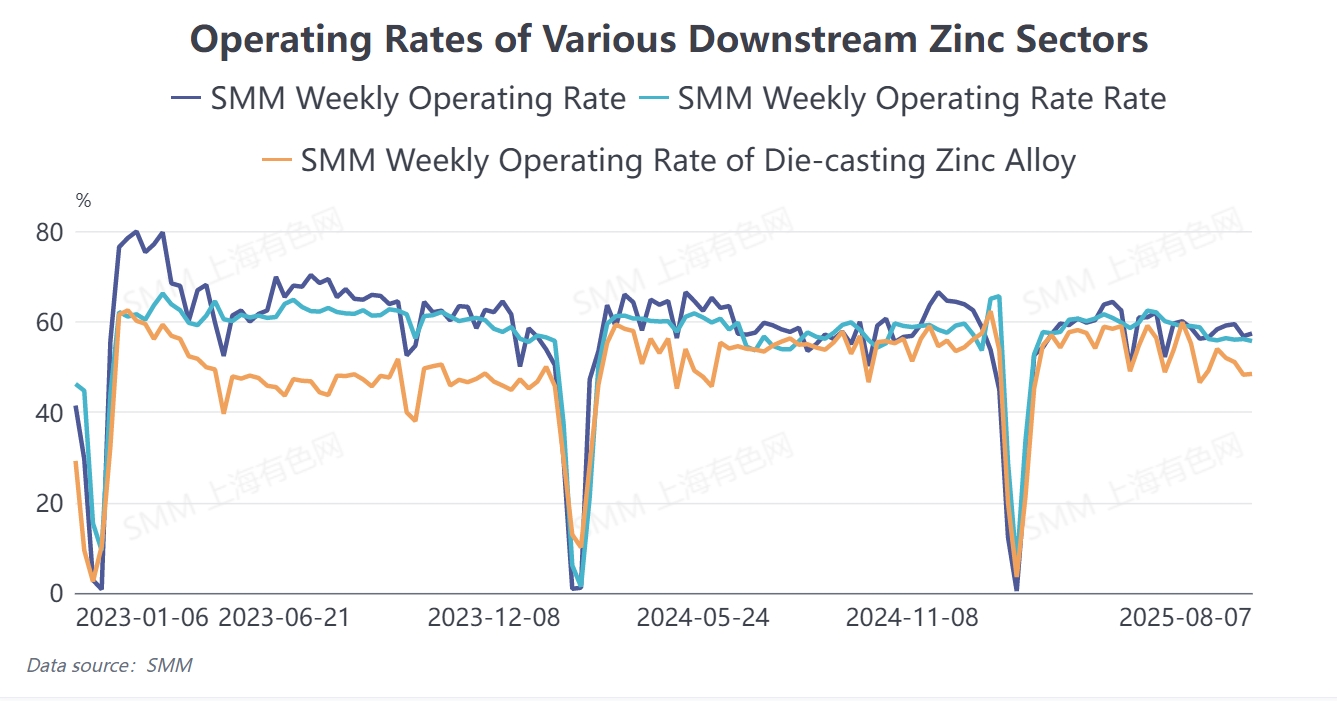

Post-Holiday Price Outlook: Supply side, with the continuous production resumptions at some domestic smelters, SMM expects domestic refined zinc production to reach 622,700 mt in October, up 22,600 mt MoM, indicating a relatively loose supply situation. Demand side, galvanizing consumption showed some marginal improvement in September compared to August. Although end-use consumption of die-casting zinc alloy also recovered, enterprises were heavily impacted by low-priced alloys in the market. Zinc oxide, driven by demand recovery in certain sectors, also saw an overall improvement in operating rates.

Overall, the domestic market remains in a state of oversupply. However, TCs on the supply side have peaked and started to decline, while sulfuric acid prices in most regions have begun to pull back, compressing smelter margins to some extent. Coupled with rising prices of recycled raw materials, further increases in refined zinc production are expected to face certain constraints. On the demand side, consumption may still hold some potential, supported by the fourth round of trade-in subsidies. Moving forward, it will be important to monitor actual domestic consumption trends and changes in macro policies.