ข่าว SMM วันที่ 30 กันยายน:

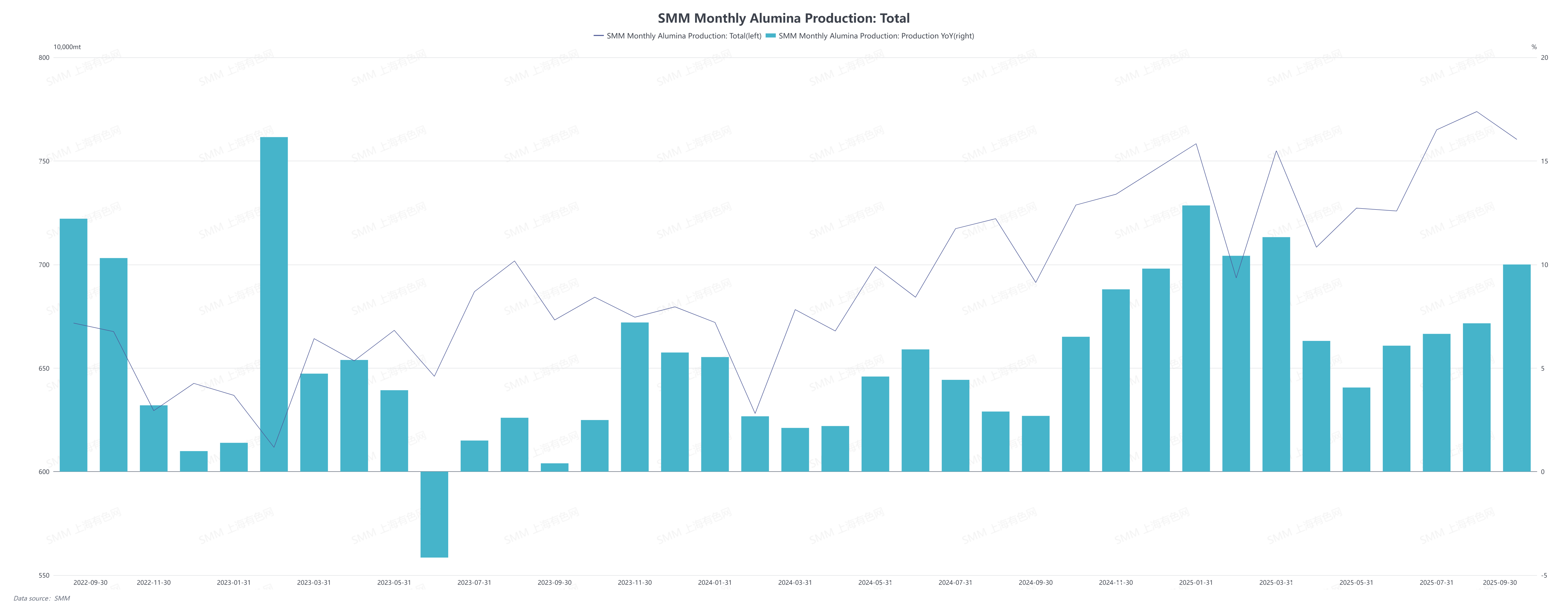

ตามข้อมูลของ SMM การผลิตอลูมินาเกรดเมทัลลูร์จีของจีนในเดือนกันยายน ปี 2025 (30 วัน) เพิ่มขึ้น 1.52% เมื่อเทียบรายเดือน และเพิ่มขึ้น 10.00% เมื่อเทียบรายปี ณ สิ้นเดือนกันยายน กำลังการผลิตอลูมินาเกรดเมทัลลูร์จีของจีนอยู่ที่ประมาณ 110.32 ล้านตัน กำลังการผลิตที่ดำเนินการจริงเพิ่มขึ้น 1.54% เมื่อเทียบรายเดือน และมีอัตราการดำเนินการ 80.23%

ปริมาณการผลิตอลูมินาระหว่างวันเฉลี่ยในเดือนนี้เพิ่มขึ้นเล็กน้อย แต่อัตราการเติบโตถูกจำกัดเนื่องจากปัจจัยต่อไปนี้: ต้นเดือน เนื่องจากการจัด "พิธีสวนสนามวันที่ 3 กันยายน" โรงงานบางแห่งทางตอนเหนือลดภาระเตาเผาชั่วคราวในช่วงการจัดงาน นอกจากนี้ บริษัทบางแห่งทางตอนใต้ได้ดำเนินการซ่อมบำรุงตามแผน ทำให้ลดภาระเตาเผาลงเช่นกัน นอกจากนี้ ราคาอลูมินาที่ลดลงทำให้กำไรของบริษัทลดลง ทำให้ความกระตือรือร้นในการเพิ่มการผลิตลดลง ในช่วงกลางถึงปลายเดือนกันยายน เมื่อข้อจำกัดจากการจัดงานและซ่อมบำรุงสิ้นสุดลง อัตราการดำเนินการของบริษัทค่อยๆ ฟื้นตัว ทำให้การผลิตเพิ่มขึ้นเล็กน้อยตลอดเดือน แม้ว่าราคาตลาดจะลดลงในเดือนกันยายน ทำให้กำไรลดลง แต่การคำนวณจากราคาเฉลี่ยรายเดือนยังแสดงให้เห็นว่ายังคงมีกำไรอยู่ ดังนั้น บริษัทอลูมินาไม่มีแผนลดการผลิตหรือซ่อมบำรุงในเดือนกันยายน และอัตราการดำเนินการโดยรวมยังคงอยู่ในระดับที่สูง

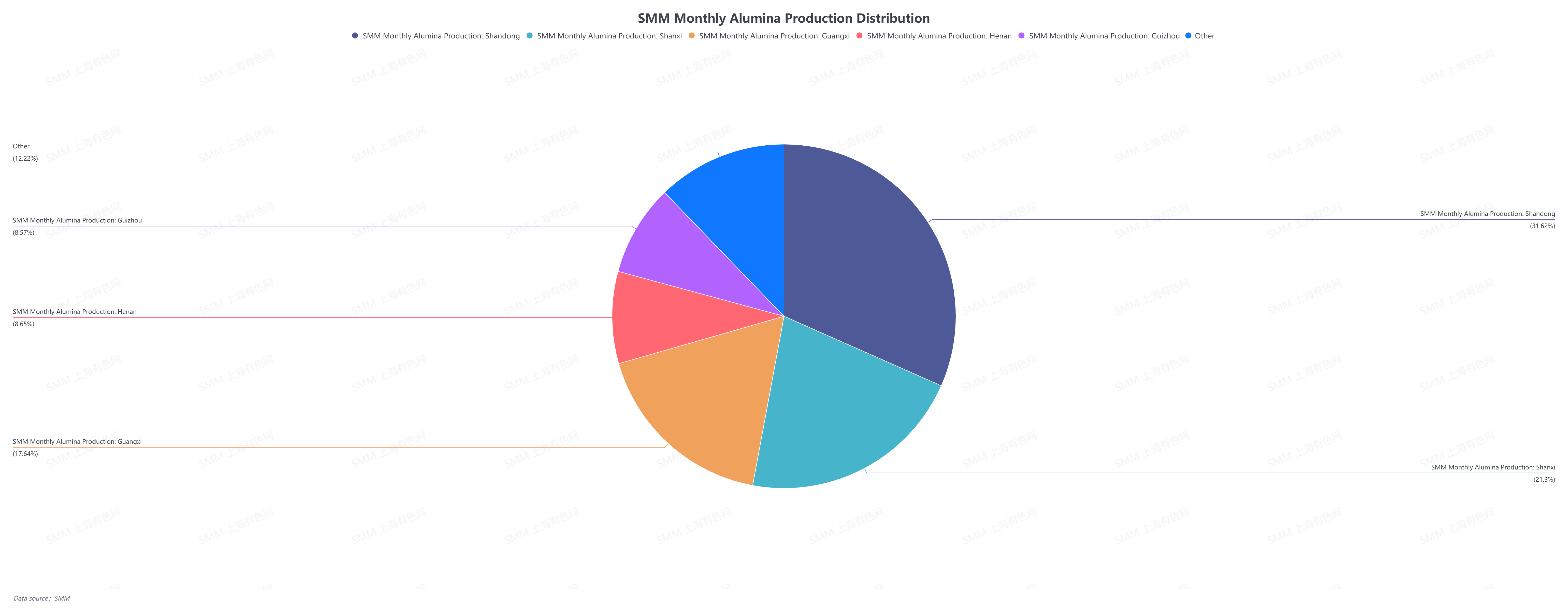

จากมุมมองทางภูมิภาค:

ในเดือนกันยายน ความแตกต่างของราคาระหว่างตลาดอลูมินาทางตอนเหนือและตอนใต้ของประเทศมีความชัดเจน ต้นเดือน การซ่อมบำรุงตามแผนของบริษัททางตอนใต้ทำให้การจัดจำหน่ายขาดแคลนเล็กน้อย สนับสนุนราคาและทำให้ราคาแข็งแกร่ง จนถึงกลางถึงปลายเดือนกันยายน เมื่อการจัดจำหน่ายฟื้นตัว พร้อมด้วยการนำเข้าอลูมินาและการ "ขนส่งสินค้าจากเหนือมาใต้" ความต้องการสนับสนุนราคาของผู้ถือสินค้าทางตอนใต้ลดลงเล็กน้อย ภายใต้ผลกระทบจากแหล่งราคาต่ำทางตอนเหนือและการนำเข้า ราคาตลาดของอลูมินาทางตอนใต้ลดลง อย่างไรก็ตาม กำลังการผลิตอลูมินาทางตอนใต้ยังคงมีกำไรมากพอสมควร และยังไม่มีรายงานการลดการผลิต

ในทางกลับกัน ราคาเสนอขายในตลาดทางตอนเหนือยังคงอยู่ภายใต้แรงกดดันตลอดเดือน รักษาแนวโน้มขาลง ขณะเข้าสู่เดือนตุลาคม คาดว่าราคาเฉลี่ยรายเดือนจะต่ำกว่าต้นทุนเงินสดของบริษัทที่มีต้นทุนสูง และบางบริษัทอาจขาดทุนและลดการผลิต

แนวโน้มสำหรับเดือนหน้า:

ตลาดอลูมินาคาดว่าจะยังคงอยู่ในรูปแบบเกินดุลในเดือนตุลาคม เมื่อเข้าสู่เดือนตุลาคม ราคาเฉลี่ยรายเดือนคาดว่าจะเผชิญกับแรงกดดันด้านขาลงและค่อยๆ เข้าใกล้เส้นต้นทุน บริษัทที่มีต้นทุนสูงบางแห่งมีแนวโน้มที่จะเผชิญกับความสูญเสียและอาจใช้มาตรการลดการผลิตและการบำรุงรักษาอย่าง proactive เมื่อด้านอุปทานหดตัว สถานการณ์เกินดุลในปัจจุบันคาดว่าจะคลี่คลายลงในระดับหนึ่ง อย่างไรก็ตาม เนื่องจากการปรับด้านอุปสงค์และอุปทานต้องใช้เวลา ราคามีแนวโน้มที่จะยังคงอ่อนแอและผันผวน ความสามารถในการดำเนินการของอลูมินาในเดือนตุลาคมคาดว่าจะลดลง โดยคาดว่าว่าความสามารถในการดำเนินการของอุตสาหกรรมจะอยู่ที่ประมาณ 88.98 ล้านตัน