The National Day holiday is approaching in 2025. SMM surveyed some copper processing enterprises regarding their production arrangements during the holiday. A total of 100 downstream copper processing enterprises were surveyed, involving a total annual capacity of 16.5398 million mt. Affected by the sharp rise in copper prices before the holiday, most copper processing enterprises indicated that the holiday duration is expected to be longer YoY. The detailed survey summary is as follows:

Copper cathode rod: Domestic copper cathode rod enterprises averaged 4.05 days off for the holiday, slightly more than last year's 3.95 days. Soaring copper prices, which surged to a high of 83,000 yuan/mt, suppressed downstream wire and cable enterprises' stockpiling sentiment. Pre-holiday procurement volume fell short of last year's level, and new orders for enterprises remained low. Although some wire and cable enterprises plan to launch sales promotions in October to boost demand, against the backdrop of high copper prices and policy support weaker than the same period last year, the operating rate of the copper cathode rod industry is expected to decline slightly MoM and be lower than the level recorded a year earlier.

Secondary copper rod: Secondary copper rod enterprises averaged 2.32 days off for the holiday, down 0.31 days YoY. Except for some areas in Anhui and Jiangxi where production remained halted due to policy impacts, secondary copper rod enterprises in other regions generally planned to maintain normal production, arranging only shift rotations for workers or brief holidays of 1–2 days. However, due to the rapid rise in copper prices this week, downstream customers urged secondary copper rod enterprises to expedite deliveries. With finished product inventories at low levels, enterprises are actively stockpiling recycled copper raw materials to ensure production during the holiday. The market generally holds a bullish outlook on future copper prices. The price difference between copper cathode rod and secondary copper rod is expected to continue widening, continuously stimulating end-use consumption and driving an increase in the operating rate of secondary copper rod enterprises.

Copper Pipe & Tube: Most copper pipe and tube enterprises increased their holiday duration by 1-3 days compared to last year, with only a few enterprises possibly shortening the holiday depending on order conditions. Pre-holiday copper prices surpassed the high of 83,000 yuan/mt, suppressing enterprises' stockpiling willingness. Large enterprises maintained inventory through long-term contracts and imported sources, while small and medium-sized enterprises mostly adopted a wait-and-see attitude, planning to make just-in-time procurement based on orders. Affected by factors such as overdrawn air conditioner production and sales in H1, YoY decline in H2 production schedules, and US tariff hikes impacting exports, the industry generally holds a pessimistic outlook for Q4 operations, expecting the copper pipe market to experience the most sluggish "October peak season" in recent years.

Copper Plate/Sheet and Strip: Copper plate/sheet and strip enterprises' holiday arrangements were largely consistent with last year, maintaining a steady production pace overall. Most large enterprises continued uninterrupted production, while a few small enterprises took 5-7 days off due to order or raw material issues. Currently, most enterprises have completed pre-holiday raw material stockpiling, preparing for seamless production during and after the holiday. As the traditional off-season ends in October, downstream demand is expected to recover, and enterprises are optimistic about order growth. However, the current high copper prices significantly dampen downstream purchase willingness, and under cost pressure, end-users are cautious in stockpiling. Therefore, copper plate/sheet and strip enterprises maintain a "cautiously optimistic" expectation regarding the actual release of post-holiday demand.

Brass Billet: Brass billet production workers generally took 3-5 days off, with an average increase of 1.15 days in holiday length compared to last year. Influenced by copper prices surpassing 83,000 yuan/mt and tight supply of recycled brass raw materials, downstream stocking enthusiasm was suppressed, resulting in a less vibrant "September-October peak season," with pre-holiday stockpiling volumes noticeably lower than the same period last year. Enterprises anticipate a MoM recovery in October orders but, given the sustained high fluctuation of copper prices, they hold a cautiously optimistic view of the future market.

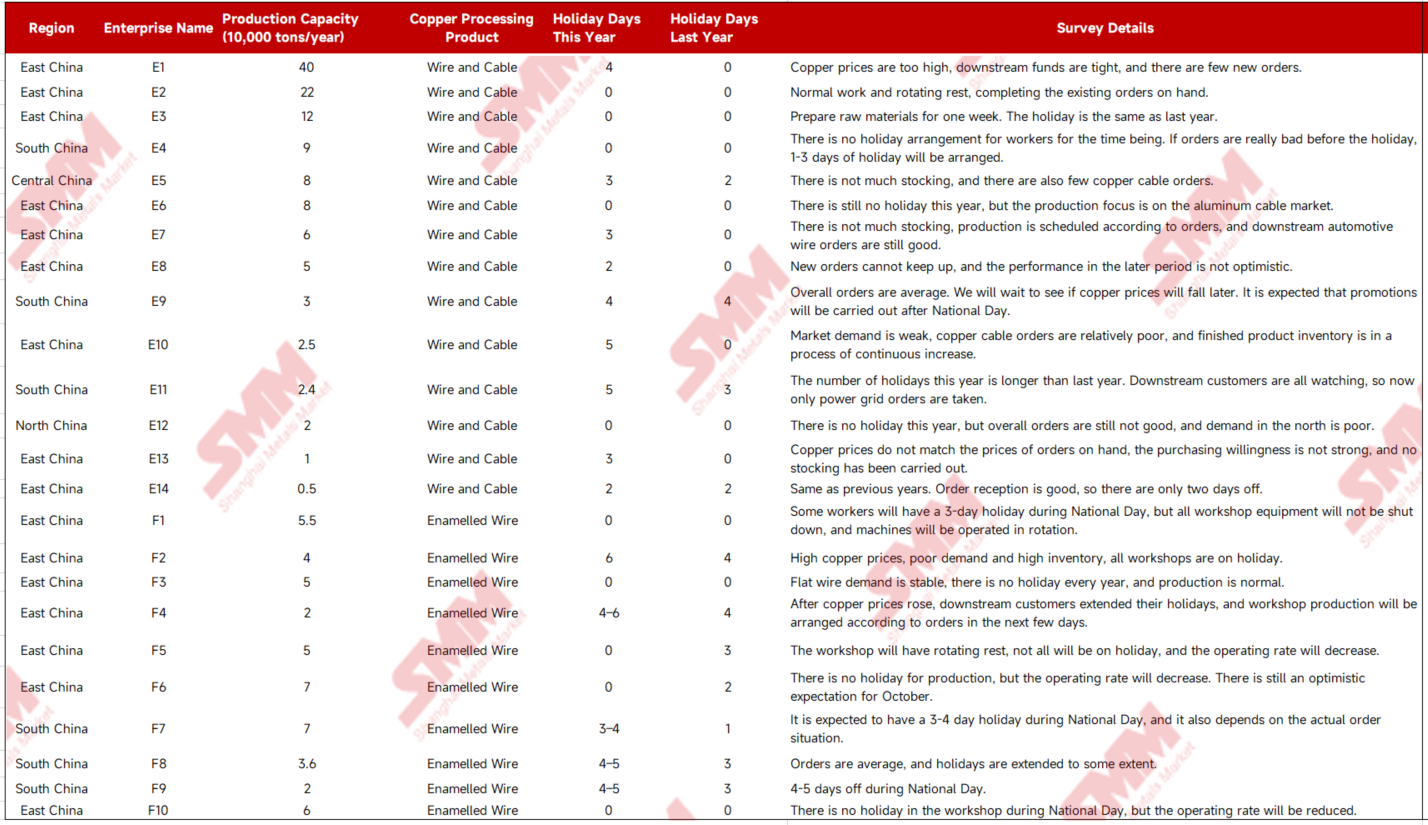

Wire and Cable: Wire and cable enterprises averaged 2.21 days off for the holiday, up 1.43 days YoY, with the overall number of work stoppages increasing year-on-year. High copper prices suppressing procurement, weak downstream demand, and funding pressures led to lower pre-holiday stockpiling volumes compared to last year, characterized by rising finished product inventories and declining raw material inventories. Some companies shifted to aluminum wire and cable production in response to changes in order structure. Although the industry still expects State Grid and China Southern Power Grid projects to provide demand support in October, market sentiment has turned cautious amid high copper prices, with most enterprises planning to boost operating rates through sales promotions after copper prices retreat.

Enamelled Wire: As copper prices broke through the high of 83,000 yuan/mt, downstream purchase willingness was suppressed, and enterprise orders were generally insufficient. Most companies arranged 3–5 days off, with some extending to 6 days; although some top-tier enterprises did not close, they reduced operating rates. Overall holiday duration in the industry increased significantly compared to previous years. Enterprises maintained cautious expectations for October demand; under dual pressures of high copper prices and slow recovery in home appliance and other end-use demand, post-holiday operating rates are expected to be difficult to surpass last year’s level.

During the 2025 National Day holiday, the average days off for copper processing enterprises (same sample as last year) increased by 3.77 days YoY, with particularly notable extensions for copper pipe & tube, wire and cable, and copper billet producers. Affected by the sharp pre-holiday rise in copper prices, downstream stocking willingness was generally suppressed, and enterprises mainly conducted just-in-time procurement, keeping overall inventory at relatively low levels. Although some companies still anticipate a recovery in October demand, constrained by multiple factors including high copper prices and slow end-use demand recovery, the industry generally holds a “cautiously optimistic” view of the post-holiday market, with overall operating rates expected to be difficult to exceed the same period last year.