The US Fed cut interest rates overnight as expected, by 25 basis points to a range of 4.00%-4.25%, the lowest level in nearly three years, breaking a nine-month streak of unchanged decisions. According to media reports, "Officials judged that the recent weakness in the labour market has outweighed the resistance from recurring inflation. Slightly more than half of the officials expect at least two more rate cuts this year, implying possible consecutive actions at the remaining two meetings in October and December."

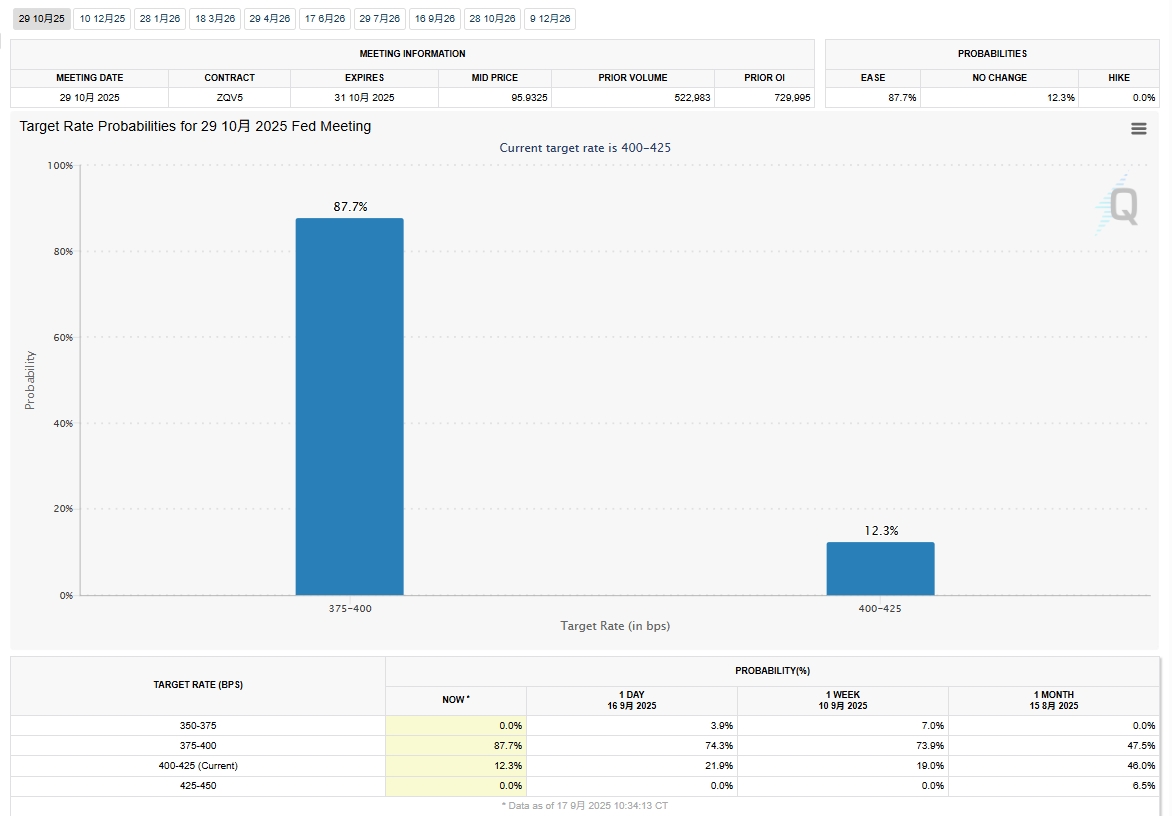

According to the latest data from FedWatch, the probability of the US Fed cutting rates by another 25 basis points in October is 87.7%, significantly higher than before; the probability of no change is only 12.3%.

Data source: FedWatch Tool

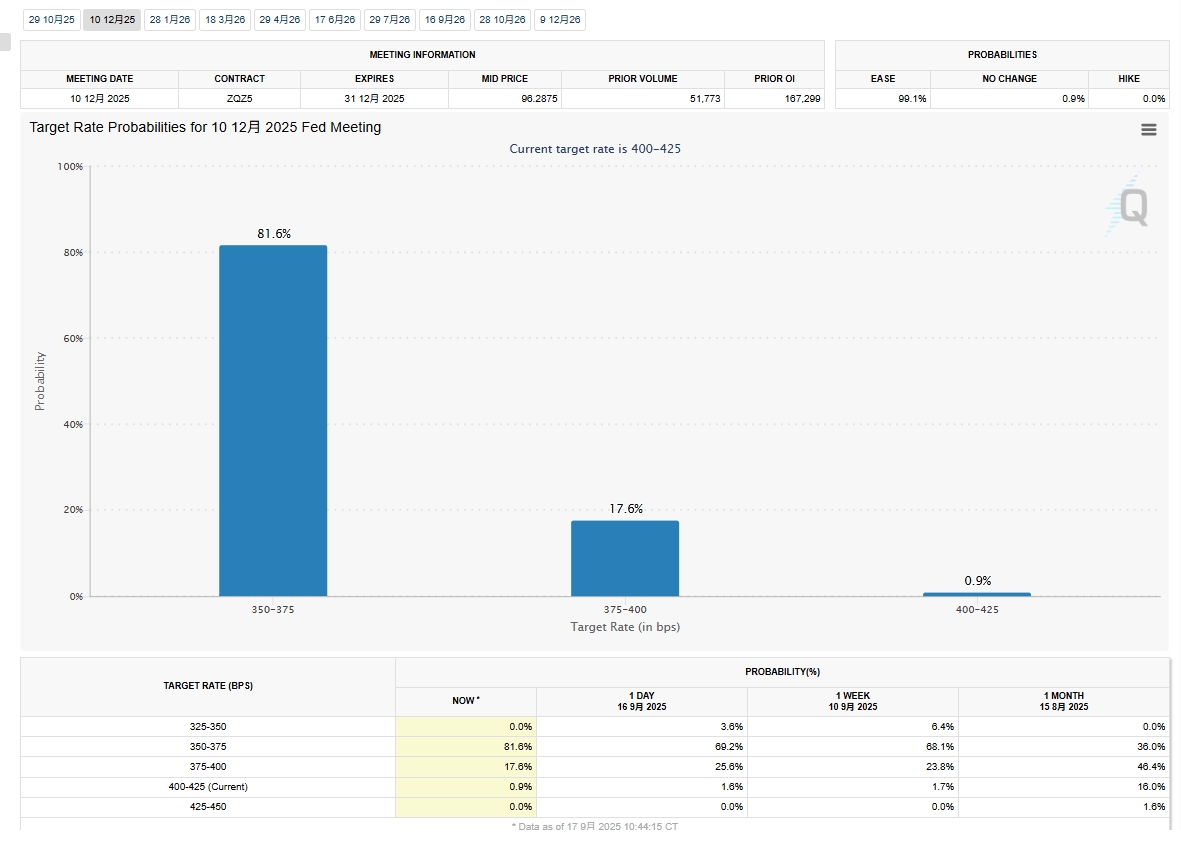

The probability of the US Fed cutting rates by another 25 basis points in December to 3.50%-3.75% on top of November's move has risen to 81.6%, while the probability of maintaining the October cut of 25 basis points to 3.75-4.00% is 17.6%; 0.9% still believe there will be no rate cuts in October or December, meaning rates would remain at 4.00%-4.25%.

Data source: FedWatch Tool

With the September rate cut implemented, the macro tailwinds have temporarily "come to an end." Yesterday afternoon, LME copper led the trading session, with bulls exiting positions. It closed with a long bearish candlestick accompanied by a long lower shadow, hitting a low of $9,927/mt. Overnight, SHFE copper opened lower with a gap, falling below the 80,000 yuan/mt level and probing a low of 79,690 yuan/mt, attracting substantial downstream point pricing of previous orders. The futures then gradually rebounded to fluctuate rangebound between 79,800-79,960 yuan/mt.

Observing the market's reaction to this round of copper price decline from a micro fundamental perspective:

In the morning session, the SHFE copper 2510 contract continued to rise from a low of 79,740 yuan/mt. During the concentrated trading period for spot transactions, the futures briefly touched the 80,000 yuan/mt level again but "faded quickly," indicating a lack of market confidence in copper prices above 80,000 yuan/mt. In the afternoon session, as LME copper declined, SHFE copper opened with a downward trend. Trading activity below 79,800 yuan/mt increased, with the front-month contract reducing positions by over 17,000 lots.

Trading activity significantly increased in the morning session. Most smelting and trading enterprises achieved actual shipments of 500-3,000 mt each between 9:30-11:30. Downstream users shifted from only picking up long-term contracts and just-in-time procurement to increasing spot orders and advance stockpiling.

Based on SMM's exchanges with enterprises:

Smelter 1: Shipments increased MoM from yesterday, with the premium center rising by 20 yuan/mt. Downstream point pricing was relatively active.

Smelter 2: Shipments increased MoM from yesterday, with the premium center rising by 10-20 yuan/mt. Inventories in the Changzhou area were depleted within the day.

Trader 1: Shipments increased MoM from yesterday, and point pricing was active during the overnight night session, but 80% were previously tentative orders. The selling price center rose during the day, with non-registered purchases being the most active.

Trader 2: Shipments increased MoM from yesterday, with low-priced sources being snapped up. Some downstream users inquired about future arrivals, likely preparing for National Day holiday procurement.

Downstream 1: Only picked up long-term contracts yesterday but made spot purchases today. There were new orders, but growth was mild rather than explosive. The procurement price was 10 yuan/mt higher than the spot offers heard yesterday.

Downstream 2: Procurement orders today were 1,000 mt more than yesterday. Stockpiling for the National Day holiday began gradually from yesterday, but order growth remained mild. Non-registered prices were 30 yuan/mt higher than yesterday's procurement price.

Summary:

The September rate cut did not exhaust the bullish factors. The market sensed weak demand at high copper prices and grew concerned about the upside room for copper prices. However, as copper prices fell by just 1,000 yuan/mt, market demand gradually released, with support emerging at 79,500 yuan/mt. If precious metals continue to retreat, copper prices are expected to fall to the 79,000-79,500 yuan/mt range. With only eight trading days left before the National Day holiday, demand is expected to improve.

Supply side: Domestic copper cathode supply remains tight amid concentrated maintenance at domestic smelters in September and October and unclear policies on copper scrap. Import supplements are expected to increase, but production cuts of copper cathode in Africa may impact October supply.

Demand side: Although large-scale downstream stockpiling for the National Day holiday was not widely felt this week, large enterprises are expected to gradually increase daily procurement volume next week. If copper prices reach 79,000 yuan/mt, consumption sentiment is expected to improve further next week, and destocking will accelerate.

Due to high copper prices and continuous import arrivals, copper inventories were still in a buildup two to three weeks before the National Day holiday in 2025. Against the backdrop of this round of copper price decline and reduced import supplements WoW, destocking is expected to appear on September 25. Fundamental support for copper prices remains. After the brief retreat of macro tailwinds, the market is expected to resume trading expectations for an October rate cut. Key focuses include signs of stabilization in precious metals and fundamental consumption sentiment for copper. Copper prices are expected to pause their decline near 79,000 yuan/mt and gradually recover to fill the gap.