SMM September 15 News:

I. Core Market Contradiction: Rigid Cost Increases and Slower-Than-Expected Consumption Recovery

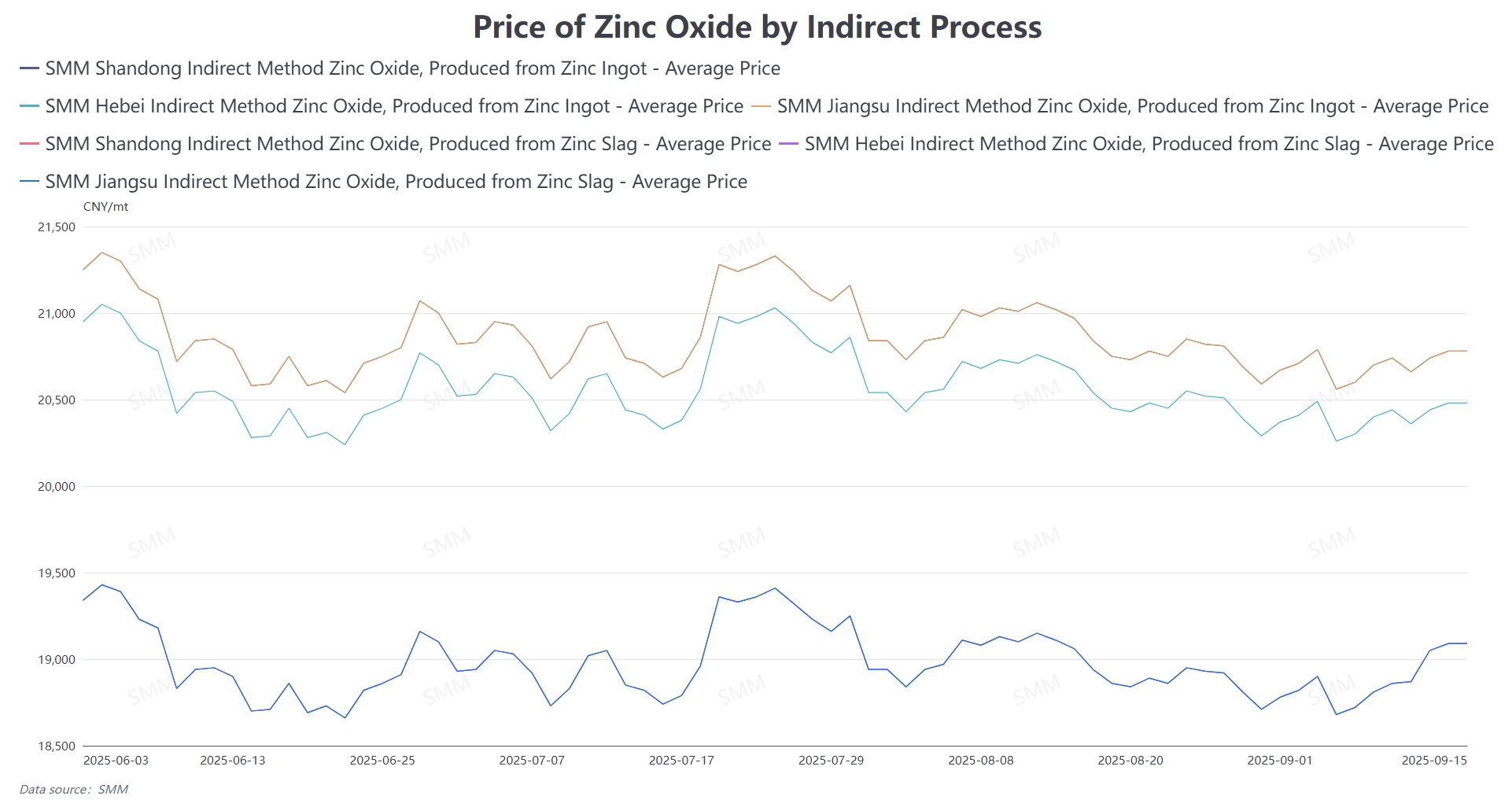

In early September, the combination of the SCO Summit and the September 3 military parade led to significantly enhanced environmental protection-related controls in North China. As the galvanizing industry is the main source of zinc slag—a key raw material for indirect-process zinc oxide production—it faced certain restrictions. According to SMM, most galvanizing plants in North China adopted measures such as reduced operating rates or short-term shutdowns during this period, directly leading to a significant contraction in domestic zinc slag supply. Amid the supply-demand imbalance, the zinc slag payable indicator recently rose by approximately 2 percentage points.

For zinc oxide enterprises, over 60% of production uses zinc slag as raw material. The increase in raw material prices has directly translated into rigid cost pressures, continuously squeezing profit margins. However, in stark contrast to the strong cost-side increases, downstream rubber and ceramic consumer markets have not entered the expected peak season recovery, with overall demand remaining sluggish. The dual pressures of "rising costs and weak demand" have become the core contradiction in the current zinc oxide market.

II. Divergent Demand Across Segments: End-Use Industry Variations Drive Market Performance

(I) Rubber-Grade Zinc Oxide: Strong Auto Data Fails to Mask Mediocre Tire Industry Demand

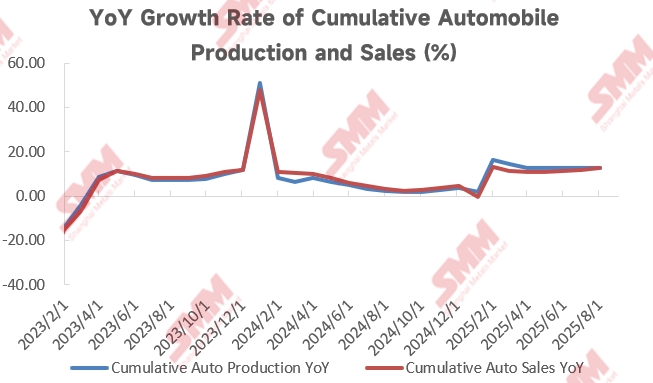

As the largest application segment for zinc oxide, rubber-grade zinc oxide demand is closely tied to the rubber products industry, particularly the tire sector. From end-use automotive data, China's cumulative auto production reached 21.051 million units in August, up 12.7% YoY, while cumulative sales were 21.128 million units, up 12.6% YoY. The overall data is impressive, providing theoretical support for rubber industry demand.

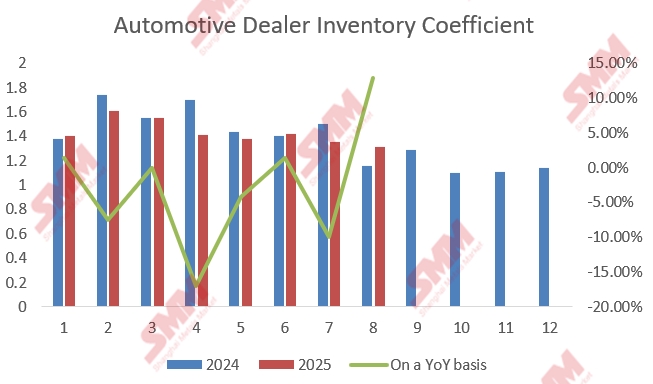

However, from the actual procurement side, the tire industry still faces multiple pressures. On one hand, data from the China Automobile Dealers Association shows that the automobile dealer inventory coefficient in August was 1.31. Although it decreased slightly by 0.04 MoM, it was up 12.9% YoY and remained above the reasonable range of 0.8-1.2. Under inventory pressure, large tire enterprises mainly focused on digesting previous stockpiling, maintaining low and stable procurement volume of rubber-grade zinc oxide. On the other hand, some tire factories, affected by insufficient orders and other factors, remain in a state of shutdown or production cuts. Among them, all-steel tire enterprises showed poor operating rates, while semi-steel tire enterprises also face dual issues of slowing production and sales growth and inventory backlog.

From enterprise feedback, the current rubber-grade zinc oxide market is polarizing: leading zinc oxide enterprises, relying on long-term cooperation with large tyre factories, have relatively stable orders; however, small and medium-sized zinc oxide enterprises, affected by insufficient order-taking from small and medium-sized rubber product manufacturers, have significantly weaker orders, with overall demand support being limited.

(II) Ceramic-grade zinc oxide: Real estate downturn drags on demand for ceramic-grade zinc oxide

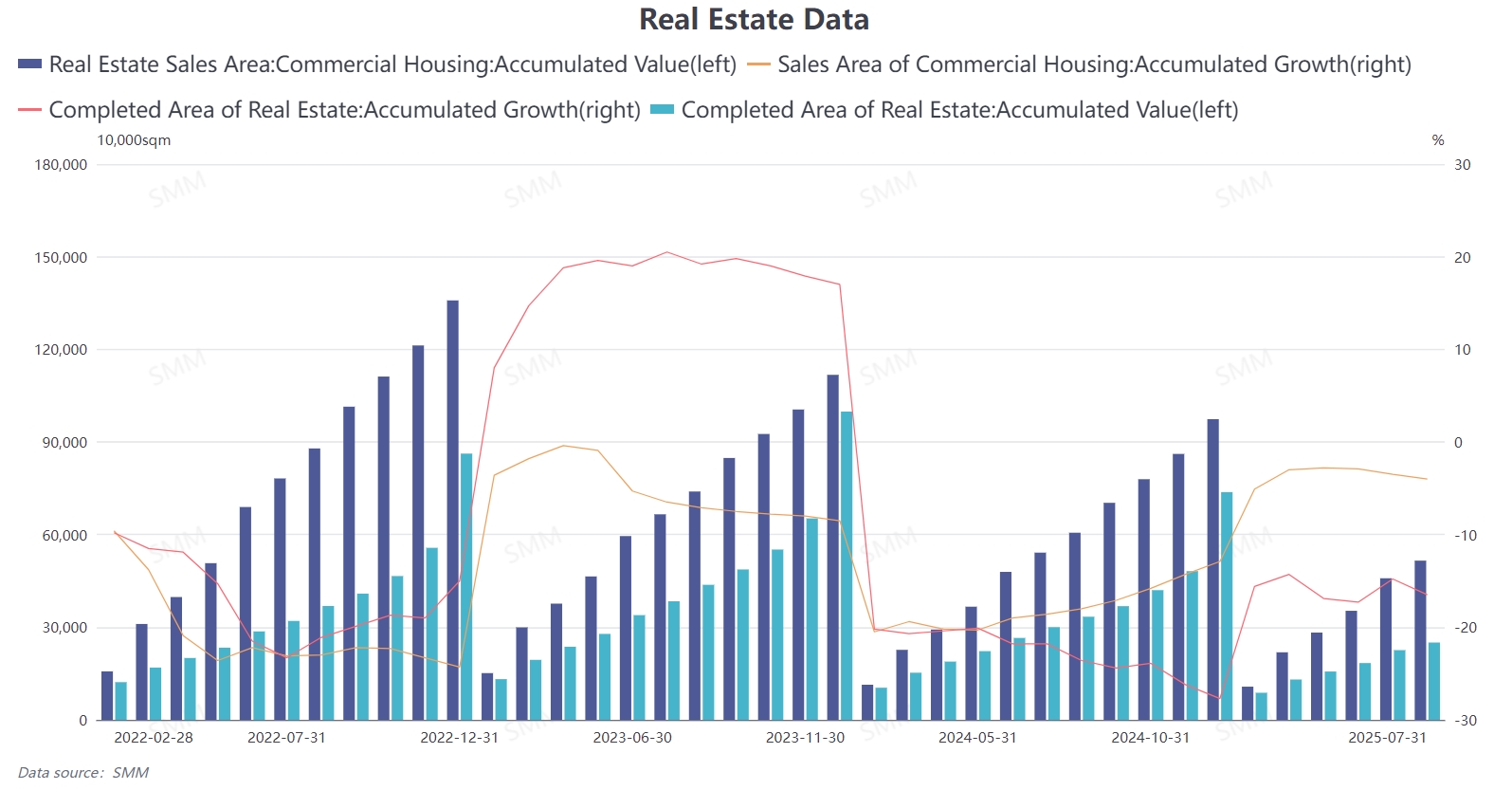

Ceramic-grade zinc oxide is mainly used in ceramic glazes, electronic ceramics, and other fields, and its demand is closely related to the real estate industry. According to real estate data, China's real estate sales area and completed area remained in negative growth in August, with cumulative YoY figures recorded at -4% and -16.5%, respectively. Downstream real estate demand continues to be sluggish, resulting in low procurement demand for ceramic-grade zinc oxide, which has become a major factor dragging down the market.

Although the high-purity ceramic-grade zinc oxide market has recently shown slight improvement, high-purity products account for a relatively small share of the overall ceramic-grade zinc oxide market, and their boosting effect on the overall market is relatively limited. The ceramic-grade zinc oxide market remains in a pattern of "weak demand and low transaction volume."

(III) Feed-grade zinc oxide: Transition between peak and off-peak seasons begins, but cost pressures constrain corporate profits

Feed-grade zinc oxide is primarily used as an additive in livestock and poultry feed, with demand fluctuating cyclically according to the peak and off-peak seasons of the breeding industry. Currently, as the weather cools, demand for feed-grade zinc oxide has shown marginal signs of improvement.

However, enterprises still face significant cost pressures: In the short term, environmental protection-related controls in North China in early September reduced production of low-grade zinc oxide, driving up the low-grade zinc oxide payable indicator. In the long term, since 2024, imports of low-grade zinc oxide have decreased YoY, coupled with declining blast furnace operating rates at domestic steel mills. These dual factors have jointly led to a sustained increase in the low-grade zinc oxide payable indicator. Under cost pressure, some enterprises producing active zinc oxide have had to reduce production to protect profits, further exacerbating uncertainty in market supply and demand.

(IV) Electronic-grade zinc oxide: Minimal raw material interference + solid demand support, market performance remains relatively stable

The production of electronic-grade zinc oxide primarily uses zinc ingot as raw material rather than zinc slag, making it less affected by the recent rise in the zinc slag payable indicator.

Demand side, the steady progress of State Grid Corporation of China's construction projects continues to support demand for electronic components. Meanwhile, domestic home appliance production maintained good growth momentum in August, further boosting demand for electronic-grade zinc oxide. Under these dual positive factors, demand for electronic-grade zinc oxide remains relatively stable overall, making it the most robust segment in the current zinc oxide market.

IV. Short-Term Outlook: Cost Pressure May Marginally Ease, Demand Recovery Remains Key

In the short term, as relevant control measures in the north are gradually lifted, galvanizing plants in North China are steadily resuming production. The supply of zinc slag is expected to increase accordingly, and the upward trend in the zinc slag payable indicator may moderate. Cost-side pressure for zinc oxide enterprises is anticipated to ease marginally.

However, in the long run, whether the zinc oxide market can escape its current difficulties still fundamentally depends on the recovery pace of downstream consumption. If end-use industries such as automobiles, real estate, and rubber achieve a substantial recovery in demand, driving synchronized growth across various segments, the zinc oxide market is expected to gradually enter a virtuous cycle of "stable costs and rising demand." Conversely, if demand remains persistently weak, enterprises will continue to face prolonged cost pressure.