SMM September 11 News:

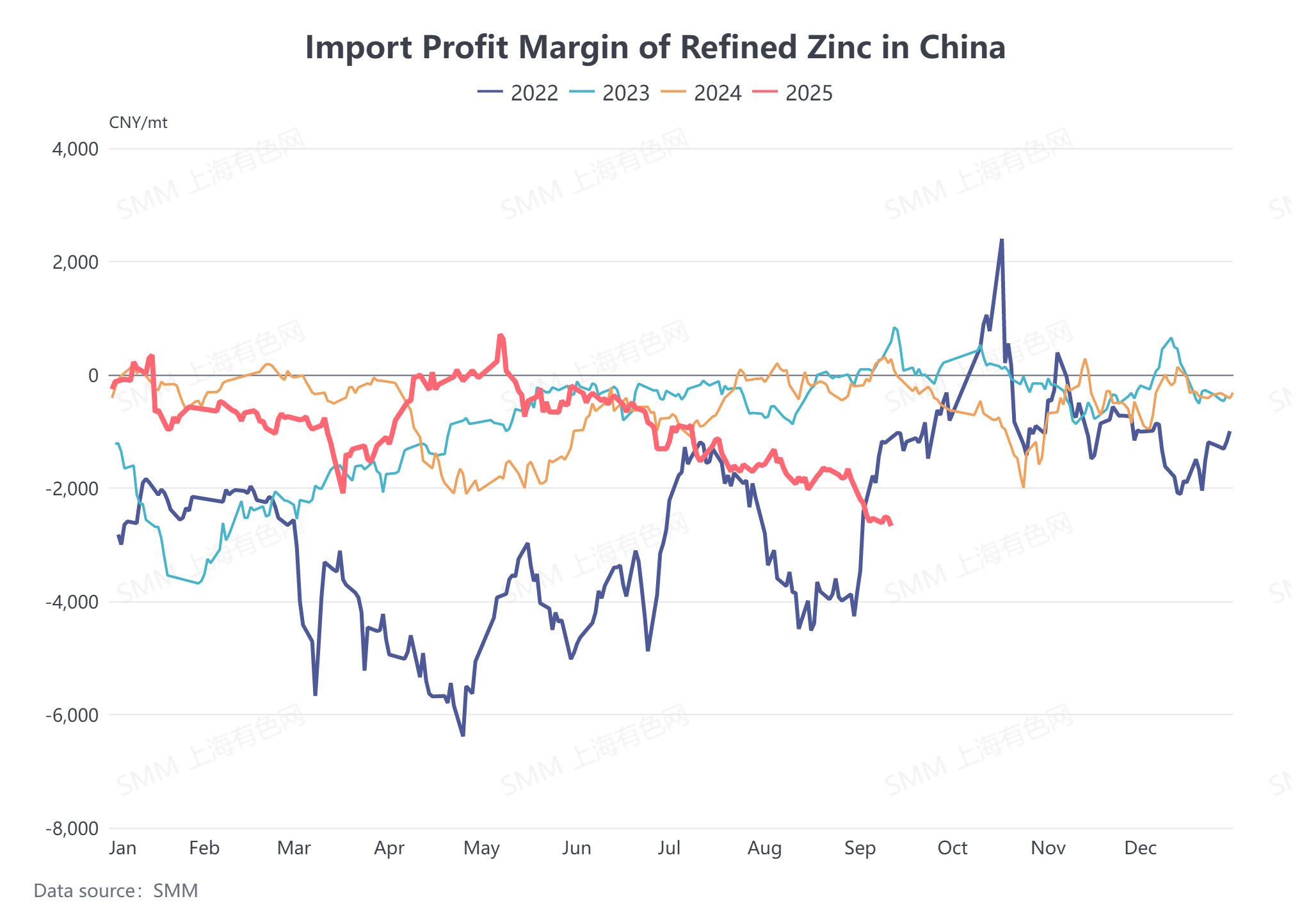

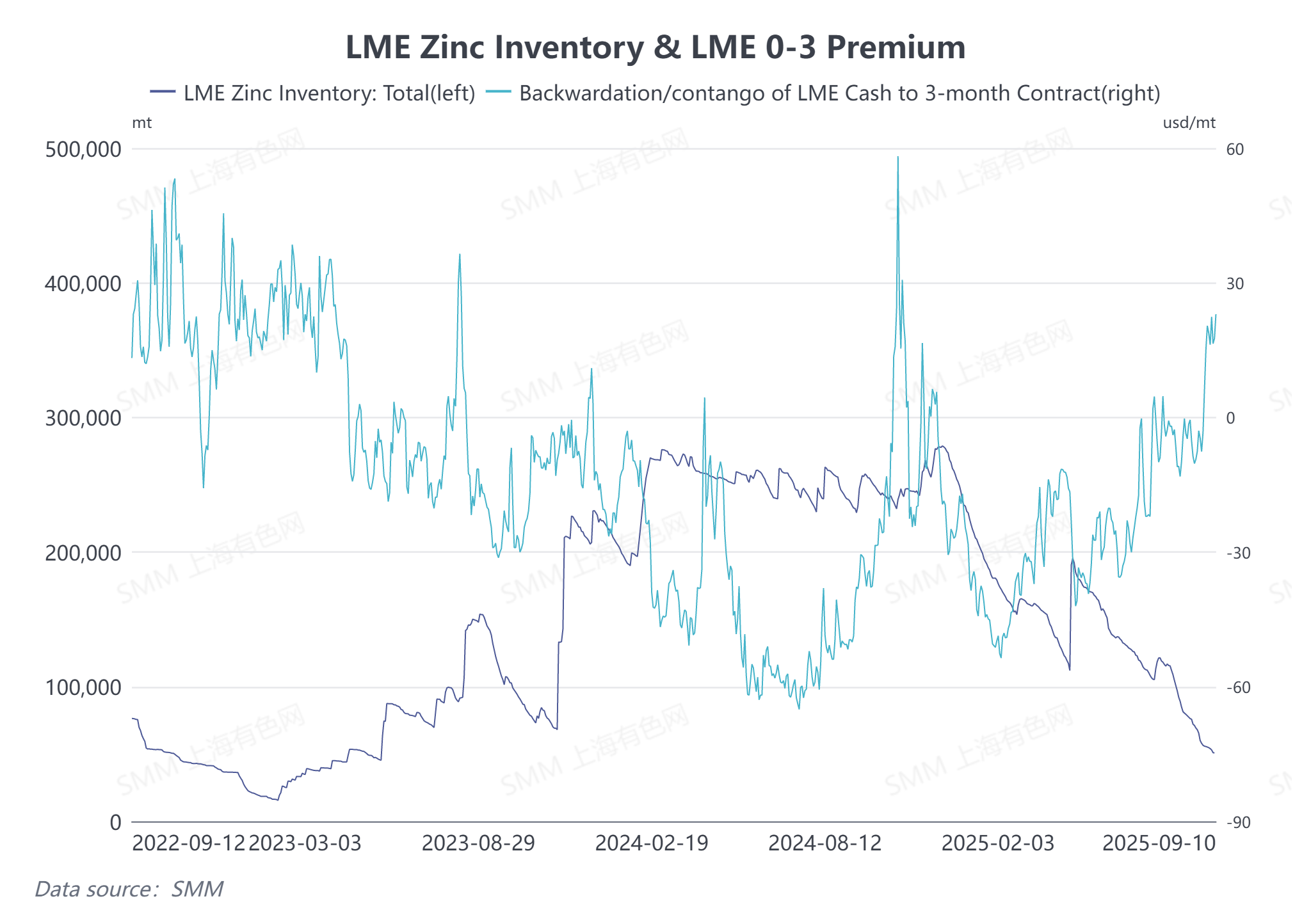

As of September 10, LME zinc inventory dropped to around 50,000 mt, hitting a low since June 2023, while the LME zinc 0-3 premium expanded to $23.01/mt. Amid "squeeze" risks, LME zinc prices continued to rise since late August. However, domestic zinc inventory kept accumulating, and SHFE zinc remained in the doldrums due to the surplus logic. The SHFE/LME price ratio weakened again, significantly narrowing China's zinc export losses. Market attention on the zinc export window gradually increased.

Historically, China’s zinc export window only opened in 2022 over the past decade.

In 2022, the Russia-Ukraine conflict triggered an energy crisis in Europe. Soaring electricity prices and energy shortages led to multiple overseas zinc smelters reducing or halting production. Reduced zinc supply drove continuous destocking of LME zinc, and LME zinc prices surged violently. At that time, domestic COVID-19 outbreaks led to persistently weak end-use consumption of zinc. Domestic zinc inventory fluctuated at highs. Against the backdrop of severe divergence in fundamentals between domestic and overseas markets, zinc import losses expanded to over 4,000 yuan/mt in March, prompting the opening of China’s zinc export window. This round of zinc exports lasted nearly seven months, peaking in May 2022 with a monthly net export volume of 32,300 mt and total annual exports of 80,900 mt.

Will China’s Zinc Export Window Open Again Soon?

As the SHFE/LME price ratio continues to weaken, China’s zinc import window has remained closed since May, and refined zinc imports narrowed significantly in Q3. Entering September, domestic zinc consumption has not shown significant improvement, while overseas LME zinc inventory continues destocking. As of September 10, the SMM #0 refined zinc price was 22,090 yuan/mt, and the SHFE/LME price ratio has fallen to around 7.6. According to estimates, current zinc import losses are around 2,500 yuan/mt, and exports still incur losses of over 1,000 yuan/mt. Currently, there is no export arbitrage opportunity for domestic zinc. However, if the SHFE/LME price ratio continues to weaken and import losses expand to around 4,000 yuan/mt, the domestic zinc export window may open accordingly.

(The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research and decision-making. Customers should make cautious decisions and should not replace their independent judgment with this information. Any decisions made by customers are not related to SMM.)