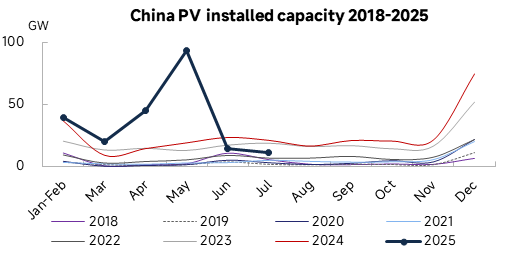

September has arrived, but the traditional September-October peak season effect in the wire and cable industry has not yet significantly materialized. The release of peak season demand is somewhat delayed, and market attention on the pace of demand release continues to rise. According to SMM, the expected operating rate for copper wire and cable enterprises in September is 72.46%, up 0.04 percentage points MoM. Currently, the industry as a whole is in a transitional phase from off-season to peak season, characterized by "insufficient upward momentum and limited downward adjustment." Due to the lag in peak season demand, the industry's prosperity remains stable without significant fluctuations. From the perspective of downstream sectors, the PV industry, affected by the previous installation rush, now sees a slowdown in the pace of demand release, limiting its ability to boost overall industry demand. The construction industry, facing both off-season and cyclical adjustment pressures, also experiences persistently weak demand, making it difficult to effectively drive growth in industry demand.

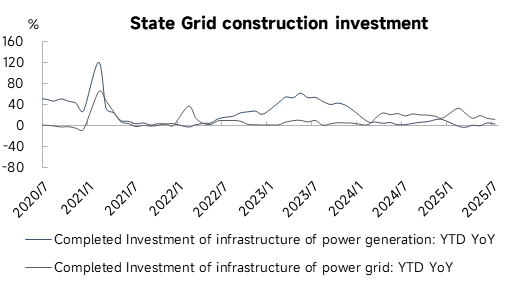

As a core downstream sector of the wire and cable industry, the power industry, affected by the overall weak macro demand environment, has underperformed expectations. However, significant divergence exists within the industry: specifically, the submarine cable sector, supported by stable demand from scenarios such as offshore wind power, continues to perform well, with production schedules remaining steady; orders from the two grid companies show notable differences—order releases from the Southern Grid have slowed down, with relatively weak demand, while orders from the State Grid have remained consistently stable, providing critical support for the operation of wire and cable enterprises.

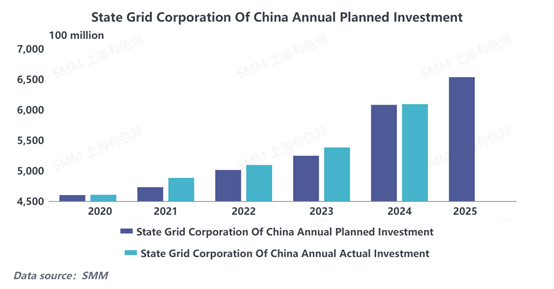

2025, as the concluding year of the 14th Five-Year Plan, sees State Grid planning to raise its investment to 650 billion yuan for the first time. Historically, State Grid's actual investment often exceeds the planned amount, indicating a strong expected demand boost for the wire and cable industry this year. In terms of investment progress, State Grid's cumulative investment in H1 reached 270 billion yuan, up 11.7% YoY, but it has not yet reached 50% of the annual planned investment. The market generally holds high expectations for the release of State Grid's investments in H2. According to SMM, wire and cable enterprises began sensing an increase in orders from State Grid in July, with the industry gradually transitioning into the final sprint towards the 650 billion yuan annual investment target. However, there has not been a significant surge in orders so far, and the market widely expects that a concentrated release of orders from State Grid will occur by late October.

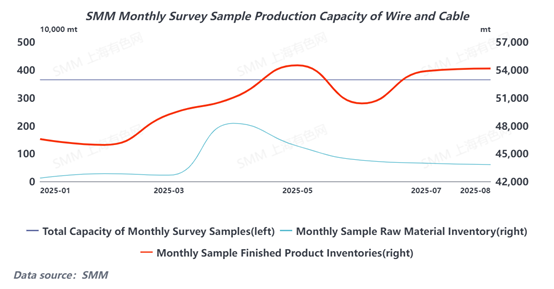

Currently, wire and cable enterprises have seen an increase in orders from State Grid, but overall demand has not improved significantly. The pace of cargo pick-up by end-users has slowed down, leading to an inventory buildup of finished products among copper wire and cable enterprises. The market has two main concerns: first, in the current macro environment, overall demand has not shown substantial improvement, and there is uncertainty about whether order growth can sustainably match inventory changes; second, under high investment targets, if short-term orders are accelerated to meet planned investment amounts, it may trigger the risk of demand being front-loaded, putting pressure on the steady release of subsequent industry demand.

Overall, in the short term, the steady release of orders from State Grid and the push to meet the annual investment plan in H2 are expected to continue providing crucial support for the stable operation of the wire and cable industry, partially offsetting the pressure from weaker demand in sectors such as PV and construction. However, the current order growth is accompanied by a slowdown in end-user cargo pick-up, inventory buildup of copper wire and cable products, and potential risks of demand being front-loaded, which still require industry attention.

![The Price Spread Between High-Quality Copper and Standard-Quality Copper Continued to Narrow, While SHFE Copper Spot Discounts Gradually Stabilized [SMM Shanghai Spot Copper]](https://imgqn.smm.cn/usercenter/YIaMU20251217171711.jpg)

![Inventory Continued to Decline, Suppliers Held Prices Firm Accordingly, and Spot Trades Were Better Than Yesterday [SMM South China Spot Copper]](https://imgqn.smm.cn/usercenter/KtfdC20251217171713.jpeg)