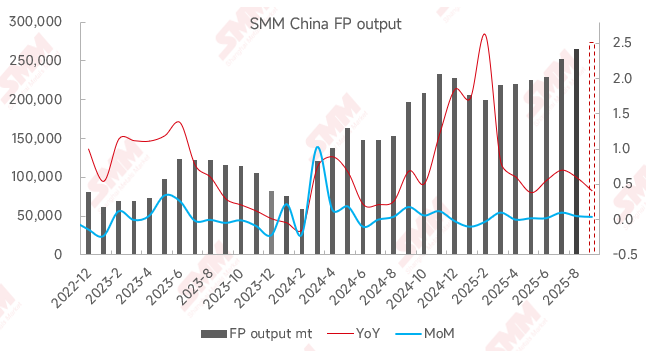

In August, the domestic production of iron phosphate showed a significant growth trend, with a month-on-month increase of 5% and a year-on-year increase as high as 59%, clearly indicating an expanding production capacity. Looking at the driving factors behind the increase, the core logic is concentrated in two major dimensions: demand pull and capacity release. On the one hand, integrated lithium iron phosphate enterprises had sufficient orders, directly driving up the production of in-house self-used iron phosphate and becoming an important support for production growth. On the other hand, some iron phosphate production enterprises actively expanded their output scale to match their capacity expansion plans, further boosting the overall industry production.

Coupled with the price fluctuations of lithium carbonate in August, this market change directly stimulated downstream lithium iron phosphate manufacturers to accelerate their inventory replenishment pace, indirectly driving up the market demand for iron phosphate. However, as the market share of integrated lithium iron phosphate enterprises continues to expand, the demand space for iron phosphate in non-integrated sectors has shown a shrinking trend. Against this background, the production capacity of iron phosphate in the industry remains in a continuous expansion channel, while the growth rate of overall market demand is relatively limited.

The subtle changes in the supply-demand relationship have forced iron phosphate enterprises to adjust their price strategies or upgrade product competitiveness to consolidate downstream customer orders and maintain market share. In terms of cost, iron phosphate enterprises faced dual pressures of "one relaxation and one tightening" in August: the industrial monoammonium phosphate market entered the traditional off-season, with prices showing a significant decline, providing some cushion for enterprise cost control; however, the price of ferrous sulfate continued to rise, significantly increasing the cost pressure on enterprises in the iron source procurement process and squeezing profit margins.

Looking ahead to September, with the further release of downstream demand, the traditional peak season for the iron phosphate industry is approaching, market confidence is gradually recovering, and most iron phosphate enterprises hold optimistic expectations for the September market. Based on production forecasts, it is expected that domestic iron phosphate production will continue to grow in September, with a month-on-month increase of approximately 4% and a year-on-year increase of up to 61%, and the industry as a whole is expected to maintain a good operating trend.