1H 2025 underscored the complexity of Indonesia’s nickel ore market, where pricing was increasingly influenced not only by physical supply and demand but also by shifting policy landscapes and broader macroeconomic signals. Saprolite ore remained supply-constrained, with prices heavily shaped by cost-push factors and procurement urgency. By contrast, limonite market saw a more demand-led recovery narrative, gaining momentum from the recovery and ramping-up of HPAL production capacity.

1H 2025 marks the second year of RKAB three-year validity period. In this analysis, quarterly review will be discussed as below:

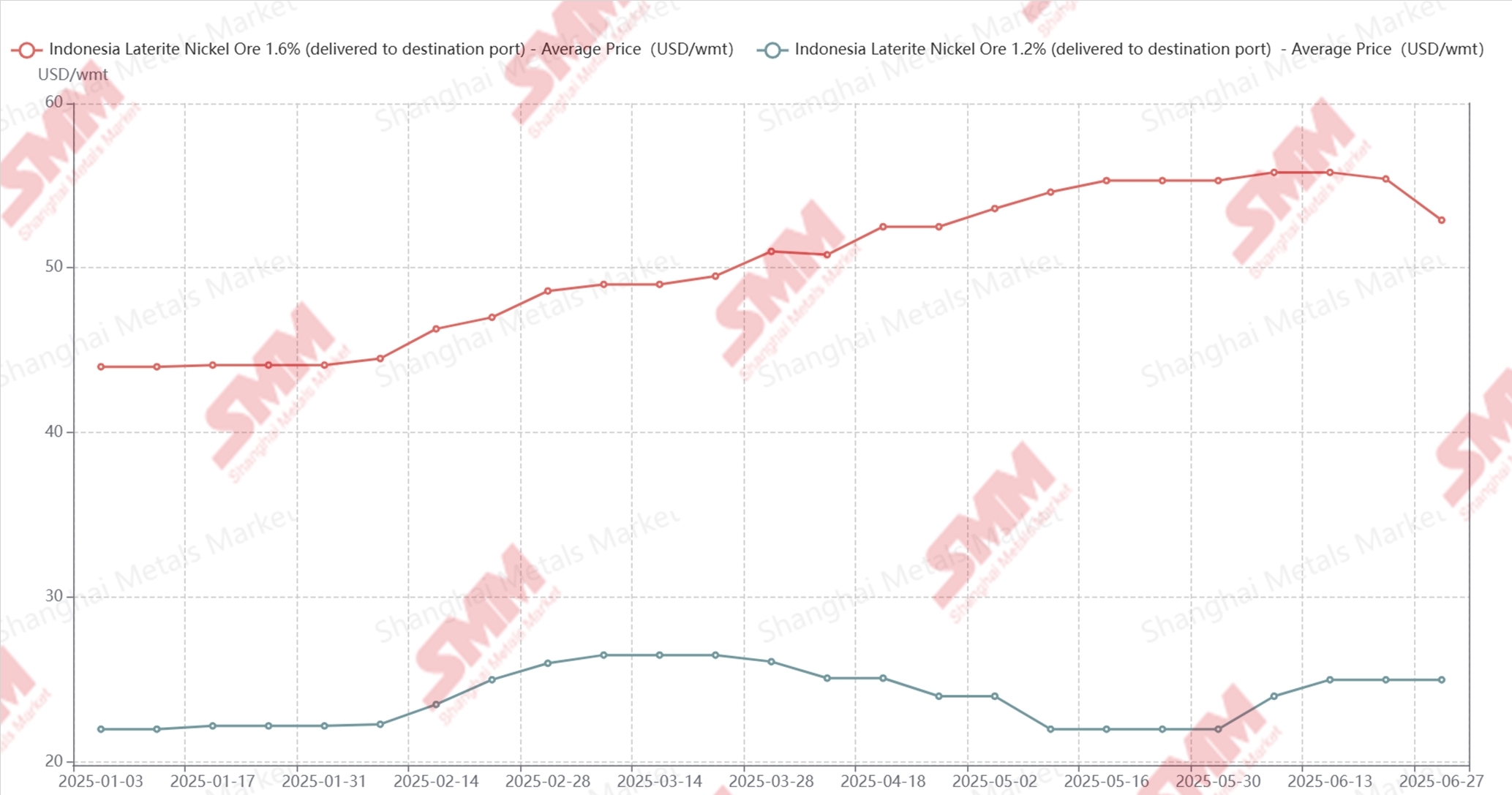

Indonesian Nickel Ore Price 1H 2025

Q1 2025: Policy Tailwinds and Seasonal Tightness Drive Prices Up

Nickel ore pricing in Q1 began on a strong footing. Prices for saprolite ores remained elevated, supported by firm premiums that climbed to an average of $22/wmt by the end of March. Limonite prices tracked a similar trend early on, with 1.3% ore with around $26–28/wmt. Market sentiment was buoyed by the shift to a semi-monthly HPM pricing system, which reinforced bullish expectations.

This upward pressure stemmed largely from tight supply conditions, particularly in Sulawesi, where the prolonged rainy season hindered mining activity and logistics. The quota system under RKAB—although technically in place—faced implementation delays, leaving much of the approved capacity underutilized in the early months. As a result, ore supply remained limited, especially for higher-grade saprolite. Demand-side dynamics also contributed to pricing strength. Many Indonesian NPI producers entered the year with relatively low ore inventories, a typical seasonal pattern compounded by the timing of the Chinese New Year. This might have triggered a wave of restocking from late January through March, which further tightened the market.

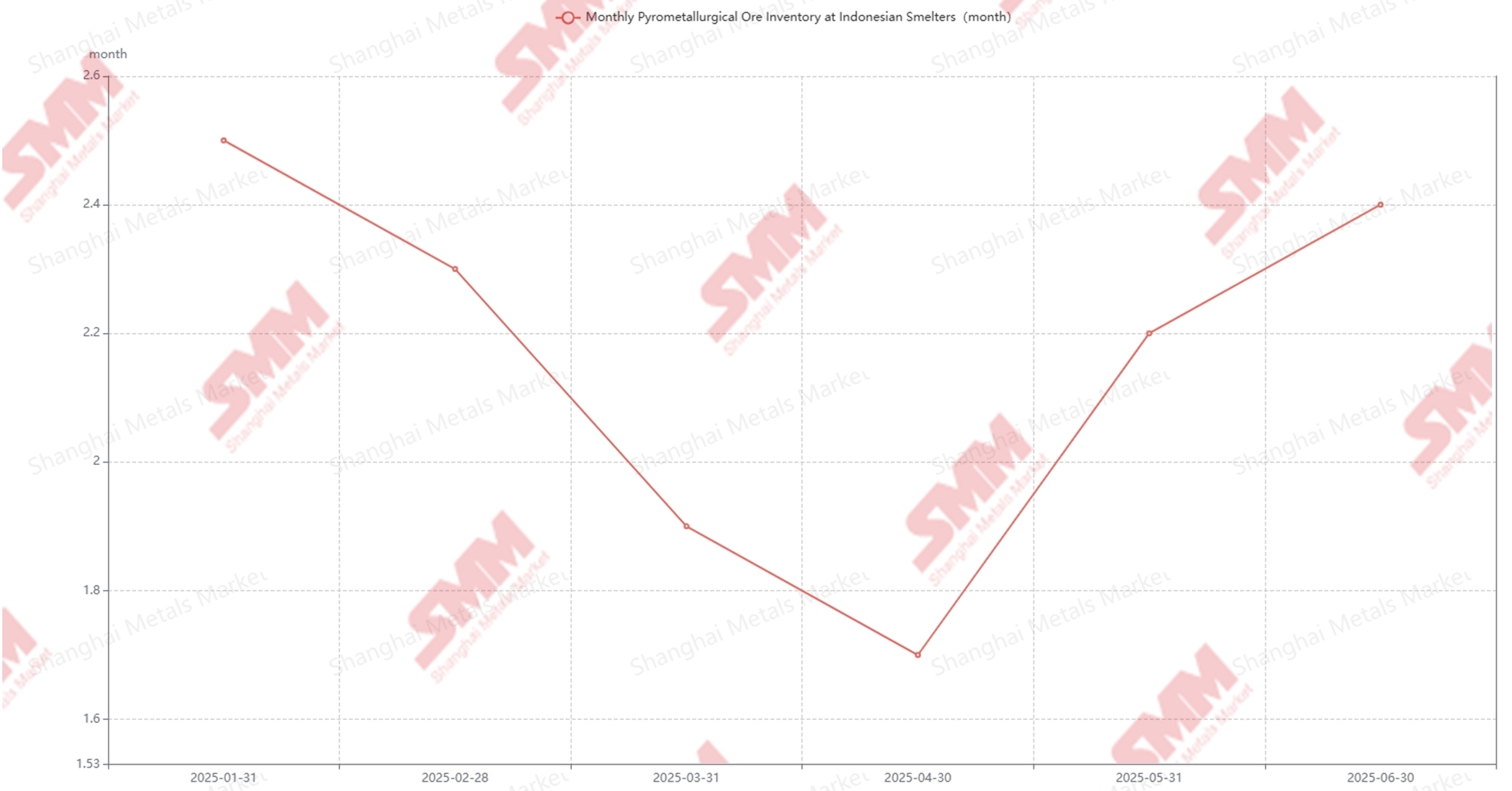

From a stockpiling perspective, smelters—particularly RKEF operators—struggled to maintain sufficient supply, with most holding less than two months’ worth of feedstock. High fuel prices and logistic bottlenecks exacerbated the situation, leading to failed restocking attempts in some areas. The urgency to secure cargoes might have pushed buyers to accept higher prices throughout the quarter, although the overall inventory levels are in a down trend due to anticipations of better conditions for next quarter.

Q2 2025: Market Divergence, Cost Pressure, and a Turning Point for Limonite

Q2 ushered in more complex dynamics. Saprolite and limonite markets began to diverge meaningfully—both in terms of price movement and underlying fundamentals.

For saprolite, prices continued climbing through May, reaching as high as $57.3/wmt for 1.6% Ni ore, before easing slightly by the end of June. The supply situation remained constrained, with continued rainfall in Sulawesi and Halmahera delaying mining and loading operations. Although some RKAB quota approvals began to trickle in by June, they were insufficient to normalize the market. On the demand side, smelters are trying to restock inventories in the second quarter due to low inventory. Therefore, increased demand forcefully drives the nickel ore prices up.

Adding to this price increase was the implementation of the new PNBP royalty structure on April 26, which raised nickel royalty rates from 10% to 14%. According to SMM, this initiative added roughly $1–2/wmt to mining costs. Therefore, mining companies held prices firm and would favor price increase to alleviate the royalty burden, while RKEF smelters have little choice but to accept the higher prices in order to replenish their ore inventories.

On the inventory side, stockpiling conditions improved modestly on Q2 2025, wtih most smelters replenishing their stock. In April, the supply of saprolite reached its lowest inventory levels, approximately 1.7 months. Therefore, smelters are gradually increasing their ore supply until June despite the cost-inversion burden aggravates.

Pyrometallurgical Ore Inventory in 1H 2025

In terms of the limonite market, ore supply has not shown significant tightness. Due to geological formation and mining sequence of limonite as the first layer. Increased royalty rates has made an overall less profit for limonite compared to saprolite with the same mining cost. However, demand took a hit in early Q2 after a tailing accident at the Morowali HPAL plant in March. Limonite of 1.3% price decreased to $25.5-26.5/wmt. Moving towards May, as the operations gradually resumed and other HPAL projects ramped up, demand also recovered, resulting in a price rebound to $26–28/wmt by June, which are also aided by expectations of limited RKAB quota for end of 1H 2025.

Outlook for 2H 2025: Another Policy Reform and Potential Supply Ease

Entering the third quarter of 2025, Indonesia’s nickel ore market has generally shown a downward trend. By mid-August, the final price for 1.6% laterite nickel ore ranged between USD 50.5–53.8/wmt, with mainstream premiums realized at around USD 24–26/wmt. Meanwhile, 1.3% laterite nickel ore prices edged down to USD 25.5–27.5/wmt, averaging a 1.9% decline compared with the final price levels in Q2.

On the policy front, the Ministry of Energy and Mineral Resources (ESDM) announced that a revision of the RKAB framework—shifting from a three-year to an annual approval system—will be finalized in early September. Mining companies are expected to begin submitting their annual RKAB applications by the end of September, with approvals for 2026 quotas likely to start in October. According to SMM research, Indonesia’s nickel ore RKAB quota in 2025 stands at around 300–310 million tonnes, with most of the pending revisions anticipated to be completed by late August. This could bring a marginal increase in supply, while demand has weakened since July, as several smelters cut or suspended production.

Weather conditions have also improved, with most areas of Sulawesi experiencing more favorable conditions and only occasional light rainfall. In contrast, Halmahera and Obi continued to see frequent precipitation. Overall, mining conditions in Indonesia are easing compared with the previous quarter.In the saprolite market, cost-inversion pressures have deepened in early Q3. However, Indonesian NPI prices have shown a relatively firm upward trend from mid-July to mid-August, though negative margins persist for certain smelters. Despite this, sentiment in the NPI market has improved compared with the sharp losses seen in the previous quarter. For limonite, the approval of RKAB revisions has led to an oversupply situation, as demand from HPAL smelters remains limited. Many new HPAL projects have yet to commence large-scale ore procurement, placing additional pressure on prices.

Looking ahead, the completion of RKAB quota applications, potential ramp-ups of new HPAL lines, and the restart of certain RKEF smelters will be key drivers in shaping market dynamics in the second half of the year. In addition, the approval process for 2026 RKAB applications will heavily influence pricing expectations and smelter procurement strategies.

In summary, nickel ore demand is expected to remain resilient amid intense competition between miners and smelters. However, prices are likely to stay volatile through year-end, with limited upside potential and some downside risks still in play.