SMM August 20 News:

Zinc prices rose in 2024, with a tight supply in the zinc fundamentals. In 2025, the center of zinc prices pulled back, and the supply fundamentals became more relaxed, marking the beginning of a turning point in the zinc oxide raw material landscape.

What specific changes have occurred in the zinc oxide raw material market, and how will it develop going forward?

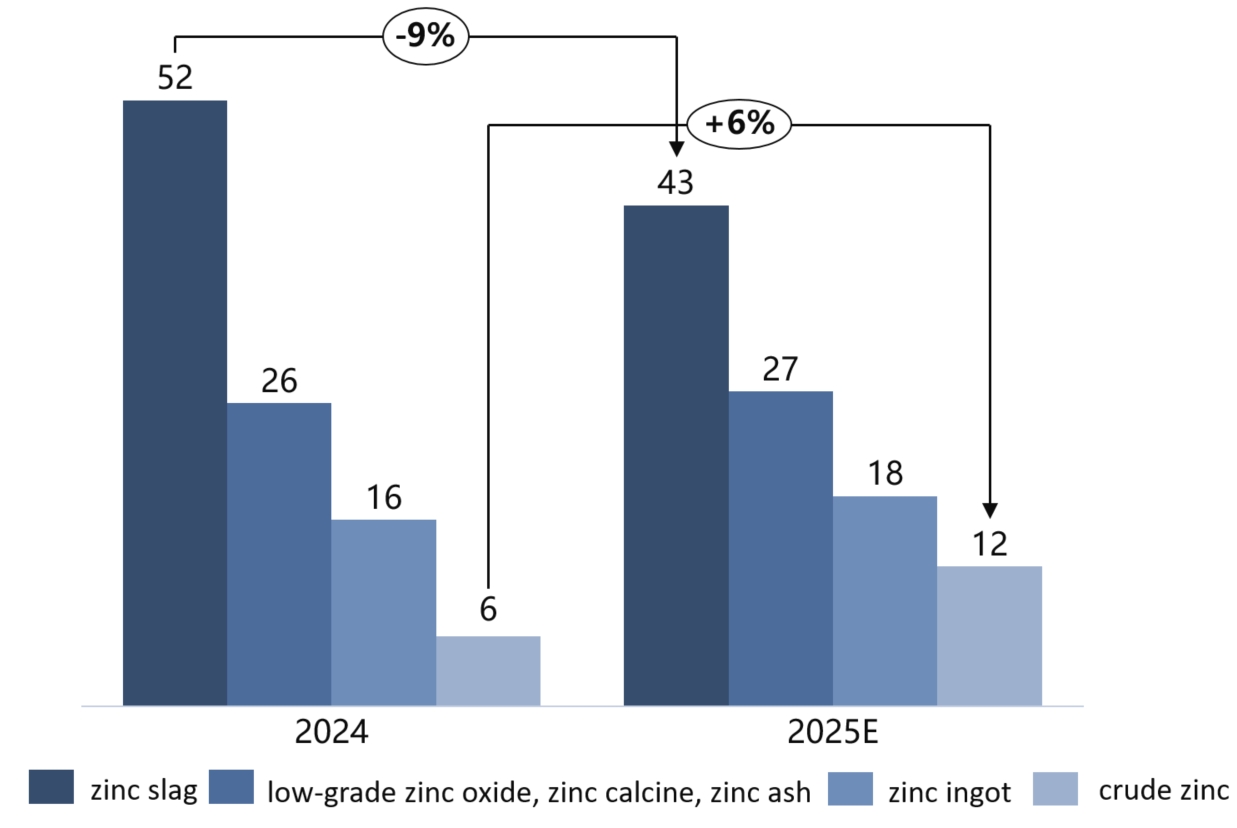

According to SMM's communication and understanding, the most noticeable shift in the current raw material market is the increased use of crude zinc by zinc oxide enterprises and the decreased use of zinc slag. However, zinc slag still holds the largest share in the zinc oxide raw material market, though its proportion has decreased from 52% in 2024 to 43% in 2025. The share of zinc ingots increased from 16% in 2024 to 18%, while that of crude zinc rose from 6% in 2024 to 12% in 2025.

In terms of cost-effectiveness, the current market's crude zinc contains over 99% zinc, with its pricing coefficient mostly at 93 or 94; while zinc slag contains around 95-96% zinc, with its pricing coefficient at 92 or 93. The pricing for both is mainly based on 0# or 1#, with a base price difference of 70 yuan/mt. In this scenario, it is more cost-effective for zinc oxide enterprises to use crude zinc in certain periods, driving up the usage of crude zinc by zinc oxide enterprises in H1.

Looking ahead, downstream zinc consumption is currently in an off-season, with low operating rates for galvanized sheets and galvanized structural components. Additionally, as the parade ceremony approaches in early September, some small-scale galvanizing enterprises in Tianjin have already halted production, which may exacerbate the shortage of raw materials in the short term. Meanwhile, influenced by recent LME trends and macro sentiment, zinc prices are more likely to rise than fall, showing a volatile trend. However, after the weakening of external forces, zinc prices are expected to return to the fundamental logic center of strong supply and weak demand, with a slight downward shift in the center. Nevertheless, the tight supply situation in the zinc oxide raw material market will not change during the off-season, and the zinc slag market supply is expected to remain tight.

Furthermore, crude zinc supply is currently in an undersupply state, with coefficients continuously rising since the beginning of the year, and a small portion of the market's crude zinc coefficients have now reached around 95.

Given the current tight supply of zinc oxide raw materials and the ongoing fluctuations in zinc prices, enterprises are expected to engage in intense competition over the usage ratios of zinc ingots, zinc slag, and crude zinc. SMM will continue to monitor specific changes in the zinc oxide raw material market.