SMM, August 8:

By July 31, the SHFE zinc main contract closed at 22,345 yuan/mt, down 150 yuan/mt (0.67%). Zinc prices bottomed out in July, hitting a monthly low of 21,865 yuan/mt in early month before rebounding to 23,070 yuan/mt by month-end, supported by domestic funding for the program of large-scale equipment upgrades and consumer goods trade-ins, the implement major national strategies and build up security capacity in key areas, and anti-"rat race" competition policies. How will zinc prices perform in August?

Macro Front: Multiple Factors Intertwined

In July, China's domestic market saw sustained macro sentiment recovery driven by favorable policies, with anti-"rat race" competition measures gradually expanding across industries. Meanwhile, expectations for US Fed interest rate cuts intensified, US tariff negotiations with multiple countries progressed, and the third round of formal China-US trade talks in Sweden at month-end resulted in a consensus to extend the suspension of additional 24% tariffs and corresponding countermeasures for another 90 days. Currently, Russia and the US plan talks next week, while recent dovish signals from US Fed officials further strengthened market expectations for a September rate cut.

Supply side: The loose pattern continues

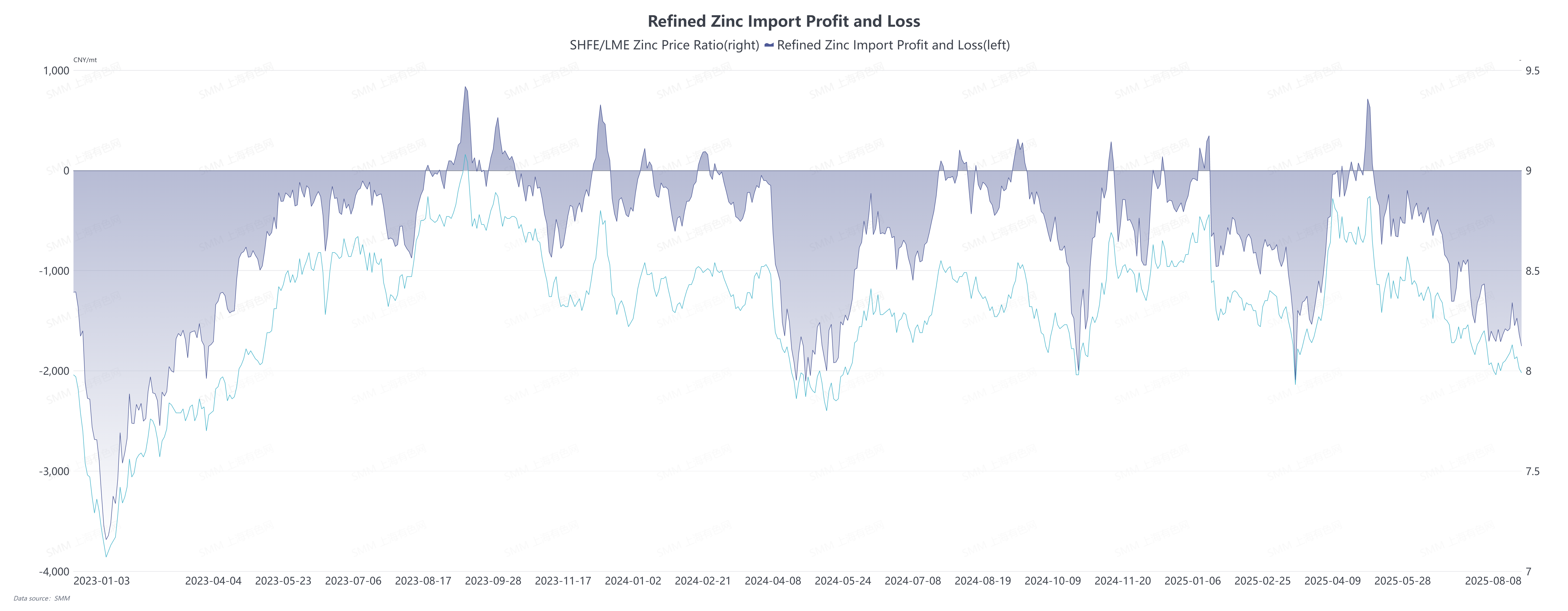

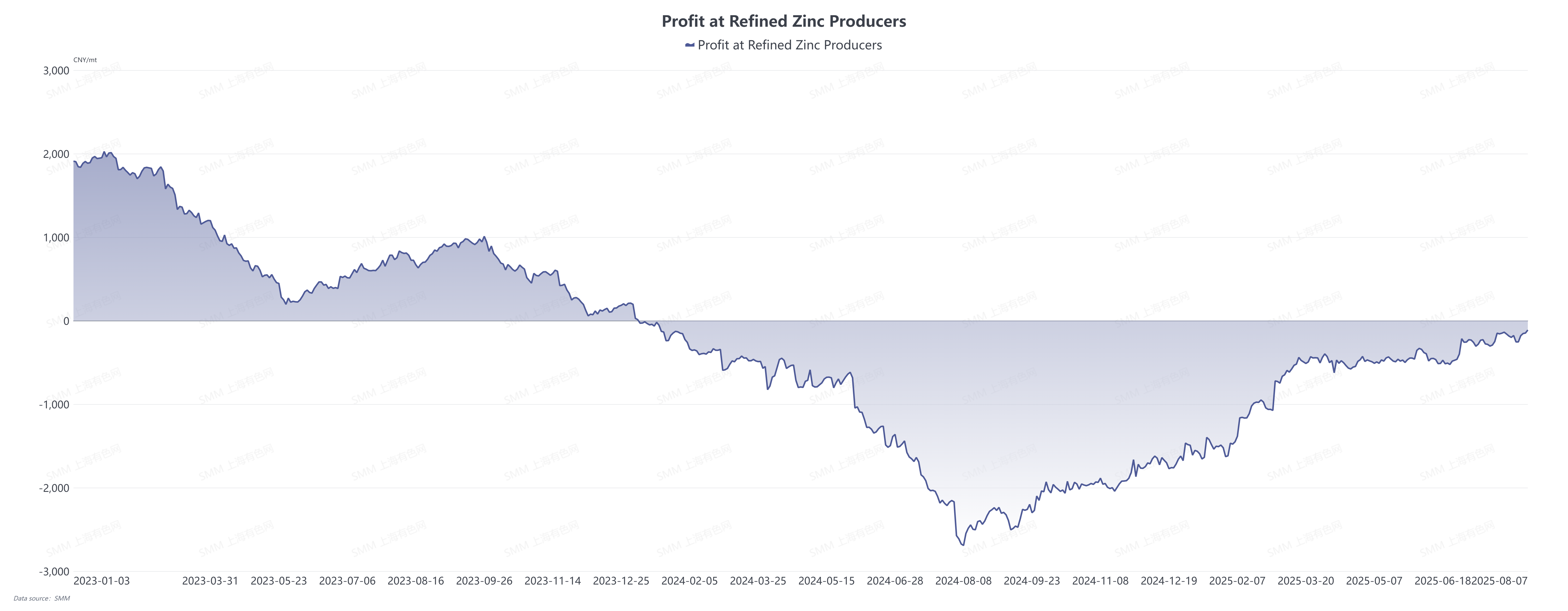

From the supply side, the domestic zinc market has generally shown a loose trend. According to SMM data, zinc concentrate production in July was 346,800 mt, up 24,300 mt MoM. In terms of imports, China's zinc concentrate imports in June reached 330,000 mt (in mt), showing a 32.67% MoM decline but a 22.42% YoY increase, indicating that the supply of raw materials remains resilient. In the refined zinc sector, production in July was 602,800 mt, up 3.03% MoM. However, the import window remained closed in July. Affected by the overseas market outperforming domestic market, subsequent zinc ingot imports are expected to arrive mainly in the form of long-term contracts, but it is difficult to reverse the overall expectation of loose domestic supply. Currently, sulphuric acid prices in most domestic regions are at historical highs, driving a continuous expansion of smelters' profit margins and sufficient production enthusiasm. It is expected that domestic refined zinc production in August will further increase to 621,500 mt, up 3.1% MoM, and the loose supply expectation will continue.

Demand side: Off-season characteristics are prominent

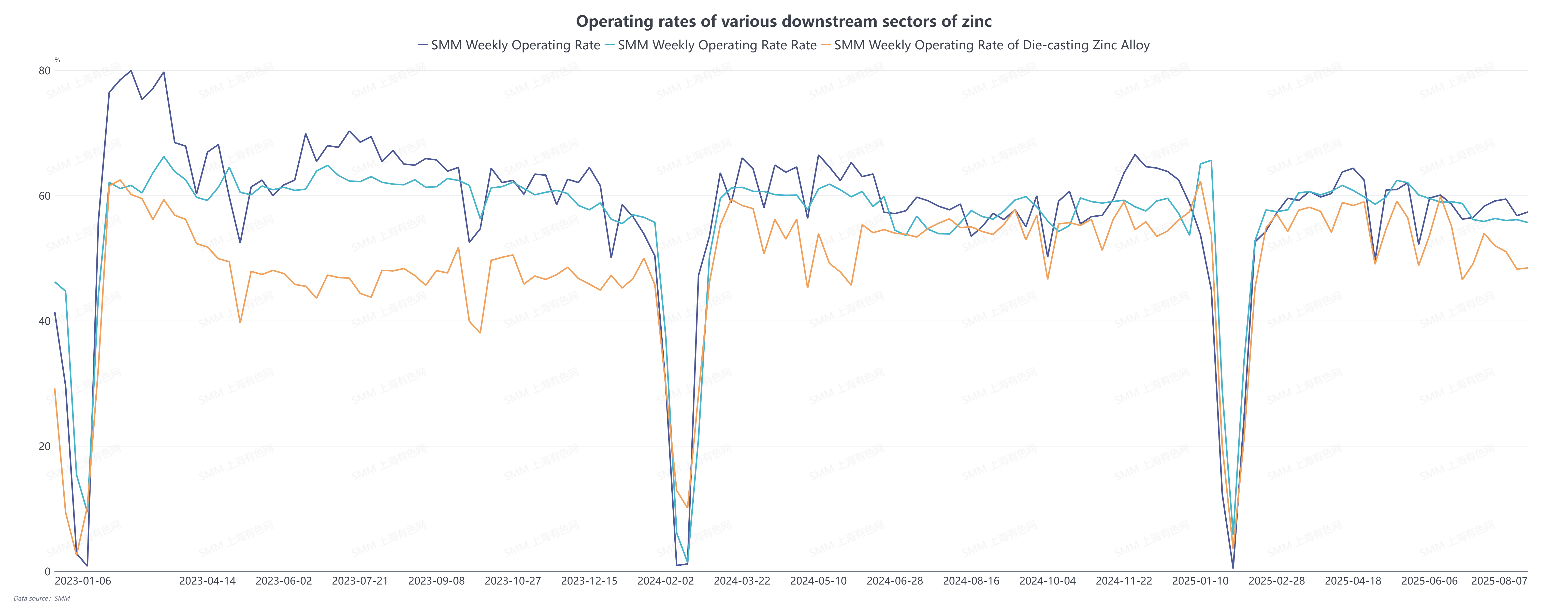

From the consumption side, affected by both the seasonal off-season and extreme high-temperature weather in July, the overall downstream demand for zinc has been weak: infrastructure project construction has been hindered, leading to a decline in the operating rates of both galvanized structural parts and galvanized sheets; the operating rate of die-casting zinc alloy has also been weak due to low demand and the impact of low-priced products; orders for zinc oxide terminals in various sectors have also pulled back simultaneously. Looking ahead to August, the effect of the seasonal off-season will continue, and it is expected that the operating rates of galvanizing and die-casting zinc alloy will further decline. Although the zinc oxide sector is expected to see a slight recovery driven by feed-grade orders, overall, the operating rates of various downstream zinc sectors will remain weak.

From the overall situation in August, the fundamental pattern of oversupply and weak consumption in the domestic market will continue—with clear expectations of a loose supply side and limited substantive improvement on the demand side due to the off-season. However, overseas markets have shown significant divergence: LME zinc inventory continues to decline to a low level, and concentrated open interest has driven the overseas market to hold up well. Under the linkage mechanism between domestic and overseas markets, SHFE zinc may continue to exhibit the characteristic of being "more likely to rise than fall" in the short term, driven by the overseas market. However, once the marginal support from the overseas market weakens, the fundamental supply-demand imbalance in the domestic market will become the dominant factor, and price fluctuations will center more around the supply-demand pattern.