Aluminum Scrap: This week, the domestic aluminum scrap market saw a strong upward trend overall, with the price center rebounding significantly. Spot primary aluminum prices continued to rise, and as of August 7, the SMM A00 price closed at 20,690 yuan/mt, up 110 yuan/mt from last Thursday. Driven by the intensifying shortage of aluminum scrap supply and the policy adjustment period, purchases were mainly for immediate needs, and transactions were sluggish. There was a clear differentiation among aluminum scrap varieties: shredded aluminum tense scrap (water price) saw prices rise from 16,700-17,200 yuan/mt (tax-exclusive) to 17,100-17,600 yuan/mt (tax-exclusive), with a cumulative increase of 400 yuan/mt; baled UBC prices increased from 15,150-15,650 yuan/mt to 15,400-15,900 yuan/mt, with an increase of 250 yuan/mt. Regional linkage strengthened, with east China (Shanghai, Jiangsu, Shandong) closely following the aluminum price increases, with daily adjustments up to 200 yuan/mt; while quotes in Jiangxi, Anhui, and other places lagged behind, initially remaining flat before gradually increasing. The price difference between primary metal and scrap fluctuated more sharply, with the price spread of machine-made aluminum tense scrap in Foshan narrowing from 1,944 yuan/mt to 1,736 yuan/mt. The price adjustments for aluminum tense scrap raw materials far exceeded those for A00, leading to a rapid narrowing of the price difference between primary metal and scrap in the short term. In terms of downstream secondary aluminum, high temperatures suppressed operating rates, and order reductions constrained transactions. It is expected that the price center of the aluminum scrap market will remain fluctuating at highs next week. Affected by the policy adjustment period related to secondary aluminum, it will push up the prices of raw material purchases. The tight supply of shredded aluminum tense scrap (water price) resources will intensify, and the operating range is expected to fluctuate between 17,000-17,500 yuan/mt (tax-exclusive); baled UBC will still be suppressed by weak end-use demand, with an operating range of 15,300-15,800 yuan/mt (tax-exclusive).

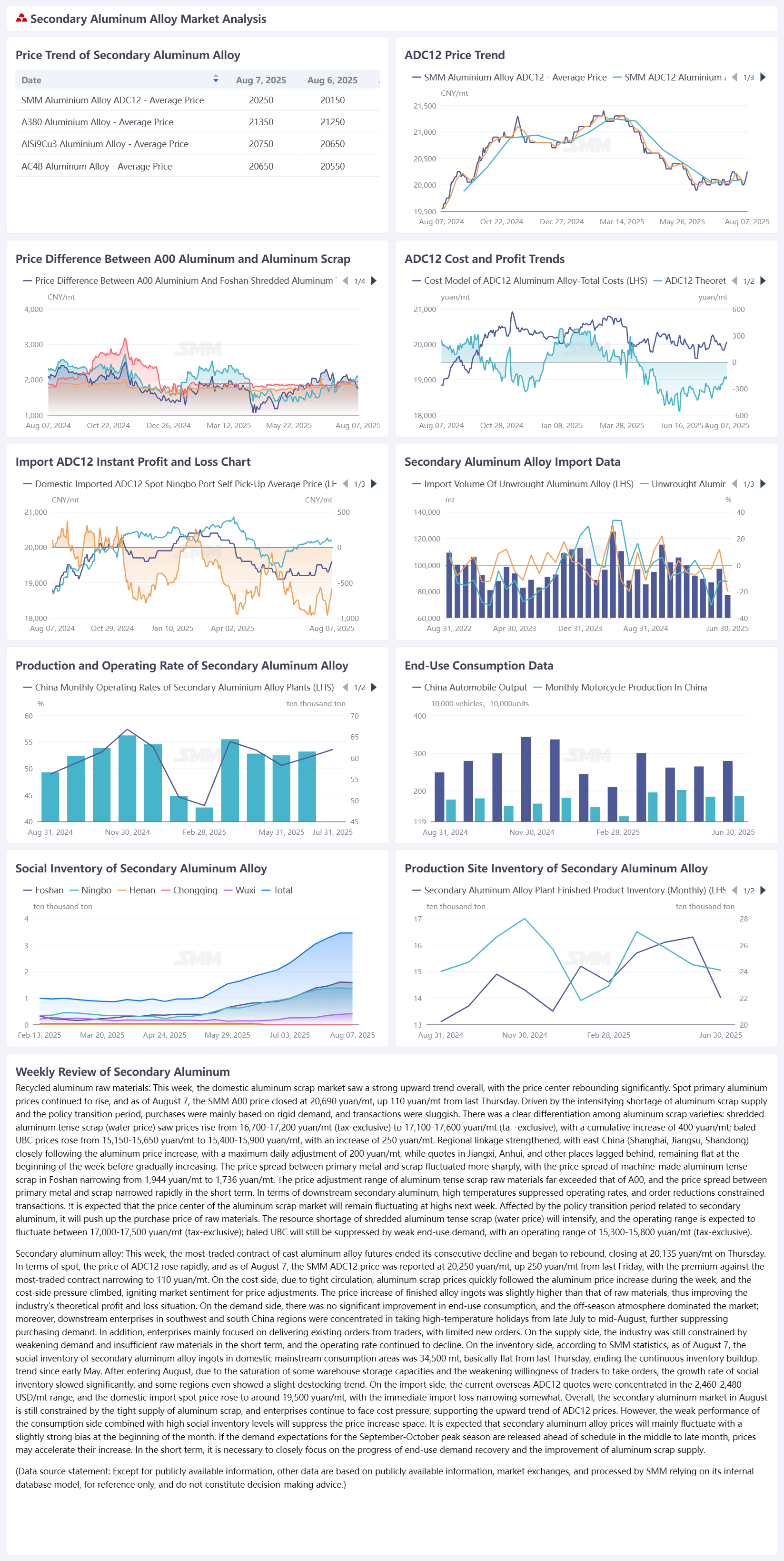

Secondary Aluminum Alloy: This week, the most-traded contract of cast aluminum alloy futures ended its consecutive decline and began to rebound, closing at 20,135 yuan/mt on Thursday. In terms of spot, the price of ADC12 rose rapidly, and as of August 7, the SMM ADC12 price was reported at 20,250 yuan/mt, up 250 yuan/mt from last Friday, with the premium against the most-traded contract narrowing to 110 yuan/mt. On the cost side, due to tight circulation, aluminum scrap prices quickly followed the aluminum price increases during the week, and the cost pressure climbed, igniting market sentiment for price adjustments. The price increase of finished alloy ingots slightly exceeded that of raw materials, thus improving the industry's theoretical profit and loss situation. On the demand side, there was no significant improvement in end-use consumption, and the off-season atmosphere dominated the market; moreover, downstream enterprises in southwest and south China regions were concentrated in taking high-temperature holidays from late July to mid-August, further suppressing purchasing demand. In addition, enterprises mainly focused on delivering existing orders from traders, with limited new orders. On the supply side, the industry was still constrained by weakening demand and insufficient raw materials in the short term, and the operating rate continued to decline. On the inventory side, according to SMM statistics, as of August 7, the social inventory of secondary aluminum alloy ingots in domestic mainstream consumption areas was 34,500 mt, basically flat from last Thursday, ending the continuous inventory buildup trend since early May. After entering August, due to the saturation of some warehouse storage capacities and the weakening willingness of traders to take orders, the growth rate of social inventory slowed significantly, with some regions even showing a slight destocking trend. On the import side, the current overseas quotes for ADC12 were concentrated in the 2,460-2,480 USD/mt range, and the domestic import spot price rose to around 19,500 yuan/mt, with the immediate import loss narrowing somewhat. Overall, the August secondary aluminum market is still constrained by the tight supply of aluminum scrap, with enterprises facing continuous cost pressure, supporting the upward trend of ADC12 prices. However, the weak performance of the consumption side, coupled with high social inventory levels, will suppress the price increase space. It is expected that secondary aluminum alloy prices will mainly fluctuate with a slightly strong bias at the beginning of the month. If the demand expectations for the September-October peak season are released ahead of schedule in the mid-to-late month, prices may accelerate their increase. In the short term, it is necessary to closely monitor the progress of end-use demand recovery and the improvement of aluminum scrap supply.