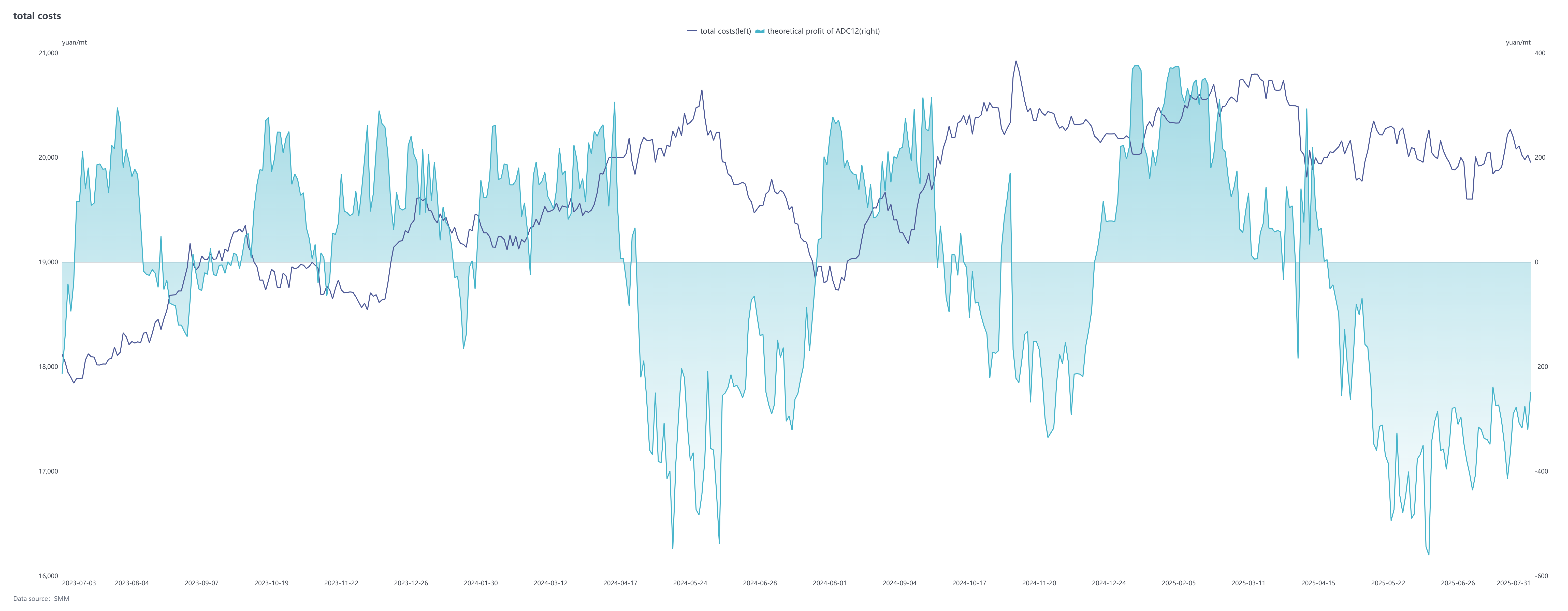

In terms of prices, in the futures market, the trend of the most-traded cast aluminum alloy 2511 contract in July generally followed that of SHFE aluminum, with the overall center moving upward, showing a pattern of rising first and then falling: after hitting bottom at 19,685 yuan/mt in early July, it fluctuated upward, climbing to 20,350 yuan/mt in mid-month to set a new high since listing, and then experiencing a slight correction at month-end, closing at 20,075 yuan/mt as of August 6. In the spot market, the price of ADC12 fluctuated smoothly overall, with weak changes in both rises and falls. It closed at 20,150 yuan/mt on August 5, rising slightly by 150 yuan/mt MoM from early July. The theoretical premium of spot ADC12 against the most-traded futures contract gradually narrowed from 330 yuan/mt in early July to around 100 yuan/mt.

The cost side continues to face pressure. Affected by the reduced output of new materials during the off-season, the suppression of old material dismantling due to high temperatures, and the decline in imported supplements, the circulation of aluminum scrap has become increasingly tight. Secondary aluminum enterprises face difficulties in purchasing and have seen a decline in their raw material inventory. Meanwhile, the price of silicon, an auxiliary material, has experienced a long-awaited increase, with the price of oxygen-blown #553 silicon rising by 1,300 yuan/mt within the month. Copper prices have also risen. The increase in the cost of core raw materials has kept the industry in a state of theoretical loss, although the extent of the loss has narrowed slightly. Overall, the cost still provides support for the price of ADC12.

The cost side continues to face pressure. Affected by the reduced output of new materials during the off-season, the suppression of old material dismantling due to high temperatures, and the decline in imported supplements, the circulation of aluminum scrap has become increasingly tight. Secondary aluminum enterprises face difficulties in purchasing and have seen a decline in their raw material inventory. Meanwhile, the price of silicon, an auxiliary material, has experienced a long-awaited increase, with the price of oxygen-blown #553 silicon rising by 1,300 yuan/mt within the month. Copper prices have also risen. The increase in the cost of core raw materials has kept the industry in a state of theoretical loss, although the extent of the loss has narrowed slightly. Overall, the cost still provides support for the price of ADC12.

Demand side, secondary aluminum orders in July performed better than expected. Firstly, orders from new energy vehicles (NEVs), motorcycle parts, and other sectors were robust, supporting orders for some enterprises. Secondly, after the listing of cast aluminum alloy futures, futures and spot traders acquired large quantities of delivery brand or non-delivery brand ADC12, which to some extent hedged against the decline in downstream orders for enterprises and mitigated the fluctuations between traditional peak and off-seasons. Since August, market demand has weakened, with enterprises mainly focusing on fulfilling existing orders from traders, and new orders have been limited. Currently, there are no obvious signs of improvement on the consumption side, and it is necessary to closely monitor whether the "September-October peak season" can drive the market to stabilize and recover after mid-August.

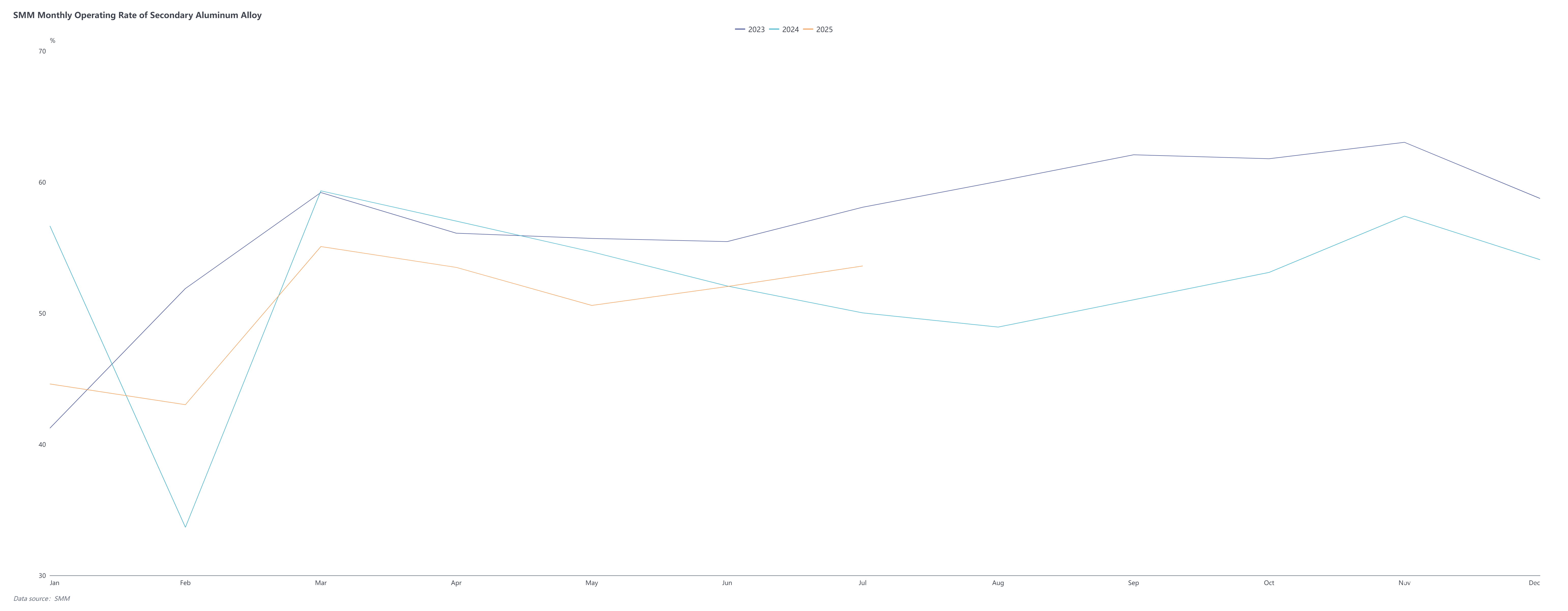

In terms of supply, the operating rate of the secondary aluminum alloy industry increased by 1.57 percentage points MoM to 53.60% in July, up 3.58% YoY. The operating rate in July showed a differentiated trend, with large factories benefiting from sufficient orders and the advantages of delivery brands, continuously improving their operating rates and becoming the main driving force for the overall industry operating rate. However, small and medium-sized enterprises generally faced issues such as raw material shortages, production losses, or order contractions, with some enterprises in a state of prolonged production cuts or even shutdowns. Entering August, with no significant improvement on the demand side, the off-season atmosphere dominated the market, and terminal automakers in regions such as Southwest and South China entered high-temperature holidays, which will further suppress procurement demand. Without favorable support, it is expected that the industry's operating rate will be under pressure in August.

Entering August, the secondary aluminum market is still facing a shortage of aluminum scrap supply, and it is difficult to alleviate the cost pressure on enterprises in the short term. The downside room for ADC12 prices is limited. However, the weak performance of the consumption side and the high social inventory have constrained the upside room for prices. At the beginning of the month, secondary aluminum alloy prices will continue to be adjusted within a narrow range. If the demand expectations for the "September-October peak season" are realized ahead of schedule in the mid-to-late month, driving a recovery, prices are expected to stabilize and rebound. In the short term, it is necessary to focus on the recovery of end-use demand, the supply of aluminum scrap, and the impact of futures trends on spot cargo.