SMM July 29 News:

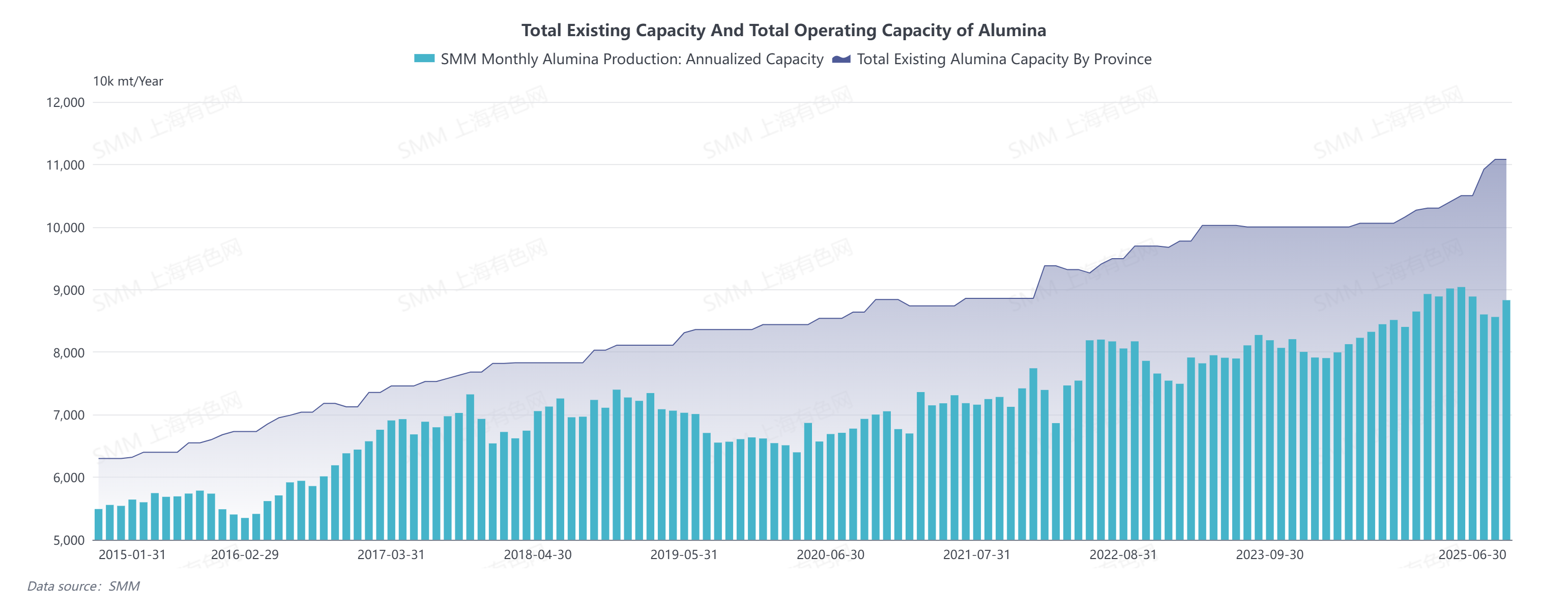

Reviewing H1 2025, China's alumina existing capacity and operating capacity both hit record highs. The country's alumina existing capacity increased by 7.3 million mt/year to 110.32 million mt/year, while the monthly average operating capacity reached 88.24 million mt/year, up 7.42 million mt/year (9.2%) YoY and 1.85 million mt/year (2.1%) compared with H2 2024. From January to June 2025, China's cumulative metallurgical-grade alumina production totaled 43.68 million mt, with net alumina exports reaching 1.075 million mt. Domestic aluminum production demand amounted to 41.78 million mt, resulting in an overall alumina surplus and a downward price trend.

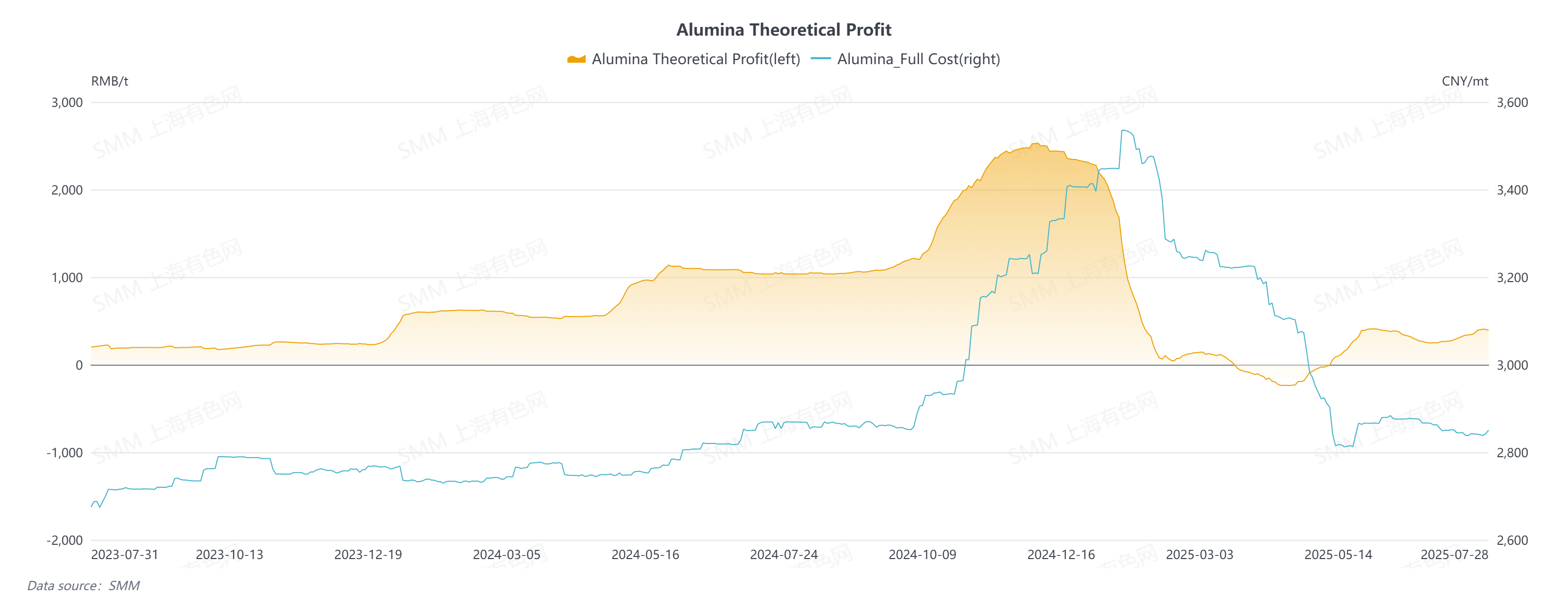

In 2024, raw material constraints limited alumina production growth, pushing alumina prices to a decade-high. Entering 2025, the lingering effects of high prices kept alumina profitability strong. According to SMM's daily cost-profit model, the theoretical profit for the alumina industry reached 2,279 yuan/mt on January 2, turning negative only by mid-March. Stimulated by high ore prices, bauxite supply increased, lifting raw material constraints. Boosted by profitability, alumina operating capacity rose, shifting the market into sustained surplus and triggering a rapid price pullback, followed by fluctuations around cost levels.

Monthly supply-demand and price trends:

In January-February, spot alumina prices fell sharply, but producers remained profitable, maintaining moderate production enthusiasm. Operating capacity continued to rise, reaching 90.17 million mt/year and 90.41 million mt/year, respectively.

In March, alumina prices continued declining, but ore price drops lagged. Spot prices gradually approached production cost lines, reducing overproduction. Some producers cut output due to ore supply or cost issues, lowering operating capacity. However, sustained prior profitability strengthened loss tolerance, with most producers avoiding maintenance, keeping capacity high.

In April-May, monthly average spot alumina prices hit H1 lows, causing severe losses. Producers selectively cut output, reducing supply and shifting the market into deficit. From May, spot prices rebounded from lows, peaking between late May and early June.

In June, alumina prices maintained a downtrend, but the monthly average rose MoM, improving profitability. Some idled capacity resumed, coupled with new capacity ramping up, lifting annualized operating capacity back above 88 million mt/year.

H2 outlook: Raw material supply is unlikely to constrain alumina operating capacity, with the market expected to remain in surplus. Spot prices may fluctuate around cost levels.

Cost side, bauxite prices trended downward in H1, while caustic soda prices also fell significantly from year-start, reducing alumina costs.

In Q1, SMM's imported bauxite CIF index averaged $101.42/mt, with alumina average costs at 3,337 yuan/mt. In Q2, ore prices dropped sharply, with the CIF index falling 22.5% to $78.57/mt, pulling average costs down to 2,942 yuan/mt. Assuming H2 imported ore averages $75/mt and domestic ore prices stabilize, alumina average costs may range between 2,800-2,900 yuan/mt. With lower cost lines, alumina prices are likely to remain in the doldrums, fluctuating around costs.