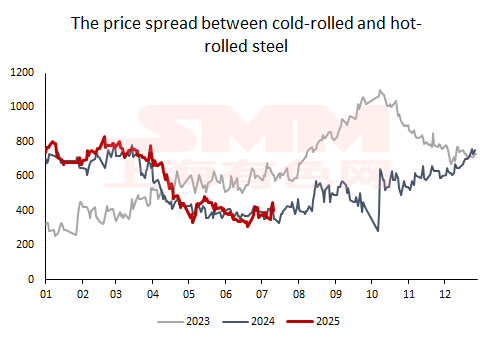

• The price spread between cold-rolled and hot-rolled steel ended its downward trend and entered a range-bound movement.

According to SMM data, as of July 24, the average SMM price spread between cold-rolled and hot-rolled steel for this month was 382 yuan/mt, remaining stable MoM from the June average. Since Q2, the price spread between cold-rolled and hot-rolled steel has continued to narrow. On the one hand, due to the escalation of tariff conflicts between China and the US, steel product exports have been impacted, directly leading to a blockage in the release of cold-rolled steel demand, which in turn caused a rapid decline in the spot price of cold-rolled steel. On the other hand, from March to May, the hot-rolled steel market performed well during the peak season, with demand showing strong resilience, while production was temporarily affected by maintenance at steel mills. The fundamentals of the hot-rolled steel market were far better than those of the cold-rolled steel market, also driving the price trend of hot-rolled steel to be stronger than that of cold-rolled steel. Under the combined influence, the price spread of cold-rolled steel contracted significantly. The low point of the price spread between cold-rolled and hot-rolled steel in 2025 occurred at 310 yuan/mt on July 2. Entering July, the price spread between cold-rolled and hot-rolled steel ended its continuous downward trend since Q2 and entered a range-bound movement.

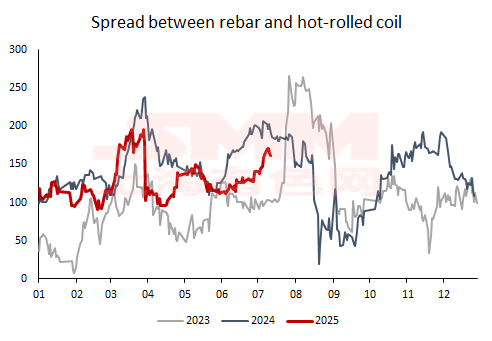

- The HRC-rebar spread is within the normal range

From mid-May to the present, the HRC-rebar spread has gradually widened. As of July 24, the HRC-rebar spread of the most-traded contract on SMM was 162 yuan/mt, up 22% MoM from July, and at a medium level compared to the same period in previous years. In the short term, under the backdrop of the off-season in Q3, with frequent occurrences of high temperatures, rainfall, and extreme weather, outdoor construction projects are facing severe challenges. However, the demand from the manufacturing sector is relatively less affected by seasonal factors. The fundamental pressure on HRC is slightly less than that on rebar. Coupled with the relatively high price elasticity of HRC, it is expected that the HRC-rebar spread will fluctuate within the range of 130-170 yuan/mt in the short term.

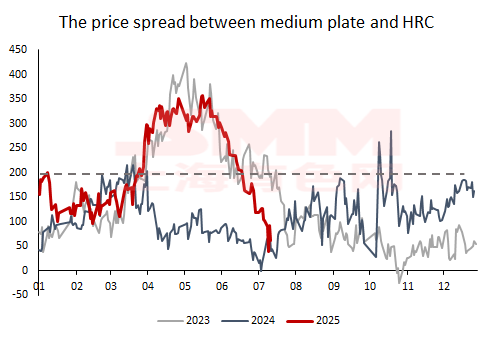

- The price spread between medium plate and HRC narrowed significantly since May, with a trend similar to that in 2023

In the first five months, the price spread between medium-thickness plates and HRC gradually widened amid fluctuations, primarily driven by the robust demand from downstream industries such as shipbuilding and wind power for medium-thickness plates. The price trend of medium-thickness plates was significantly stronger than that of HRC and other varieties, even experiencing an uptick against the market trend around mid-April. However, the price spread began to narrow significantly from the end of May. As of July 24, the SMM price spread between medium-thickness plates and HRC was 63 yuan/mt, hitting a year-to-date low of 39 yuan/mt on July 22, down 53% MoM from July. What caused the significant narrowing of the price spread between medium-thickness plates and HRC?

On one hand, when the price spread between medium-thickness plates and HRC exceeds 200 yuan/mt and persists for a period, steel mills will adjust the flow of hot metal, increasing production of medium-thickness plates while cutting production of HRC. From mid-April to mid-June, as steel mills redirected their hot metal flows, the fundamental supply-demand imbalance for domestic medium-thickness plates significantly increased, leading to a rapid price correction. Meanwhile, HRC prices fluctuated rangebound. During the decline in medium-thickness plate prices, the price spread between medium-thickness plates and HRC "narrowed".

On the other hand, from May to the present, domestic steel prices have experienced a decline followed by a rebound. As of July 25, the nationwide average price of HRC increased by 239.6 yuan/mt MoM from early May, while the nationwide average price of medium-thickness plates decreased by 46.6 yuan/mt MoM from early May. Given that HRC has stronger financial attributes and is more significantly influenced by macroeconomic and industrial news than medium-thickness plates, during the price rally, HRC prices increased at a faster pace than medium-thickness plates. As a result, the price spread between medium-thickness plates and HRC significantly narrowed.

The price spread trends among different steel varieties each had their own "styles" in H1. What about H2? Let's wait and see.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)