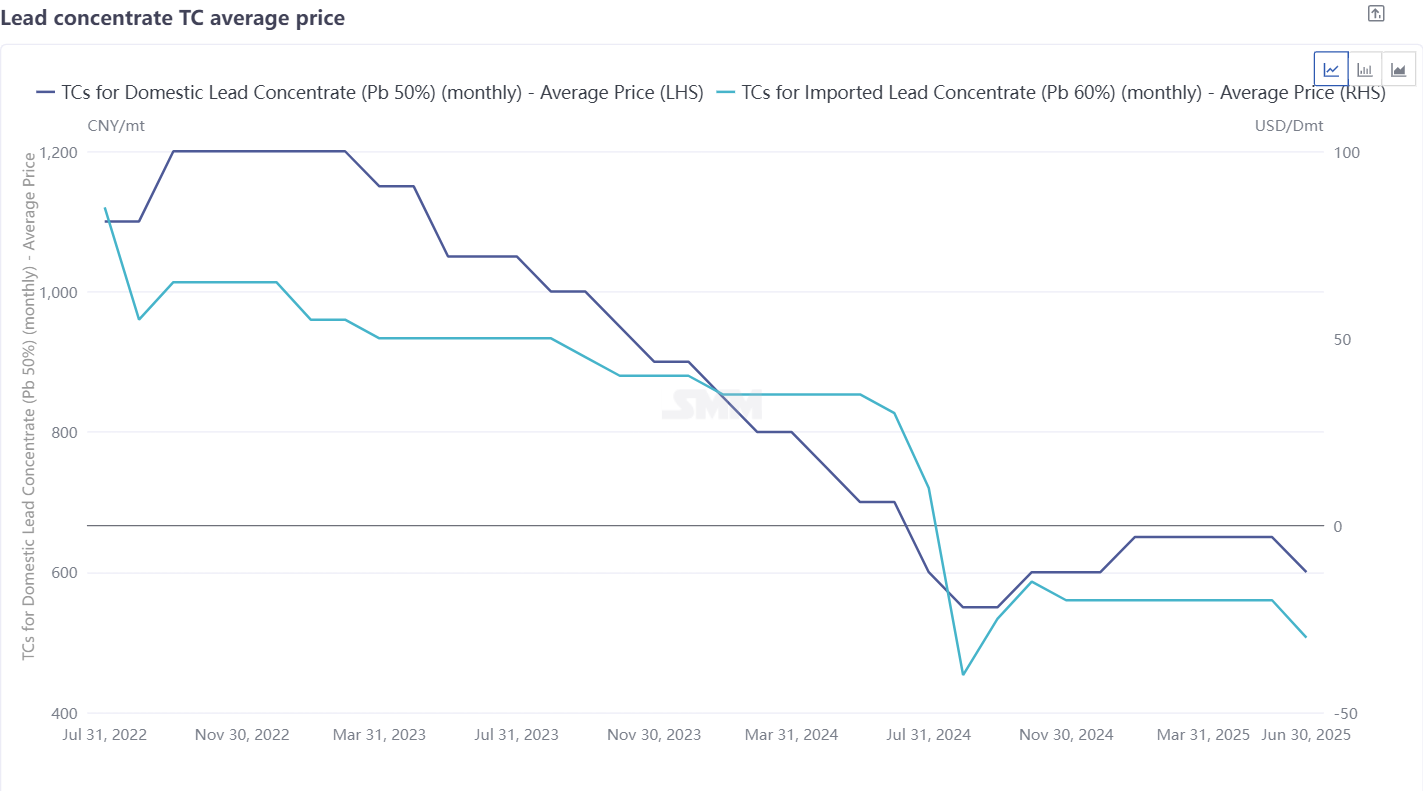

Driven by the strong performance of precious metals in July, domestic silver-lead ore processing fees continued their downward trend, with market structural differentiation intensifying. Most suppliers of silver-lead ore chose to covertly reduce the processing fees for silver-bearing lead concentrates. As the revenue from lead smelting by-products rose with the popularity of precious metals, smelters seeking comprehensive returns were generally willing to pay lower lead processing fee deductions for lead concentrates rich in silver and other minor metals. Consequently, tender and bid TC prices below mainstream quotations occasionally emerged in the market.

The significant rise in silver prices also indirectly influenced the intention to adjust processing fees for lead ore—

Low-silver ores (<200g/mt) had symbolic pricing coefficients of 0.2-0.3, with some mines incorporating the price fluctuations of precious metals into lead processing fees during negotiations. This was mainly because mines hoped to gain from the rise in precious metal prices after the significant increase in silver prices. When silver prices were below 7,500 yuan/kg, they usually did not price the small amount of silver enrichment, leading to an "invisible" drop in actual processing fees.

The coefficients for medium-low silver ores (300-500g/mt) rose to 0.8-0.83. A smelter indicated that without a reduction in lead ore processing fees, it was no longer possible to obtain the coefficient quotations of 0.78-0.8 in the first half of the year for such low-silver lead ores in late July.

For other lead concentrates with varying silver grades, the silver pricing coefficients remained stable overall after multiple rounds of increases. The coefficients for high-silver ores (>2.5kg/mt) reached the ceiling of 0.92-0.93, with quotations above 0.94 often including premiums for rare and scattered metals. This was mainly because after the silver content in lead concentrates exceeded 2.5kg/mt, the marginal increase in refined silver recovery rates declined.

Regarding smelter quotations, smelters with guaranteed internal resource supply or long-term contracts for imported ore raw materials only slightly reduced their spot order quotations in line with the market or had not yet participated in the ore market trade. However, small and medium-sized smelters participated in processing fee quotations, with some manufacturers experiencing marginal production cuts or extended maintenance periods due to insufficient raw material supply.

For imported lead concentrates, in the second half of 2025, the import outlook for silver-bearing lead concentrates remained pessimistic. SMM learned at the end of July that the tender and bid price for an overseas silver-bearing lead concentrate had been quoted at -$150/dmt. Since the enrichment of rare and scattered metals was not priced separately, this price was significantly lower than the SMMpb60TC quotation. Due to the scarcity of global lead-polymetallic ore resources and production cuts at some lead-zinc mine projects, there was no expectation of a rebound in forward pb60TC quotations in the market. Forward pb60TC contracts (M+3) had low trading volumes, and the domestic supply of lead concentrates was expected to remain in a tight balance.